I don’t do a lot of these things because it’s just easier and more comfortable to talk about stuff on my podcast but this one sent me a great list of questions ahead of time that I liked.

Here are 6 of the best questions with some thoughts on each:

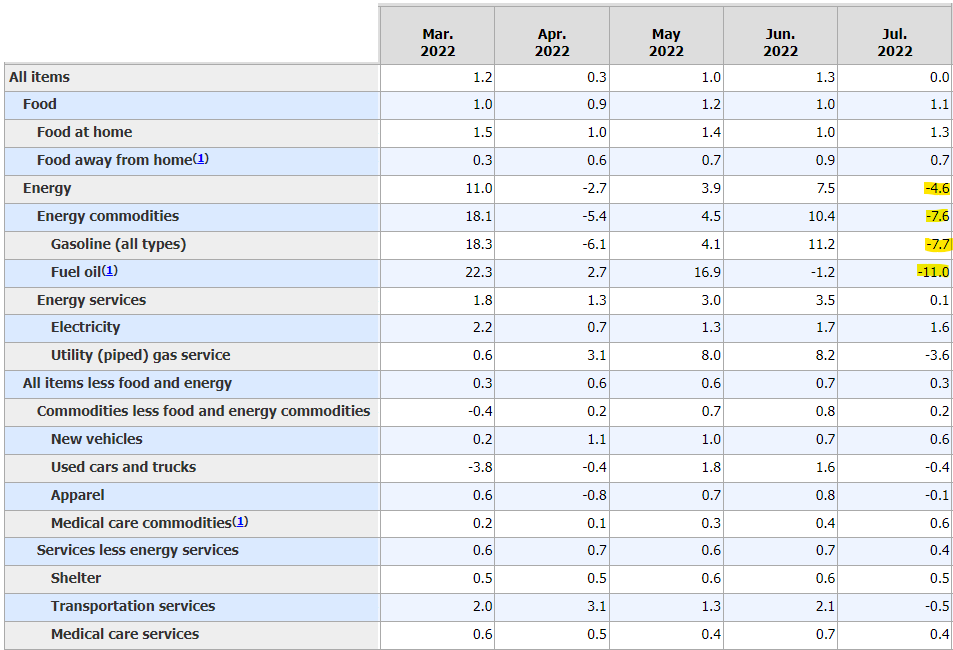

(1) What is your reaction to the latest CPI report and your outlook on inflation?

Inflation was basically flat from June to July.1

This is the first good news we’ve gotten on the price front in a while. You can see the energy components finally softened in a big way (via the BLS):

Inflation of 8.5% over the past 12 months is still uncomfortably high but it’s going to take a while for that rate to subside, even if prices do continue to slow in the months ahead.

Obviously, one data point does not make a trend but it does seem like the Fed’s moves along with some easing of supply chains have helped stop the uninterrupted rise in prices.

Gas prices are down like 60 days in a row. Oil prices are down. Used car prices are finally falling.

We can build on this (I hope).

(2) Where does the Fed go from here?

It’s difficult to know exactly what the Fed will do without knowing what the inflation data will look like in the coming months.

The labor market is certainly in a better place than it was in 2020 but inflation is running just a smidge higher than their 2% target.

Fed officials say they’re not done hiking rates just yet and I tend to believe them (for now):

Minneapolis Federal Reserve Bank President Neel Kashkari on Wednesday said he is sticking to his view that the U.S. central bank will need to raise its policy rate another 1.5 percentage points this year and more in 2023, even if that causes a recession.

The Fed is “far, far away from declaring victory” on inflation, Kashkari said at the Aspen Ideas Conference, despite the “welcome” news in the consumer price index report earlier in the day that inflation may have begun to cool.

Kashkari said he hasn’t “seen anything that changes” the need to raise the Fed’s policy rate to 3.9% by year-end and to 4.4% by the end of 2023. The rate is currently in the 2.25%-2.5% range.

The Fed waited too long to act and they don’t want to look like idiots again.

They care more about inflation than the job market right now so they’ll likely keep raising rates until we get a number of lower inflation prints.

If they go too far that has to be a risk to both the stock market and the economy.

