Right now, increasingly many market pundits and media outlets are turning very negative on real estate.

Here are just a few examples:

Charlie Munger recently said:

“A lot of real estate isn’t so good anymore. We have a lot of troubled office buildings, a lot of troubled shopping centers, a lot of troubled other properties. There’s a lot of agony out there.” – Charlie Munger

Kevin O’Leary said:

“Regional banks. About 20-25% of their portfolio is in commercial real estate and a lot of it is underwater. So there is going to be a lot of consolidation among owners of real estate because they don’t have enough equity in their portfolios… So yes, a big correction coming…” – Kevin O’Leary

Elon Musk:

“We really haven’t seen the commercial real estate shoe drop. That’s more like an anvil, not a shoe… So the stuff we’ve seen thus far actually hasn’t even — it’s only slightly real estate portfolio degradation. But that will become a very serious thing later this year, in my view.”–Elon Musk

And there are many others.

In short, they claim that:

The office market is collapsing and could hurt other property sectors.

The surge in interest rates will lead to a significant cap rate expansion.

The banking crisis will only make it harder for landlords to refinance.

This sure seems like a perfect storm. Is now the time to sell real estate, and by extension, is it time to sell REITs as well?

Let us review one by one the most popular bear theses for real estate and see how they apply to the REIT sector. Finally, I will share my conclusion and highlight a few REITs to sell and a few opportunities for you to consider buying.

1. The office market is collapsing and this could hurt other property sectors

The office sector is in for a lot of pain.

That’s not a secret to anyone.

Office utilization rates still haven’t recovered from the pandemic, occupancy rates are plummeting, and tenants are able to negotiate large TI packages and/or significant rent cuts.

This also doesn’t appear to be changing any time soon. Workers now demand hybrid work conditions or they simply leave the company for another. They don’t want to return to 5 days a week at the office in a cubicle and so there’s likely a lot more pain to come.

But the office sector is just one property sector among many others. It only represents 5% of the REIT market. The other 95% invest in:

Apartment communities

Single-family rentals

Manufactured housing communities

Timberland

Farmland

Strip centers

Warehouses

Factories

Cell towers

Data centers

Billboards

Casinos

Net lease properties

Self storage

Etc…

So the big question is how will the pain of the office sector affect these other property sectors.

Many fear that work-from-home will have a cascading negative impact on other properties. As an example, if fewer people are going to work in Manhattan, then fewer people will also visit the retail stores in the vicinity of the office buildings. The apartments there may also drop in demand. Finally, if Zoom (ZM) can replace meetings, hotels may see a drop in business travel.

That’s really what’s getting all the attention today. It is negative and the media loves negative stories.

But the reality is more complex than that because there are always winners when there are losers. In fact, many property sectors are actually benefiting from work-from-home:

Self-storage is experiencing a boom in demand as people make space for home offices.

Public Storage

Apartments in the suburbs, especially in sunbelt markets, are also growing in demand as increasingly many people decide to move out of cities into more affordable, safer, and tax-friendlier suburbs.

Mid-America Communities

Single-family rentals also benefit as people suddenly want more space as they work from home.

Invitation Homes

Resort-type hotels are also benefiting as people have gained greater geographical freedom and can leave for longer weekends on a regular.

Host Hotels

Then some manufactured housing communities benefit from people who decide to go full-remote and relocate to more affordable locations with plenty of nature.

Sun Communities

Timberland benefits as we face a housing crisis and a lot more needs to be built to meet the growing demand.

Weyerhaeuser

Cell towers profit as the consumption of data only grows as a result of work-from-home. Data centers also benefit in a similar way.

<img src=”https://static.seekingalpha.com/uploads/2023/8/20/saupload_1_z2k79Wvq5UPTdNChfSAx6g.png” alt=”American Tower (AMT): tesis de inversión | by Eloy “Snowball” | Medium” contenteditable=”false” loading=”lazy”>

American Tower

Suburban strip centers and malls benefit from greater traffic during off-hours as people become more flexible with their schedules. As an example, someone may not have had time to go to the gym with his/her previous work schedule but things have now changed for the better.

