Apple (NASDAQ:AAPL) is a tech giant, and the highest market capitalization stock traded on the stock market. The iPhone is the most successful consumer product ever created in the entire universe. A successful encore is nearly impossible. As the innovator of the smartphone, Apple has had unrivaled success and is a global powerhouse and dominant position the United States, especially with teenagers and young adults.

Globally, around 1 billion people have an iPhone. Since the launch of the iPhone sales is estimated to have totaled $2 trillion. Apple is the most valuable company of all time, with a market cap of $2.6 Trillion.

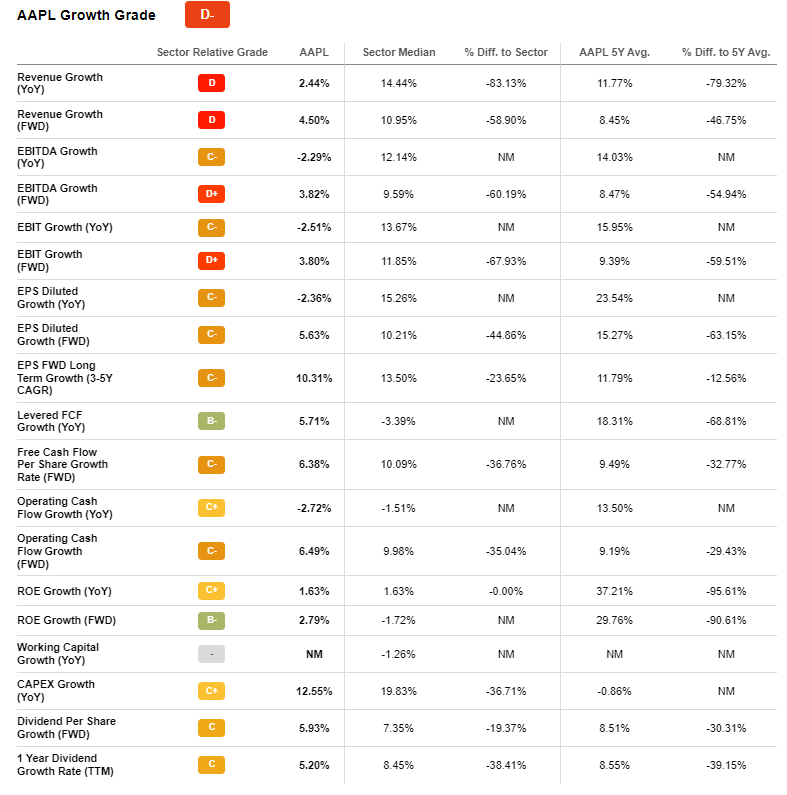

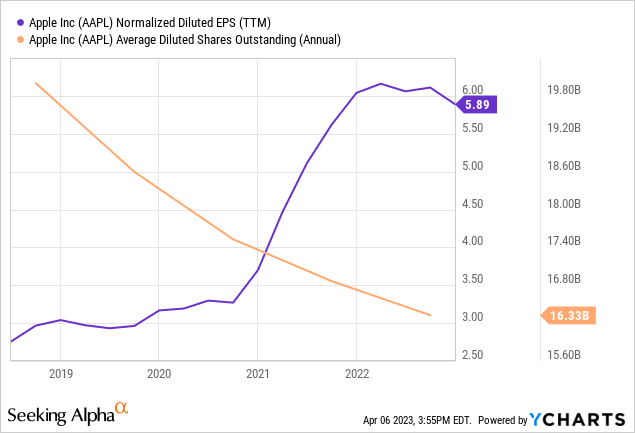

However, revenue and earnings growth has slowed to the 4-6% range. This slow growth is primarily a victim of “The Law of Large Numbers” and Apple’s on success. Additionally, Apple has not been immune to COVID-19 supply chain chokepoints and a saturated smartphone market. Most of the developed world has a smartphone so business there is replacement only and few new features warrant an upgrade. In the developing world, fewer customers can afford the luxury of purchasing the status symbol of buying an iPhone.

SeekingAlpha

Nonetheless, Apple is still priced as a growth stock with a 27.8 PE (Price to Earnings ratio). Given that AAPL had a 12 PE in 2013 when its 8.6% 10-year CAGR revenue was still in front of them, we would not be surprised to see the PE fall to this level which would be more appropriate given its low forward expected growth. Apple has been one of the greatest investments of all time. I hope you own it and are in a position to sell or trim. I believe the stock will underperform over the next 5-10 years and do not own any shares.

