Russ Wiles

| Arizona Republic

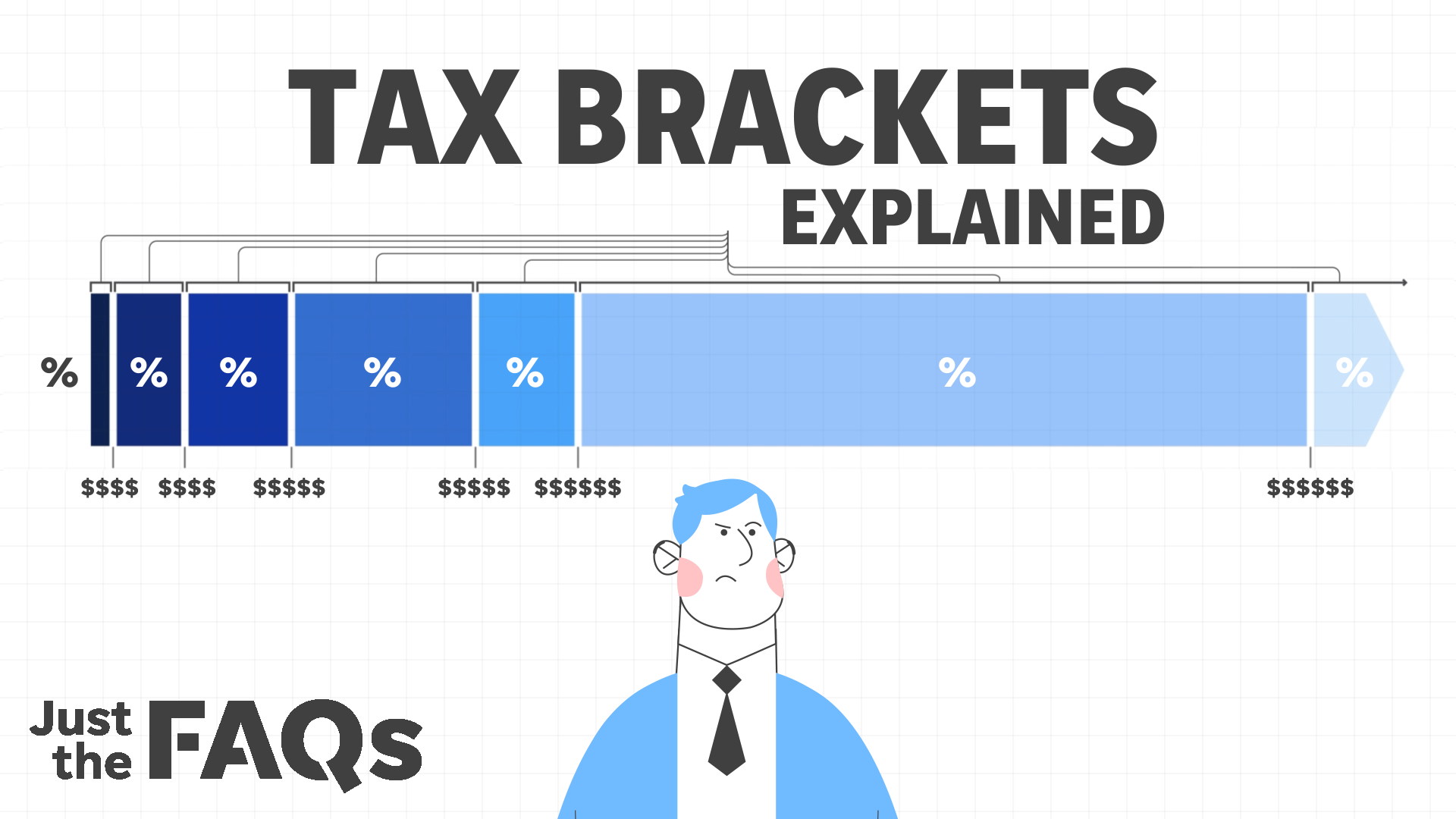

How tax brackets affect what you pay in income taxes

Why being taxed, say 22% of your income, is a lot more complicated than you may assume. Here’s a breakdown of what you actually pay in income taxes.

As a most unusual year winds down, here are some of the investment, tax and other money considerations that should be on your radar.

Some, but not all, were shaped by the COVID-19 pandemic and government efforts to ease the financial fallout.

Tax planning for a stimulus payment

A general income-tax planning tip is to defer income into the following year if you can, to delay tax payments if for no other reason. There might be another reason for doing so this month, because of the prospect for an additional round of stimulus payments.

Early in 2020, the Internal Revenue Service sent payments of up to $1,200 per person or $2,400 for married couples, plus $500 per qualifying child, to help stimulate the economy in the wake of COVID-19 business shutdowns and layoffs. The size of those payments phased out for people in certain income ranges.

