This regularly-scheduled sponsored Q&A column is written by Eli Tucker, Arlington-based Realtor and Arlington resident. Please submit your questions to him via email for response in future columns. Enjoy!

Question: What has been the impact of the Coronavirus/COVID-19 on the real estate market?

Answer: I hope you are all staying healthy and sane(ish). My wife and I are trying to wrap our heads around school being canceled through the end of the academic year… yay!

Over the last two weeks, my Coronavirus columns (one and two) have included mostly anecdotal evidence on the impact of COVID-19 on the real estate market, but now we’ve been in this for long enough that I can start using market data to measure the true effects. It will be at least a few more weeks before we can measure the effect on prices, but we can look at things like supply, showing activity and contract activity now.

What I’m Seeing/Hearing

This past weekend, most Open Houses were canceled and over the last week showing activity has dropped off dramatically. However, there are still plenty of active, motivated buyers making offers. What I’m seeing/hearing right now in the D.C. Metro market is that competition is down, prices haven’t taken much of a hit (yet), and new listings are still coming onto the market.

Mortgage rates had their most volatile week ever last week as investors basically stopped buying mortgages on the secondary market, but the Fed stepped in and has promised to stabilize the market until our economy (hopefully) returns to normal. Here are two (one and two) good reads on what happened last week to mortgages.

Impact On The D.C. Area Economy

While not real estate specific, I want to share the excellent work of Jeannette Chapman, Director of the Stephen S. Fuller Institute at our very own George Mason University, which takes an in-depth look at how Coronavirus is likely going to impact the D.C. area economy, based on current projections. Notably, they determine that the D.C. area will not be as insulated from this recession as the 2008 financial crisis. Be smart, be careful with your money folks.

While I’m slightly off the topic of real estate, I wanted to share a great website for tracking global and domestic COVID-19 data in real time, with helpful visuals. This website was shared with me by Arlington resident/Mom Elissa David, who owns the Unbroken Body to help Moms heal their bodies after pregnancy. She has temporarily turned her website into a resource for all of us parents who have suddenly become home school teachers!

Now let’s jump into some relevant real estate market data.

Market Data

SUPPLY

The number of new listings this past week in Arlington jumped 27% over the same week last year and 6% over two weeks ago. The D.C. Metro experienced less dramatic increases in new listings, but increases nonetheless.

Anecdotally, it seems many homeowners who were planning to sell in the next 4-8 weeks are accelerating their timeline, fearing the uncertainty of the future economy. A boost in inventory from motivated sellers while demand continues to fall (see below) could lead to a drop in prices in the near future.

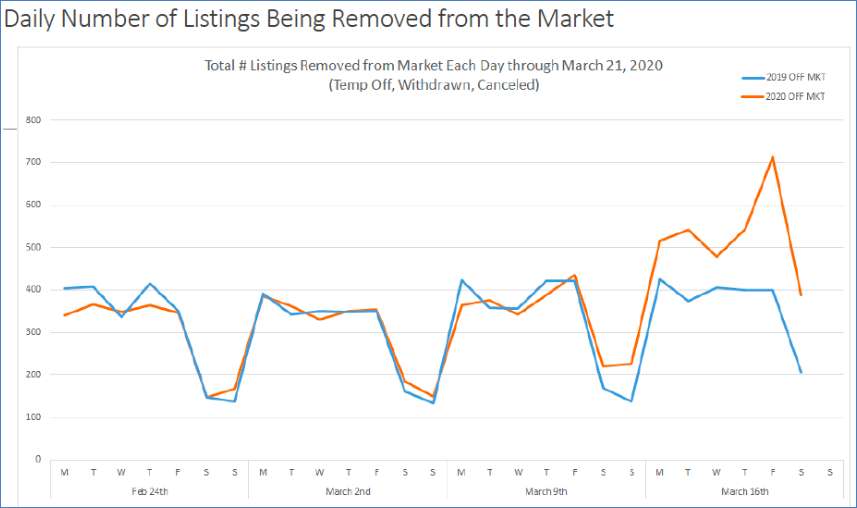

Nationwide, the number of listings pulled off the market spiked over the past week.

Nationwide Data

SHOWINGS

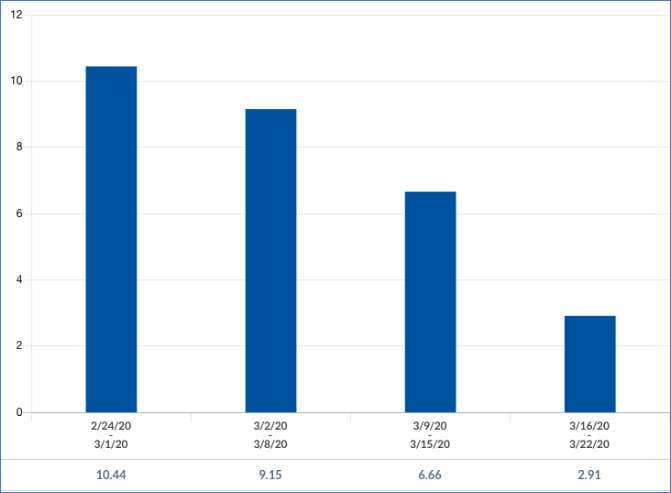

The average number of showings per listing in Arlington (first chart) have dropped each of the last four weeks from 10.44 showings four weeks ago to 2.91 showings this past week.