Outlook

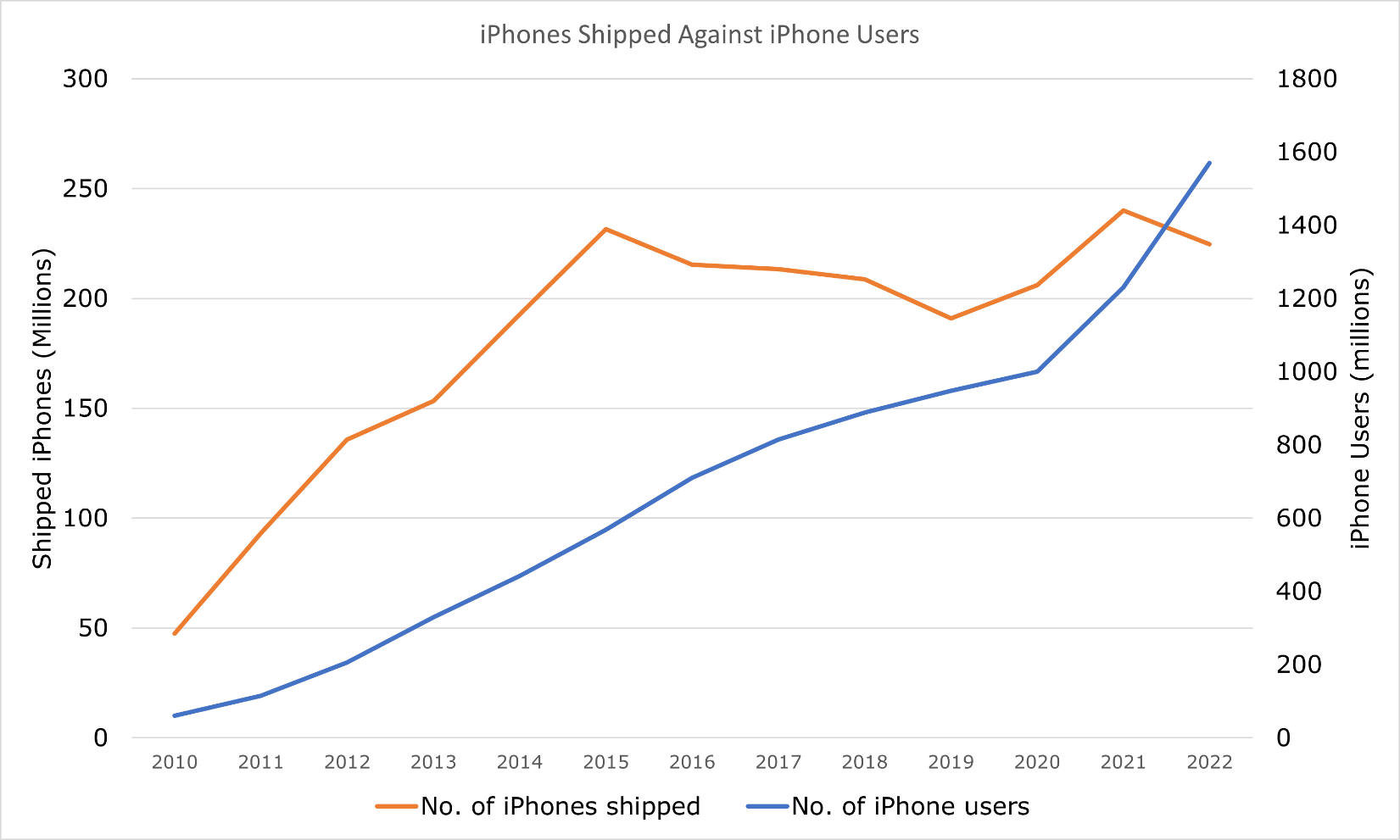

Consumer spending is expected to weaken in FY23. Apple’s financial performance is heavily reliant on the success of their consumer products like the iPhone. Around 52% of revenue in FY22 came from iPhone sales, trailed by services which made up 20%. Additionally, iPhone sales have been flat in recent years, stagnating or declining since FY15. No other device Apple has produced has had the growth rate or sales of the iPhone. It is not even close as the iPhone is the most successful consumer product ever created in the entire universe.

