Warren Buffett is one of the most closely followed investors of all time. Known as the Oracle of Omaha, Buffett’s investment strategy has become a template for people looking to create and preserve wealth.

Buffett spent decades studying well-capitalized businesses that generate strong cash flow and use excess profits to reward shareholders. These are qualities that are not typically associated with high-growth technology businesses that burn money. Hence, Buffett avoided the sector for quite some time.

But in 2016, Buffett shocked Wall Street after he took a sizable position in Apple(NASDAQ: AAPL). What was initially considered a head-scratcher has ballooned into his largest position, currently representing just over 50% of Berkshire Hathaway‘s investment portfolio. Although he has been a repeat buyer of the stock, the real reason for Apple’s top-ranking is its price appreciation over the years.

Let’s dig into Apple’s business and assess if the “Magnificent Seven” stock is worth a position in your portfolio.

Apple’s revenue is declining…

Apple is one of the most innovative companies in history, creating everyday devices such as the iPhone and iPod. For this reason, the company is one of the most recognized brands in the world. For years, Apple generated eye-popping revenue and profit growth, earning cheers from investors and sending the stock shooting higher.

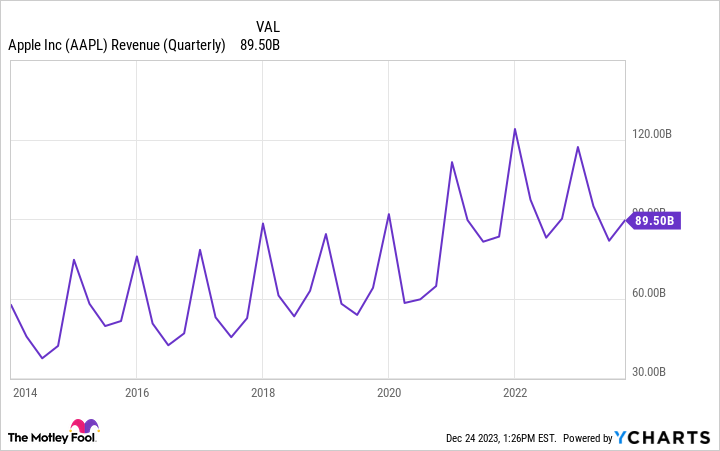

However, like many businesses, Apple reached a maturing point in its corporate lifecycle and the business results reflect this dynamic. A tough macroeconomy plagued by inflation and high borrowing costs has taken a toll on consumer demand for luxury products, thereby stifling Apple’s revenue. The chart below illustrates the company’s sales over the past decade.

AAPL Revenue (Quarterly) Chart

While consumer businesses tend to ebb and flow, the obvious theme here is that Apple’s top line is no longer accelerating. Some investors may fear that Apple’s best days are behind it and believe exiting the stock for new growth opportunities is the most prudent move. While this view has merit, there is more to consider with Apple than just its revenue patterns.

Image source: Getty Images.

…but profits are growing

Although Apple is struggling to grow its overall revenue, investors should keep in mind that the company derives sales from more than just hardware devices. Apple splits its revenue into five categories: iPhone, iPad, Mac, wearables, and services. Each of these revenue streams declined in fiscal 2023, ended Sept. 30, except for the highly profitable services operation.

AAPL Gross Profit Margin (Quarterly) Chart

The chart above illustrates Apple’s gross margin profile over the past 10 years. Even though the company has faced some headwinds from a revenue perspective, the trend above shows just how powerfully the underlying business is really performing.

The company has been able to expand its profits on a consistent basis thanks to a robust services business that boasts roughly 70% gross margins. This stunning margin expansion has fueled hundreds of billions in free cash flow over the years, bolstering the company’s balance sheet. The company has found some creative ways to allocate capital, such as consistently repurchasing stock.

AAPL Stock Buyback (Annual) Chart

Best recipe: Patience, discipline, and long-term thinking

All of the Magnificent Seven stocks are focusing in on artificial intelligence (AI) in some capacity. While AI represents a new growth frontier, it’s a costly endeavor. For this reason, many businesses investing in AI do not have the flexibility to provide more direct rewards such as dividends or stock buybacks.

Not only does Apple do both of these. Apple is notorious for playing coy, often keeping a tight lid on new product development and surprising the public. Given the company’s massive ecosystem, stitched together by a fiercely loyal customer base, I think it’s only a matter of time before Apple’s AI roadmap is revealed.