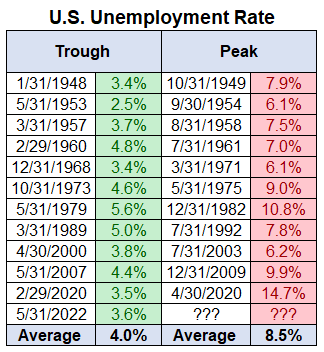

(3) What does a soft landing look like?

Let’s start with what a hard landing looks like and work backwards.

The average increase is more than a doubling off the lows. That would take us to more than 7% from the current 3.5% unemployment rate.

To me, a soft landing would see inflation below 4% or so without a commensurate rise in the unemployment rate. The lowest it’s ever increased to during past slowdowns is just over 6%.

I’d say anything 5% and under for the unemployment rate would be a win if we could get inflation back to 3% or so.

What’s the scenario that could make this happen?

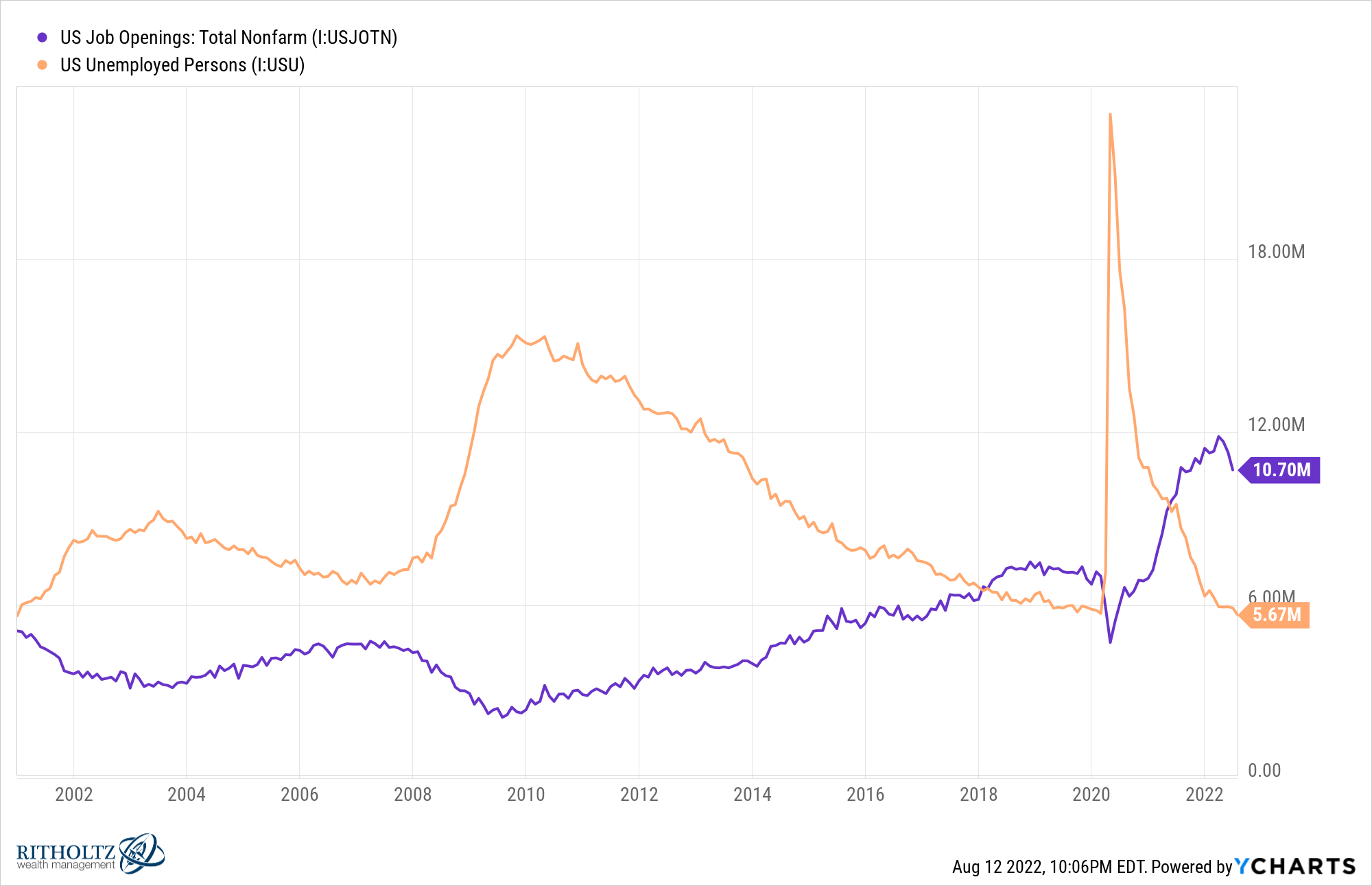

The labor market is in a weird place right now since there are more jobs available than people who are looking for one:

Those openings have come down a bit from 11.7 million to 10.7 million. The dream soft landing scenario for the Fed would see these openings fall by 4-5 million but the unemployment rate doesn’t go much above 4-5%.

Is this actually possible?

History says no but employers have been dealing with a challenging hiring market since the start of the pandemic.

Sam Ro wrote a thought-provoking piece this week about the concept of labor hoarding that’s worth considering:

So what explains the current reluctance to shed workers?

Maybe recent experience has something to do with it.

Much of the ongoing economic recovery has come with persistent labor shortages. Employers haven’t been able to hire fast enough to keep up with the booming demand for their goods and services.

At least some of the employers seeing business slow right now remember how hard it was to recruit talent over the past two years and would rather just hang on to employees, even if it comes with carrying costs.

As a matter of convenience, of course it’s easier to just hang on to workers during a slowdown or recession if you expect the downturn to be brief and shallow.

Millions of people were either let go or put on the shelf in 2020 and that made it more difficult to re-staff once demand came back faster than companies are used to.

What if employers hold onto more employees than in past recessions if they assume the next one will be mild?

What if companies don’t want to go through the hiring process all over again following a recession?

That’s probably the best-case scenario for a soft landing if the Fed does cause a meaningful downturn in economic activity to get inflation under control.

(4) What is your general outlook on the markets and/or a recession?