For example, singles with no kids received the full $1,200 with adjusted gross income up to $75,000, with amounts phasing out 5% for income above that, ending entirely at $99,000. For married couples, those $2,400 payments started to phase out with income of at least $150,000 and ended at $198,000. Payments and phaseouts were based on 2019 income (or 2018 income for people who hadn’t yet filed their 2019 tax returns).

So why bring this up now? Because of the possibility of a second round of stimulus payments patterned at least somewhat on the first.

“It is conceivable that legislation could be delayed far enough into 2021 that the phaseout would be based on 2020 income,” noted tax researcher Wolters Kluwer. “Thus, it might be smart to delay income into 2021” to maximum the size of any new stimulus payments — and assuming you are near the possible income phaseout ranges, which aren’t yet known.

Holding out hope for a payment

For most of us, economic impact or stimulus payments are a distant memory. If we qualified, we were sent disbursements automatically or upon contacting the IRS at irs.gov. But for an untold number of Americans, the checks still haven’t arrived in the mail — or anywhere else.

As of Sept. 30, the IRS and Treasury had processed payments to 166 million people, including 26 million who aren’t required to file tax returns (mostly Social Security recipients). The IRS allowed non-filers to claim stimulus payments on its website, but the deadline for doing that has passed.

“It is not clear how many eligible individuals missed the deadline and remain at risk of not getting a payment in 2020,” said the Government Accountability Office in a recent report examining the IRS’ stimulus-payment program.

Many or most of these people likely won’t receive anything over the waning weeks of 2020. But all is not lost: Individuals still can claim their stimulus payment upon filing a tax return by next April 15. These people will want to claim the “recovery rebate credit,” which will be based on 2020 income as determined on tax returns filed next year.

Researching charity groups

This is the time of year when many people make donations to charity, whether to take advantage of tax deductions or just because they’re generous. If you’re going to the trouble, you might as well make sure your gifts go to organizations that use the money wisely.

Be aware that gifts are deductible only if made to qualifying charities, which means that donating to fake or unregistered groups can set you up for an audit down the road if you claimed a deduction.

The IRS has a “charities and nonprofits” section on its website where you can check to see if a group is properly registered.

As alternatives, Guidestar.org and CharityNavigator.org are two websites that provide financial and other information on nonprofits and are easier to use. You also may ask a nonprofit directly for evidence that it is allowed to accept deductible donations.

The big change this year is a new deduction, for 2020 only, of up to $300 for cash donations to charities. You may take the deduction even if you don’t itemize, which now describes about nine in 10 taxpayers.

Top 5 investing mistakes that are easy to avoid

Even seasoned investors make mistakes at times. But when you start investing, you’re prone to letting your emotions take over.

Looking ahead to December gains

November was hot for investors. Last month marked the best November for the Standard & Poor’s 500 index since 1928, the best month overall for the Dow Jones Industrial Average since 1987 and the best month ever for the small-stock Russell 2000 index, said LPL Financial.

Can the momentum continue, or are we due for a breather?

Ryan Detrick, chief market strategist at LPL Financial, believes the market can keep rolling, though he cautions that supercharged Novembers sometimes steal the thunder from the following Decembers. Still, the market tends not to reverse course all that quickly, which makes monthly gains of 10%-plus bullish, he said.

“A way-better-than-expected earnings season, a likely split Congress and major breakthroughs on the vaccine front all helped stocks soar last month,” explained Detrick in a prepared commentary. Those factors are still in play.

“The huge gains in November could actually be the start of something much stronger,” he continued. Following a sharp market retreat in late February and March, stocks also notched a 10%-plus monthly gain earlier this year, in April. The only other time that happened was in 1982, near the start of an historic bull market, he said.

Analyzing the political backdrop

Given the change of control in the White House, how might politics influence the investment climate? Assuming Republicans win at least one of the two special Senate runoff races in Georgia in January, Republicans would retain control of the Senate, guaranteeing a split Congress and likely relieving a lot of investors.

“We view a split Congress as market friendly because it probably would take (Joe) Biden’s most ambitious policy proposals off the table,” wrote Jeffrey Buchbinder, equity strategist at LPL Financial, in a post-election recap. “Tax increases to fund Biden’s green energy and infrastructure-investment programs may be nearly impossible to get through the Senate.”

Historically, the stock market has fared well when the two main political parties share power. Since 1950, the S&P 500 index has generated an average annual return including dividends of 15.9% during years when a Democrat sat in the White House and Congress was split, according to LPL Financial. The best combination has been a Democratic president and a Republican Congress (up 18.3% on average). The worst has been a Republican president and Democratic Congress (up 8.7% on average).

In years when Democrats controlled the White House and all of Congress, which would happen if both Georgia Senate seats go blue, the S&P 500 was up 13.2% annually.

Reach Wiles at [email protected].