At a forward price-to-earnings (P/E) multiple of 29.5, Apple stock ranks third-lowest among its “Magnificent Seven” peers. I think this says a lot about how the markets are viewing Buffett’s top holding. Clearly, investors are souring on the stock due to revenue deceleration and an unclear AI vision at the surface level. But to me, history points to one core theme: Apple consistently performs at a high level.

I think that as inflation cools, the clouds shading the economy will begin to clear and Apple will find itself in a unique position returning to top-line growth. This should augment the overall margin profile of the business and help sustain cash-flow generation. Moreover, in due time Apple’s role in artificial intelligence should begin to take shape. Now looks like a good opportunity to take advantage of market dynamics and scoop up some shares in this underappreciated and misunderstood stock.

Should you invest $1,000 in Apple right now?

Before you buy stock in Apple, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Apple wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

NEW YORK (AP) — Shares of Tesla soared Wednesday as investors bet that the electric vehicle maker and its CEO Elon Musk will benefit from Donald Trump’s return to the White House.

Tesla stands to make significant gains under a Trump administration with the threat of diminished subsidies for alternative energy and electric vehicles doing the most harm to smaller competitors. Trump’s plans for extensive tariffs on Chinese imports make it less likely that Chinese EVs will be sold in bulk in the U.S. anytime soon.

“Tesla has the scale and scope that is unmatched,” said Wedbush analyst Dan Ives, in a note to investors. “This dynamic could give Musk and Tesla a clear competitive advantage in a non-EV subsidy environment, coupled by likely higher China tariffs that would continue to push away cheaper Chinese EV players.”

Tesla shares jumped 14.8% Wednesday while shares of rival electric vehicle makers tumbled. Nio, based in Shanghai, fell 5.3%. Shares of electric truck maker Rivian dropped 8.3% and Lucid Group fell 5.3%.

Tesla dominates sales of electric vehicles in the U.S, with 48.9% in market share through the middle of 2024, according to the U.S. Energy Information Administration.

Subsidies for clean energy are part of the Inflation Reduction Act, signed into law by President Joe Biden in 2022. It included tax credits for manufacturing, along with tax credits for consumers of electric vehicles.

Musk was one of Trump’s biggest donors, spending at least $119 million mobilizing Trump’s supporters to back the Republican nominee. He also pledged to give away $1 million a day to voters signing a petition for his political action committee.

In some ways, it has been a rocky year for Tesla, with sales and profit declining through the first half of the year. Profit did rise 17.3% in the third quarter.

The U.S. opened an investigation into the company’s “Full Self-Driving” system after reports of crashes in low-visibility conditions, including one that killed a pedestrian. The investigation covers roughly 2.4 million Teslas from the 2016 through 2024 model years.

And investors sent company shares tumbling last month after Tesla unveiled its long-awaited robotaxi at a Hollywood studio Thursday night, seeing not much progress at Tesla on autonomous vehicles while other companies have been making notable progress.

TORONTO – Canada’s main stock index was up more than 100 points in late-morning trading, helped by strength in base metal and utility stocks, while U.S. stock markets were mixed.

The S&P/TSX composite index was up 103.40 points at 24,542.48.

In New York, the Dow Jones industrial average was up 192.31 points at 42,932.73. The S&P 500 index was up 7.14 points at 5,822.40, while the Nasdaq composite was down 9.03 points at 18,306.56.

The Canadian dollar traded for 72.61 cents US compared with 72.44 cents US on Tuesday.

The November crude oil contract was down 71 cents at US$69.87 per barrel and the November natural gas contract was down eight cents at US$2.42 per mmBTU.

The December gold contract was up US$7.20 at US$2,686.10 an ounce and the December copper contract was up a penny at US$4.35 a pound.

This report by The Canadian Press was first published Oct. 16, 2024.

TORONTO – Canada’s main stock index was up more than 200 points in late-morning trading, while U.S. stock markets were also headed higher.

The S&P/TSX composite index was up 205.86 points at 24,508.12.

In New York, the Dow Jones industrial average was up 336.62 points at 42,790.74. The S&P 500 index was up 34.19 points at 5,814.24, while the Nasdaq composite was up 60.27 points at 18.342.32.

The Canadian dollar traded for 72.61 cents US compared with 72.71 cents US on Thursday.

The November crude oil contract was down 15 cents at US$75.70 per barrel and the November natural gas contract was down two cents at US$2.65 per mmBTU.

The December gold contract was down US$29.60 at US$2,668.90 an ounce and the December copper contract was up four cents at US$4.47 a pound.

This report by The Canadian Press was first published Oct. 11, 2024.