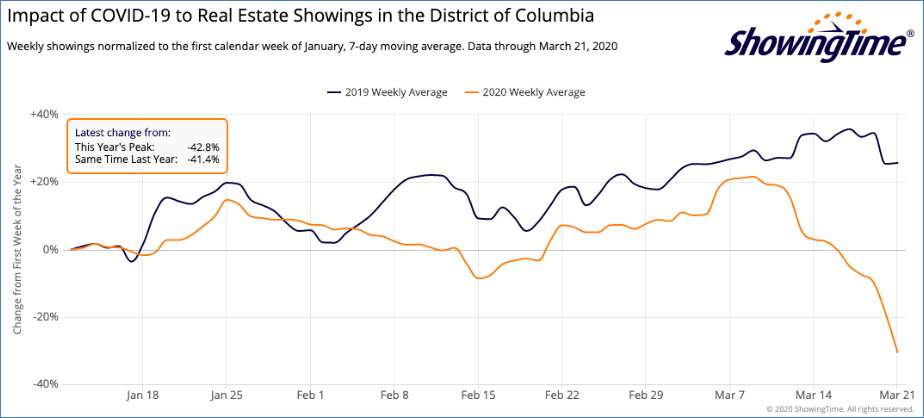

Showings in Washington, D.C. have dropped by 41.4% compared to this time last year. The tool I have to generate this data only offers statewide info, so I chose to use Washington, D.C. (yes, I know it’s not a state) instead of Virginia because the Washington, D.C. market is much more reflective of Northern Virginia than the Virginia market. Showings are down 32.9% across North America.

Arlington Data

CONTRACTS

While some buyers still find themselves competing with other offers, the amount of competition in the market is down significantly. From the first week of February through the first week of March (five weeks), 61% of homes listed for sale in Arlington went under contract within seven days.

Two weeks ago (first full week of our daily lives being disrupted by COVID-19), that dropped to 52%, and this past week only 33% of homes listed went under contract within seven days (that number will likely increase into the 40s over the next 2-3 days).

It’s worth noting that the market would normally be selling even faster this past week than it did the previous 5-6 weeks as we move into peak buyer demand season.

What Other Industry Service Providers Are Seeing

I spoke with some other industry service providers to see how their numbers looked over the past week. The title attorney and lender I spoke with saw a significant spike in the number of ratified purchase contracts they received. On the other hand, the inspector I work with saw their numbers drop dramatically.

INSPECTIONS

I spoke with Ken Humphreys, the Area Manager of Virginia and Maryland for BPG Inspections, one of the largest inspection companies in the country, and their total inspection in Virginia and Maryland were down 37% last week. They’re currently on pace to be down 45-50% this week.

TITLE

Sarah Anderson, Managing Attorney for Universal Title’s Arlington Office, shared with me that they received 35 contracts last week. They had received 75 contracts over the previous three weeks combined.

MORTGAGE

Jake Ryon, a Loan Officer with First Home Mortgage, told me that he’s been averaging 2.2 purchase contracts per week this year, and last week he received eight (crazy!).

A local lender I spoke with surveyed their appraisers on COVID-19 related questions and learned the following from 272 respondents:

35% are no longer performing interior inspections

43% are performing interior inspections but will likely stop if the situation deteriorates

22% anticipate being able to perform interior inspections with precautions for the duration of the situation

06% have heard from at least 1 borrower, realtor, or entry contact who will not permit the property to be inspected

Guidance?

While the future of public health and our economy are still extremely uncertain, the best anybody in the real estate industry can/should offer is a pulse on the current market with a very short-term outlook. Be wary of any advice you receive about what markets/life look like 3, 8, or 20+ weeks from now because nobody knows. Be especially wary of anybody promising that this will be a blip in the market and we’ll be back to normal come late summer (I’ve heard a lot of this talk).

In times like these, buying and investment decisions should be made based on long (5+ year) time horizons and you have to plan for best and worst case scenarios. If you’re considering selling your home, you have to acknowledge the massive amount of uncertainty even just a few weeks from now.

Be smart, be careful, be strategic. And stay home!

If you’d like a question answered in my weekly column or to set-up an in-person meeting to discuss local real estate, please send an email to [email protected]. To read any of my older posts, visit the blog section of my website at www.EliResidential.com. Call me directly at (703) 539-2529.

