A Golden Investment Opportunity: 1 Top Stock to Buy Before It Soars 40% to Hit $4 Trillion, According to a Wall Street ... - Yahoo Finance | Canada News Media

Apple(NASDAQ: AAPL) remains a top technology stock at Wedbush Securities despite worrisome results in its China business. Analyst Dan Ives dismissed those concerns as noise and recently said Apple will become the first $4 trillion company by the end of 2024. That prediction implies 40% upside from its current market capitalization of $2.85 trillion.

Ives provided additional commentary in a note to clients: “With roughly 240 million iPhones in the window of an upgrade opportunity globally now at play for iPhone 15, and services reaccelerating into [fiscal year 2024], we view this as a golden opportunity to own Apple for the next year.”

Here’s what investors should know.

Apple worried investors with declining sales in China and a weak outlook

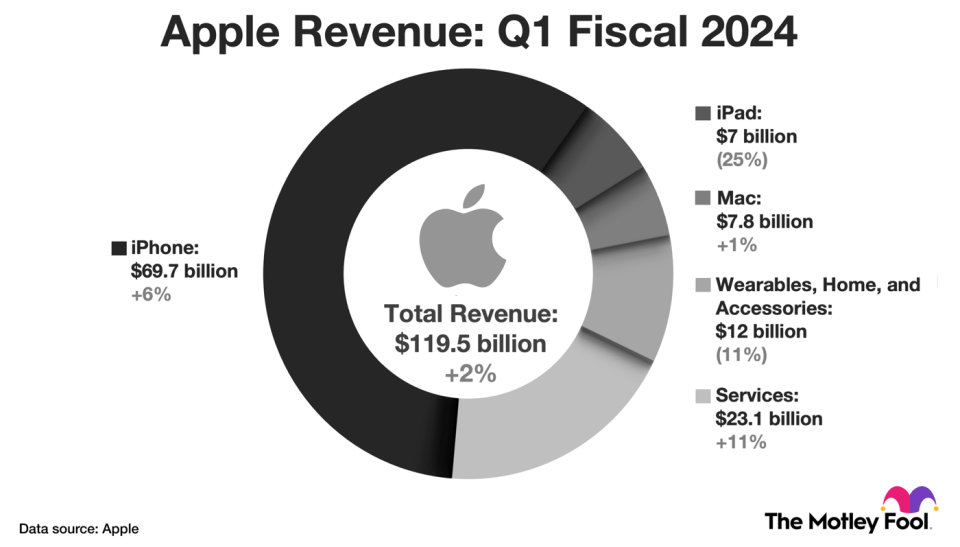

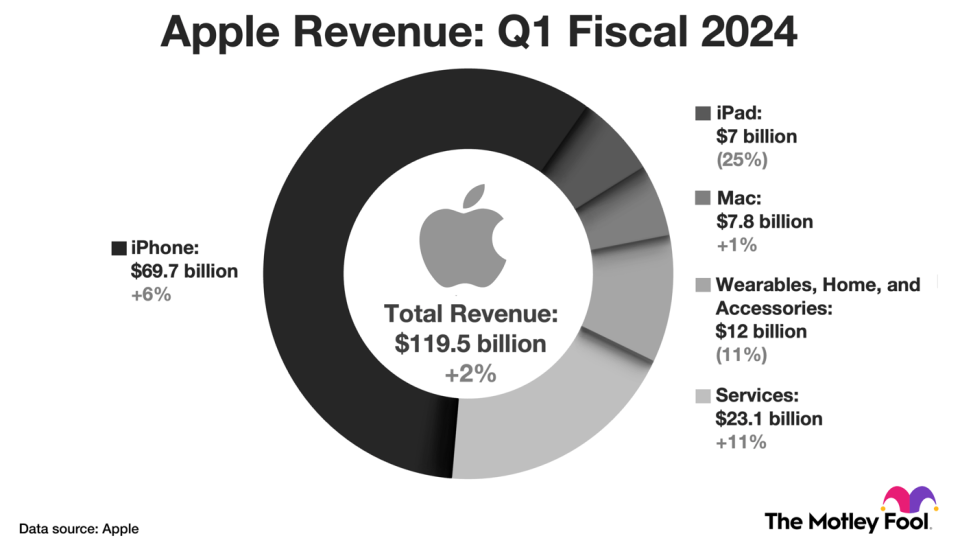

Apple reported better-than-expected financial results for the first quarter of fiscal 2024, which ended Dec. 30, 2023. Revenue rose 2% to $119.5 billion on a modest uptick in iPhone sales and more robust growth in services revenue. Management highlighted advertising, video, and cloud services as major contributors to that momentum.

Apple earns higher margins on services than hardware, so the company has become more profitable over time as its services business has scaled. That trend continued in the first quarter. Gross margin expanded 290 basis points and GAAP earnings jumped 16% to $2.18 per diluted share. Stock buybacks also contributed to rapid bottom-line growth.

The chart below provides a more detailed look at Apple’s revenue growth in the first quarter.

Chart by Author. Shown above is Apple’s revenue across all five business segments in the first quarter of fiscal 2024 (ended Dec. 30, 2023).

Despite strong results, Apple shares slid about 4% following the report for two reasons. First, sales declined 13% in China, fueling concern that the company is losing share to domestic competitors like Huawei and Xiaomi. Jeffries analysts estimate that iPhone sales fell 30% in China during the first week of 2024. That is a pressing concern because China is Apple’s third-largest market and represents one-sixth of total revenue.