I wish I had a good answer for this one. I don’t.

We could go into a recession while the stock market hits all-time highs.

Or we could see the stock market tank even if the economy improves from here.

Sometimes these things don’t make sense.

My macro outlook has never really helped my portfolio all that much.

Sometimes my thoughts on the economy/markets would have served me well. Other times my thoughts on the economy/markets would have destroyed my portfolio.

Here’s a little secret about investing the pros will never admit — you don’t have to predict the future to be successful in the markets.

Outlooks are more helpful for your ego than your performance in most cases as long as you have a reasonable investment plan in place.

(5) What can we learn from this downturn?

Since the start of 2020, the U.S. stock market has fallen 34%, risen 120%, declined 24% and now gained almost 17%.

In less than 3 years, it’s felt like we’ve lived through every cycle imaginable — 1918, 1929, 1999, the 1970s, maybe the 1960s and some other parallel I’m probably missing.

Everything in the markets is cyclical.

Stuff that has never happened before happens all the time.

The biggest risks are always the things you’re not thinking about or preparing for.

OTTAWA – Canada’s unemployment rate held steady at 6.5 per cent last month as hiring remained weak across the economy.

Statistics Canada’s labour force survey on Friday said employment rose by a modest 15,000 jobs in October.

Business, building and support services saw the largest gain in employment.

Meanwhile, finance, insurance, real estate, rental and leasing experienced the largest decline.

Many economists see weakness in the job market continuing in the short term, before the Bank of Canada’s interest rate cuts spark a rebound in economic growth next year.

Despite ongoing softness in the labour market, however, strong wage growth has raged on in Canada. Average hourly wages in October grew 4.9 per cent from a year ago, reaching $35.76.

Friday’s report also shed some light on the financial health of households.

According to the agency, 28.8 per cent of Canadians aged 15 or older were living in a household that had difficulty meeting financial needs – like food and housing – in the previous four weeks.

That was down from 33.1 per cent in October 2023 and 35.5 per cent in October 2022, but still above the 20.4 per cent figure recorded in October 2020.

People living in a rented home were more likely to report difficulty meeting financial needs, with nearly four in 10 reporting that was the case.