Eli Tucker is a licensed Realtor in Virginia, Washington D.C., and Maryland with RLAH Real Estate, 4040 N. Fairfax Dr. #10C Arlington, VA 22203, (703) 390-9460.

TORONTO – The Toronto Regional Real Estate Board says home sales in October surged as buyers continued moving off the sidelines amid lower interest rates.

The board said 6,658 homes changed hands last month in the Greater Toronto Area, up 44.4 per cent compared with 4,611 in the same month last year. Sales were up 14 per cent from September on a seasonally adjusted basis.

The average selling price was up 1.1 per cent compared with a year earlier at $1,135,215. The composite benchmark price, meant to represent the typical home, was down 3.3 per cent year-over-year.

“While we are still early in the Bank of Canada’s rate cutting cycle, it definitely does appear that an increasing number of buyers moved off the sidelines and back into the marketplace in October,” said TRREB president Jennifer Pearce in a news release.

“The positive affordability picture brought about by lower borrowing costs and relatively flat home prices prompted this improvement in market activity.”

The Bank of Canada has slashed its key interest rate four times since June, including a half-percentage point cut on Oct. 23. The rate now stands at 3.75 per cent, down from the high of five per cent that deterred many would-be buyers from the housing market.

New listings last month totalled 15,328, up 4.3 per cent from a year earlier.

In the City of Toronto, there were 2,509 sales last month, a 37.6 per cent jump from October 2023. Throughout the rest of the GTA, home sales rose 48.9 per cent to 4,149.

The sales uptick is encouraging, said Cameron Forbes, general manager and broker for Re/Max Realtron Realty Inc., who added the figures for October were stronger than he anticipated.

“I thought they’d be up for sure, but not necessarily that much,” said Forbes.

“Obviously, the 50 basis points was certainly a great move in the right direction. I just thought it would take more to get things going.”

He said it shows confidence in the market is returning faster than expected, especially among existing homeowners looking for a new property.

“The average consumer who’s employed and may have been able to get some increases in their wages over the last little bit to make up some ground with inflation, I think they’re confident, so they’re looking in the market.

“The conditions are nice because you’ve got a little more time, you’ve got more choice, you’ve got fewer other buyers to compete against.”

All property types saw more sales in October compared with a year ago throughout the GTA.

Townhouses led the surge with 56.8 per cent more sales, followed by detached homes at 46.6 per cent and semi-detached homes at 44 per cent. There were 33.4 per cent more condos that changed hands year-over-year.

“Market conditions did tighten in October, but there is still a lot of inventory and therefore choice for homebuyers,” said TRREB chief market analyst Jason Mercer.

“This choice will keep home price growth moderate over the next few months. However, as inventory is absorbed and home construction continues to lag population growth, selling price growth will accelerate, likely as we move through the spring of 2025.”

This report by The Canadian Press was first published Nov. 6, 2024.

HALIFAX – A village of tiny homes is set to open next month in a Halifax suburb, the latest project by the provincial government to address homelessness.

Located in Lower Sackville, N.S., the tiny home community will house up to 34 people when the first 26 units open Nov. 4.

Another 35 people are scheduled to move in when construction on another 29 units should be complete in December, under a partnership between the province, the Halifax Regional Municipality, United Way Halifax, The Shaw Group and Dexter Construction.

The province invested $9.4 million to build the village and will contribute $935,000 annually for operating costs.

Residents have been chosen from a list of people experiencing homelessness maintained by the Affordable Housing Association of Nova Scotia.

They will pay rent that is tied to their income for a unit that is fully furnished with a private bathroom, shower and a kitchen equipped with a cooktop, small fridge and microwave.

The Atlantic Community Shelters Society will also provide support to residents, ranging from counselling and mental health supports to employment and educational services.

This report by The Canadian Press was first published Oct. 24, 2024.

Housing affordability is a key issue in the provincial election campaign in British Columbia, particularly in major centres.

Here are some statistics about housing in B.C. from the Canada Mortgage and Housing Corporation’s 2024 Rental Market Report, issued in January, and the B.C. Real Estate Association’s August 2024 report.

Average residential home price in B.C.: $938,500

Average price in greater Vancouver (2024 year to date): $1,304,438

Average price in greater Victoria (2024 year to date): $979,103

Average price in the Okanagan (2024 year to date): $748,015

Average two-bedroom purpose-built rental in Vancouver: $2,181

Average two-bedroom purpose-built rental in Victoria: $1,839

Average two-bedroom purpose-built rental in Canada: $1,359

Rental vacancy rate in Vancouver: 0.9 per cent

How much more do new renters in Vancouver pay compared with renters who have occupied their home for at least a year: 27 per cent

This report by The Canadian Press was first published Oct. 17, 2024.

{kind=link}