(Bloomberg) — Australia’s economy contracted in the first three months of the year, setting up an end to a nearly 29-year run without a recession as an even deeper slowdown looms for the current quarter.

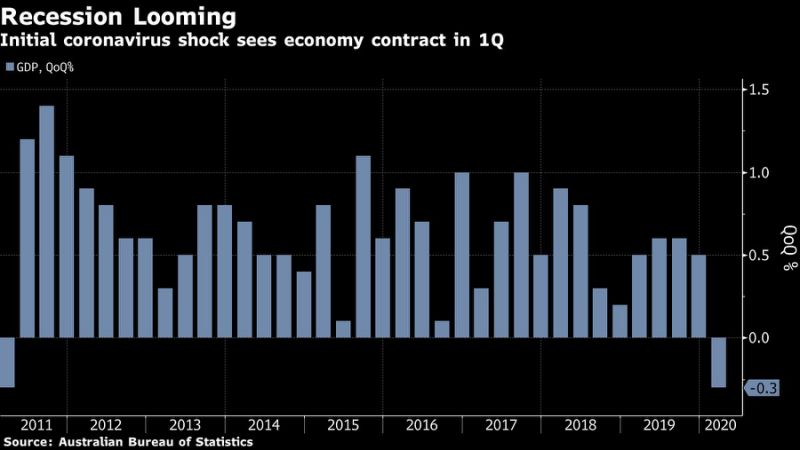

Gross domestic product fell 0.3% from the final three months of 2019, the first quarterly drop since 2011, brought down by a collapse in household spending, statistics bureau data showed in Sydney Wednesday. Economists had forecast a 0.4% drop. From a year earlier, the economy expanded 1.4%, matching estimates.

The Australian dollar edged a little lower after the release, and traded at 69.32 U.S. cents at 1:06 p.m. in Sydney.

The result sets up an end to Australia’s record run of avoiding two consecutive quarters of shrinking GDP, having dodged recessions during the 1997 Asian Financial Crisis, the Dot Com Bubble and the 2008 global financial crisis. The current quarter will see a deep contraction, with almost 600,000 jobs lost in April alone and much of the economy in lockdown to contain the coronavirus.

Treasurer Josh Frydenberg, speaking after the release, accepted this fate when asked directly whether the economy is now in recession.

“The answer to that is yes,” he told reporters. “That is on the basis of the advice that I have from the Treasury Department about where the June quarter is expected to be.”

Fiscal and monetary policy are working in tandem to rebuild the economy. The Reserve Bank of Australia has taken the cash rate near zero and lowered the cost of borrowing with its 0.25% bond yield target. The government has injected tens of billions of dollars into the economy to help tide businesses and households through the lockdown.

With the containment of the health crisis allowing activity to resume, the critical question is how quickly businesses can get back on their feet, workers regain employment and households resume spending.

“Growth should resume in the September quarter, but the impact of COVID-19 will surely cast a long and lingering shadow over the global economy and Australia’s recovery,” said Callam Pickering, an economist at global jobs website Indeed Inc. who previously worked at the central bank. “Continued support from fiscal and monetary policy will be necessary throughout 2020 and beyond.”

Today’s report showed:

Household spending tumbled 1.1%, shaving 0.6 percentage point off GDP, driven by a 2.4% drop in services expenditure. Restrictions particularity impacted spending on travel, hotels, cafes and restaurantsGovernment spending jumped 1.8%, adding 0.3 percentage point. Payments to provide support during the pandemic are expected to rise in the current quarterThe savings ratio advanced to 5.5% from a downwardly revised 3.5% in the fourth quarterDwelling construction fell 1.7%, reflecting continued weakness in approvalsNon-mining business investment fell 1.7%, while mining investment rose 3.6% as miners invest in new technologies and automation

Rising commodity prices are boosting miners’ profitability, with the terms of trade 2.9% higher in the first three months of 2020, pushing the current account surplus to a record A$8.4 billion ($5.8 billion). Yet, miners will be keeping a watchful eye on the nation’s currency, which has surged almost 20% in the past two-and-a-half months.

What Bloomberg’s Economists Say

“Typically backward looking national accounts releases contain an array of hidden trends that are often overlooked. Mining investment has climbed to a 7-year high, Australia’s terms of trade have risen and exploration intentions are elevated. This bodes well for the recovery.”

James McIntyre, economist

The economic outlook is improving as the restrictions are lifted, but will continue to be constrained by closed borders that are hitting tourism and education exports. The government is discussing a fresh round of fiscal stimulus to try to put residential construction back on its feet.

(Updates with Treasurer and economist comments)

<p class="canvas-atom canvas-text Mb(1.0em) Mb(0)–sm Mt(0.8em)–sm" type="text" content="For more articles like this, please visit us at bloomberg.com” data-reactid=”45″>For more articles like this, please visit us at bloomberg.com

<p class="canvas-atom canvas-text Mb(1.0em) Mb(0)–sm Mt(0.8em)–sm" type="text" content="Subscribe now to stay ahead with the most trusted business news source.” data-reactid=”46″>Subscribe now to stay ahead with the most trusted business news source.

©2020 Bloomberg L.P.