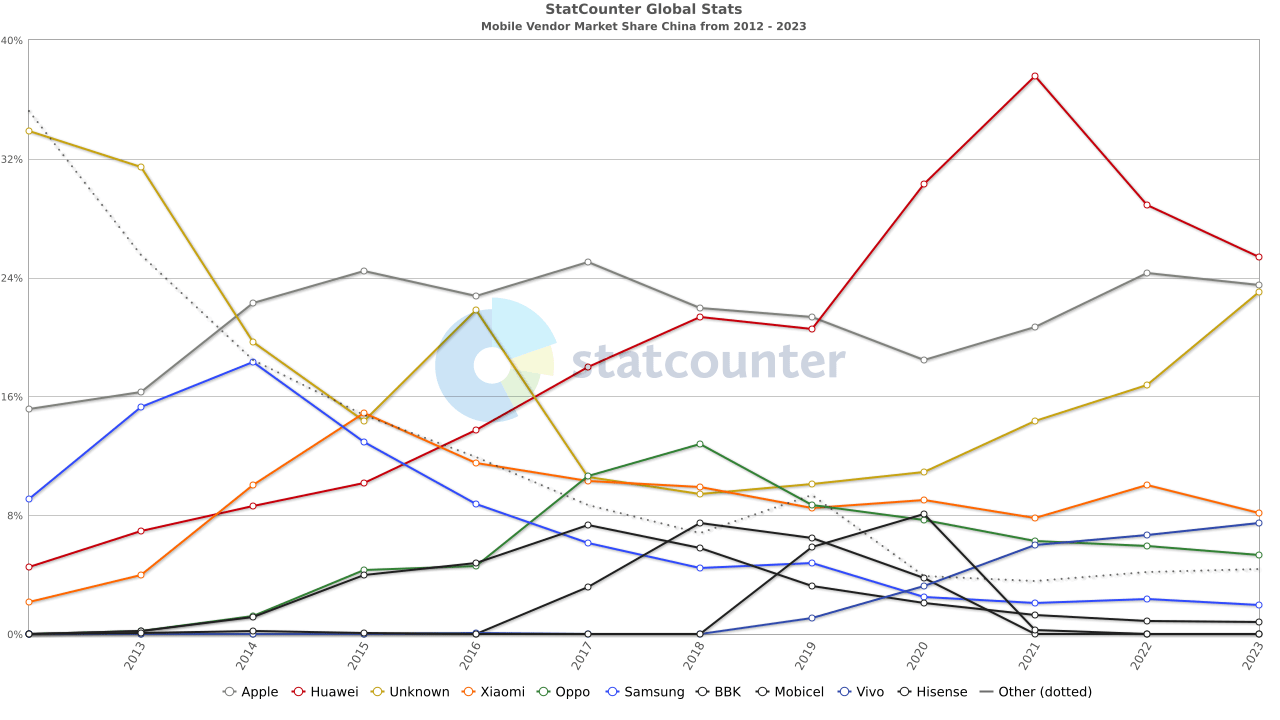

Apple’s market share in the smartphone market ballooned to record highs in FY20, reaching 61% in the US. While investors had been hopeful of a similar trend in China with its emerging middle class, Apple has not been able to breach the 25% mark in market share since the iPhone launched in China in 2009. Additionally, despite iPhone sales stagnating, iPhone users have steadily grown. While this will increase the company’s service revenue, it is clear that people are not as eager to buy brand-new iPhones every year as they have been in the past.

BuildingBenjamins, Apple, BusinessOfApps

Chinese Market Share (Statcounter)

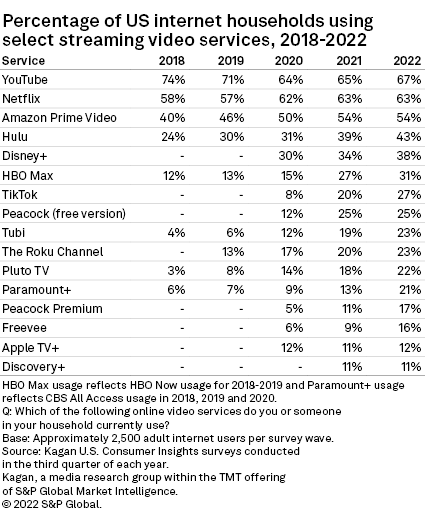

There is room to grow in the service area, with AppleTV launching its subscription service. But the market is already saturated with everyone rolling out streaming services. Apple has only been able to breach just over 10% market share in this area.