That compares with just under a quarter of those living in an owned home by a household member.

Immigrants were also more likely to report facing financial strain last month, with about four out of 10 immigrants who landed in the last year doing so.

That compares with about three in 10 more established immigrants and one in four of people born in Canada.

This report by The Canadian Press was first published Nov. 8, 2024.

The Canadian Institute for Health Information says health-care spending in Canada is projected to reach a new high in 2024.

The annual report released Thursday says total health spending is expected to hit $372 billion, or $9,054 per Canadian.

CIHI’s national analysis predicts expenditures will rise by 5.7 per cent in 2024, compared to 4.5 per cent in 2023 and 1.7 per cent in 2022.

This year’s health spending is estimated to represent 12.4 per cent of Canada’s gross domestic product. Excluding two years of the pandemic, it would be the highest ratio in the country’s history.

While it’s not unusual for health expenditures to outpace economic growth, the report says this could be the case for the next several years due to Canada’s growing population and its aging demographic.

Canada’s per capita spending on health care in 2022 was among the highest in the world, but still less than countries such as the United States and Sweden.

The report notes that the Canadian dental and pharmacare plans could push health-care spending even further as more people who previously couldn’t afford these services start using them.

This report by The Canadian Press was first published Nov. 7, 2024.

Canadian Press health coverage receives support through a partnership with the Canadian Medical Association. CP is solely responsible for this content.

As Canadians wake up to news that Donald Trump will return to the White House, the president-elect’s protectionist stance is casting a spotlight on what effect his second term will have on Canada-U.S. economic ties.

Some Canadian business leaders have expressed worry over Trump’s promise to introduce a universal 10 per cent tariff on all American imports.

A Canadian Chamber of Commerce report released last month suggested those tariffs would shrink the Canadian economy, resulting in around $30 billion per year in economic costs.

More than 77 per cent of Canadian exports go to the U.S.

Canada’s manufacturing sector faces the biggest risk should Trump push forward on imposing broad tariffs, said Canadian Manufacturers and Exporters president and CEO Dennis Darby. He said the sector is the “most trade-exposed” within Canada.

“It’s in the U.S.’s best interest, it’s in our best interest, but most importantly for consumers across North America, that we’re able to trade goods, materials, ingredients, as we have under the trade agreements,” Darby said in an interview.

“It’s a more complex or complicated outcome than it would have been with the Democrats, but we’ve had to deal with this before and we’re going to do our best to deal with it again.”

American economists have also warned Trump’s plan could cause inflation and possibly a recession, which could have ripple effects in Canada.

It’s consumers who will ultimately feel the burden of any inflationary effect caused by broad tariffs, said Darby.

“A tariff tends to raise costs, and it ultimately raises prices, so that’s something that we have to be prepared for,” he said.

“It could tilt production mandates. A tariff makes goods more expensive, but on the same token, it also will make inputs for the U.S. more expensive.”

A report last month by TD economist Marc Ercolao said research shows a full-scale implementation of Trump’s tariff plan could lead to a near-five per cent reduction in Canadian export volumes to the U.S. by early-2027, relative to current baseline forecasts.

Retaliation by Canada would also increase costs for domestic producers, and push import volumes lower in the process.

“Slowing import activity mitigates some of the negative net trade impact on total GDP enough to avoid a technical recession, but still produces a period of extended stagnation through 2025 and 2026,” Ercolao said.

Since the Canada-United States-Mexico Agreement came into effect in 2020, trade between Canada and the U.S. has surged by 46 per cent, according to the Toronto Region Board of Trade.

With that deal is up for review in 2026, Canadian Chamber of Commerce president and CEO Candace Laing said the Canadian government “must collaborate effectively with the Trump administration to preserve and strengthen our bilateral economic partnership.”

“With an impressive $3.6 billion in daily trade, Canada and the United States are each other’s closest international partners. The secure and efficient flow of goods and people across our border … remains essential for the economies of both countries,” she said in a statement.

“By resisting tariffs and trade barriers that will only raise prices and hurt consumers in both countries, Canada and the United States can strengthen resilient cross-border supply chains that enhance our shared economic security.”

This report by The Canadian Press was first published Nov. 6, 2024.