Second, while Apple did not provide formal guidance, management implied that revenue would fall about 5% in the second quarter. CFO Luca Maestri attributed that weak outlook to the absence of certain tailwinds. Specifically, Apple benefited from pent-up iPhone demand in the second quarter of last year because factory closures had previously limited production.

Apple is a consumer electronics leader with growth opportunities in services

Apple has a strong presence in several corners of the consumer electronics market. Its leadership in smartphones (as measured by revenue and shipments) is the foundation of its business. But the tech titan also enjoys a dominant position in the tablet and smartwatch markets, and it’s one of the largest personal computer vendors. That success is built on brand authority and engineering expertise.

Specifically, Apple pairs premium hardware (including custom chips) with proprietary software and services to create a compelling user experience. And while the iPhone is the center of that ecosystem, adjacent products like Macs and AirPods make the ecosystem stickier. Those qualities grant Apple substantial pricing power. The average iPhone costs twice as much as the average Android smartphone, according to Insider Intelligence.

That pricing power allows Apple to invest heavily in research and development. The company recently launched its first mixed-reality device, the Apple Vision Pro, a product some pundits believe will eventually replace the iPad.

Apple’s installed base surpassed 2.2 billion devices in the first quarter. The company monetizes those consumers once with the initial purchase, but it aims to monetize them continuously thereafter with its services business. For instance, Apple earns services revenue on App Store fees and related advertising, iCloud storage, and financial products like Apple Pay, among other subscription products.

The company has a strong position in a few of those categories. The Apple App Store leads the mobile application market in revenue; Apple is the fifth-fastest-growing digital advertising company in the U.S.; and Apple Pay is the most popular in-store mobile wallet among U.S. consumers.

Apple shares trade at an expensive valuation compared to big tech peers

To create shareholder value, Apple needs to maintain its strong position in smartphones and continue to grow its services business. The company must also stay current on nascent technologies like virtual reality and augmented reality. Products that incorporate those technologies could be the next big thing in consumer electronics. If Apple falls behind, it may be displaced in the same way the iPhone displaced products from Nokia and BlackBerry.

Whether Apple reaches $4 trillion in 2024 is a coin toss. Investors interested in buying the stock should plan on holding it for three to five years at a minimum. Personally, I doubt Apple can deliver market-beating returns during that period. Its current valuation of 29 times earnings looks expensive compared to the long-term earnings growth of 9.4% annually that Wall Street expects.

Taken together, those values produce a PEG ratio of 3.1 for Apple. For context, Alphabet has a PEG ratio of 1.5, Amazon sports a PEG ratio of 2.3, and Microsoft has a PEG ratio of 2.5. That means Apple is more expensive than its big tech peers.

Should you invest $1,000 in Apple right now?

Before you buy stock in Apple, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Apple wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Trevor Jennewine has positions in Amazon. The Motley Fool has positions in and recommends Alphabet, Amazon, Apple, Jefferies Financial Group, and Microsoft. The Motley Fool recommends BlackBerry and recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

TORONTO – Canada’s main stock index was up more than 100 points in late-morning trading, helped by strength in base metal and utility stocks, while U.S. stock markets were mixed.

The S&P/TSX composite index was up 103.40 points at 24,542.48.

In New York, the Dow Jones industrial average was up 192.31 points at 42,932.73. The S&P 500 index was up 7.14 points at 5,822.40, while the Nasdaq composite was down 9.03 points at 18,306.56.

The Canadian dollar traded for 72.61 cents US compared with 72.44 cents US on Tuesday.

The November crude oil contract was down 71 cents at US$69.87 per barrel and the November natural gas contract was down eight cents at US$2.42 per mmBTU.

The December gold contract was up US$7.20 at US$2,686.10 an ounce and the December copper contract was up a penny at US$4.35 a pound.

This report by The Canadian Press was first published Oct. 16, 2024.

TORONTO – Canada’s main stock index was up more than 200 points in late-morning trading, while U.S. stock markets were also headed higher.

The S&P/TSX composite index was up 205.86 points at 24,508.12.

In New York, the Dow Jones industrial average was up 336.62 points at 42,790.74. The S&P 500 index was up 34.19 points at 5,814.24, while the Nasdaq composite was up 60.27 points at 18.342.32.

The Canadian dollar traded for 72.61 cents US compared with 72.71 cents US on Thursday.

The November crude oil contract was down 15 cents at US$75.70 per barrel and the November natural gas contract was down two cents at US$2.65 per mmBTU.

The December gold contract was down US$29.60 at US$2,668.90 an ounce and the December copper contract was up four cents at US$4.47 a pound.

This report by The Canadian Press was first published Oct. 11, 2024.

TORONTO – Canada’s main stock index was little changed in late-morning trading as the financial sector fell, but energy and base metal stocks moved higher.

The S&P/TSX composite index was up 0.05 of a point at 24,224.95.

In New York, the Dow Jones industrial average was down 94.31 points at 42,417.69. The S&P 500 index was down 10.91 points at 5,781.13, while the Nasdaq composite was down 29.59 points at 18,262.03.

The Canadian dollar traded for 72.71 cents US compared with 73.05 cents US on Wednesday.

The November crude oil contract was up US$1.69 at US$74.93 per barrel and the November natural gas contract was up a penny at US$2.67 per mmBTU.

The December gold contract was up US$14.70 at US$2,640.70 an ounce and the December copper contract was up two cents at US$4.42 a pound.

This report by The Canadian Press was first published Oct. 10, 2024.