S&P Global Market Intelligence

Apple has made no friends in the advertising space, with its strict rules around advertising and user tracking making it an unattractive platform to advertise on. While this has been applauded as pro-privacy and pro-consumer, it dulled their own ability to carve out a revenue stream.

Apple is under scrutiny in the United States and Europe for competitive iPhone and MacOS ecosystem practices. Since 2019 Apple has been under investigation in the US on whether or not it suppresses third party apps in favor of its own. In Europe meanwhile, the entire MacOS ecosystem has been declared as a “threat to competition [utilizes] practices [that] effectively prevent them”. Not only this, but the most downloaded app on iPhones today is TikTok, which has come under equally harsh scrutiny.

It is not as though AAPL is not a financially healthy company, it has fantastic margins on every level and eyewatering levels of free cash flow yearly – nearly $100 billion. In 1Q23 AAPL repurchased $20 billion in stock but has been stingy on the dividend with only a 0.56% forward yield. We struggle to see why management would prioritize further repurchases instead of dividend expansion at these stock valuations. Our guess is the board is concerned a reasonable dividend would be like an announcement that Apple’s growth days are behind it. Consistently spending $80 billion per year on repurchases and reducing outstanding share count by roughly 4% is not a sign of a company that believes that it has lots of opportunities to invest capital in areas that will match their existing business. That gets back to the core of the problem; no business is going to have the size and margins of Apple’s hugely successful iPhone.

While the financial robustness of Apple is hard to deny, we have growing concerns about the stagnation in earnings per share and revenue – especially in segments that used to be powerhouses. The company’s market share has also not budged, and efforts to expand into streaming with AppleTV and Apple Music have faced steep competition. We no longer believe there is a likely long-term case for Apple from a growth investor’s perspective and have removed it from our portfolio.

TORONTO – Canada’s main stock index was up more than 100 points in late-morning trading, helped by strength in base metal and utility stocks, while U.S. stock markets were mixed.

The S&P/TSX composite index was up 103.40 points at 24,542.48.

In New York, the Dow Jones industrial average was up 192.31 points at 42,932.73. The S&P 500 index was up 7.14 points at 5,822.40, while the Nasdaq composite was down 9.03 points at 18,306.56.

The Canadian dollar traded for 72.61 cents US compared with 72.44 cents US on Tuesday.

The November crude oil contract was down 71 cents at US$69.87 per barrel and the November natural gas contract was down eight cents at US$2.42 per mmBTU.

The December gold contract was up US$7.20 at US$2,686.10 an ounce and the December copper contract was up a penny at US$4.35 a pound.

This report by The Canadian Press was first published Oct. 16, 2024.

TORONTO – Canada’s main stock index was up more than 200 points in late-morning trading, while U.S. stock markets were also headed higher.

The S&P/TSX composite index was up 205.86 points at 24,508.12.

In New York, the Dow Jones industrial average was up 336.62 points at 42,790.74. The S&P 500 index was up 34.19 points at 5,814.24, while the Nasdaq composite was up 60.27 points at 18.342.32.

The Canadian dollar traded for 72.61 cents US compared with 72.71 cents US on Thursday.

The November crude oil contract was down 15 cents at US$75.70 per barrel and the November natural gas contract was down two cents at US$2.65 per mmBTU.

The December gold contract was down US$29.60 at US$2,668.90 an ounce and the December copper contract was up four cents at US$4.47 a pound.

This report by The Canadian Press was first published Oct. 11, 2024.

TORONTO – Canada’s main stock index was little changed in late-morning trading as the financial sector fell, but energy and base metal stocks moved higher.

The S&P/TSX composite index was up 0.05 of a point at 24,224.95.

In New York, the Dow Jones industrial average was down 94.31 points at 42,417.69. The S&P 500 index was down 10.91 points at 5,781.13, while the Nasdaq composite was down 29.59 points at 18,262.03.

The Canadian dollar traded for 72.71 cents US compared with 73.05 cents US on Wednesday.

The November crude oil contract was up US$1.69 at US$74.93 per barrel and the November natural gas contract was up a penny at US$2.67 per mmBTU.

The December gold contract was up US$14.70 at US$2,640.70 an ounce and the December copper contract was up two cents at US$4.42 a pound.

This report by The Canadian Press was first published Oct. 10, 2024.