Kimco

The point here is that many more property sectors actually benefit than hurt from the growing trend of work-from-home. Yet, the market only focuses on the negatives.

The key as an investor is to invest in the property sectors that benefit from work-from-home before the market recognizes it.

2. The surge in interest rates will lead to significant cap rate expansion

Some cap rate expansion is expected and has already occurred. This is bad news since higher cap rates lead to lower property values, all else held equal.

But we are yet to see any significant cap rate expansion and this is because interest rates are just one piece of the puzzle.

Yes, if you keep all other assumptions constant, then higher interest rates would justify higher cap rates, but that’s not the world we live in.

The surge in interest rates was the direct result of high inflation, and what happens when inflation surges?

People seek refuge in real assets.

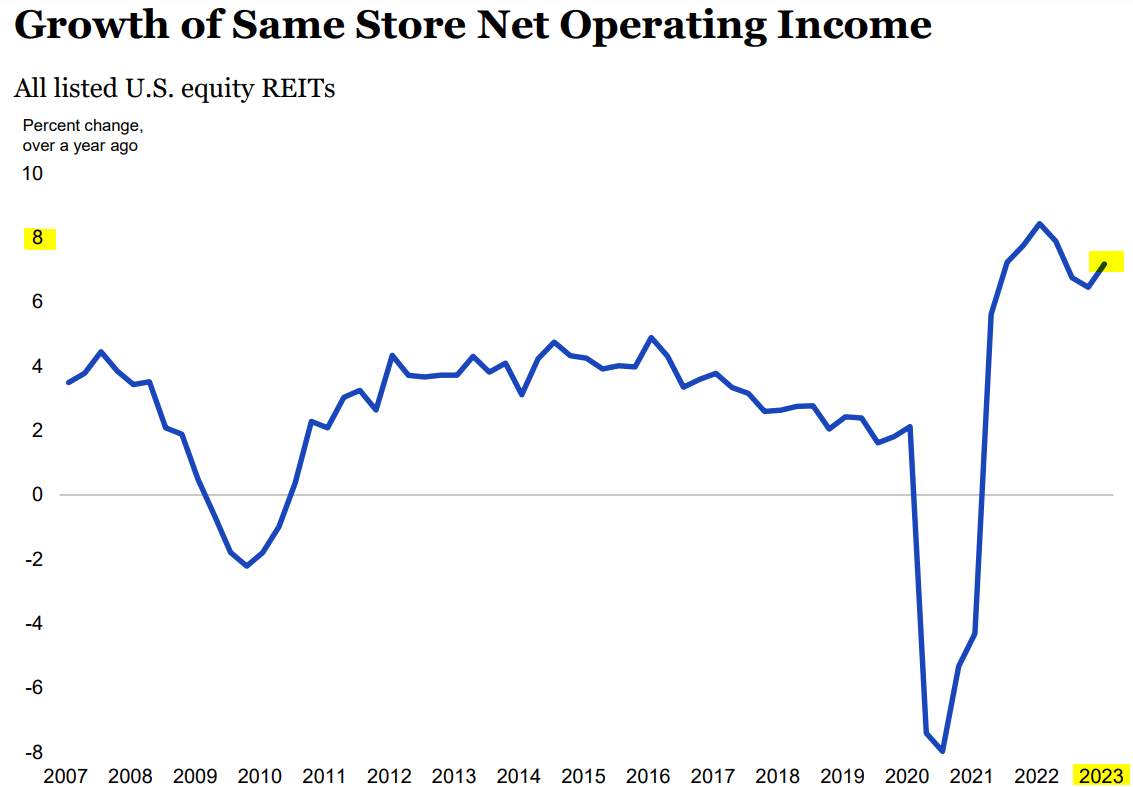

They are willing to accept somewhat lower cap rates (relative to interest rates) because they know that inflation will result in faster rent growth and this is exactly what has happened:

NAREIT

So investors will accept a lower initial yield in exchange for inflation protection and faster future growth. This is why cap rates remain persistently low relative to interest rates. Sure, you now could invest in Treasuries and earn a much higher yield, but what’s the point if your “real yield” is negative after inflation and taxes?

Again, that explains why people aren’t rushing away from real estate.

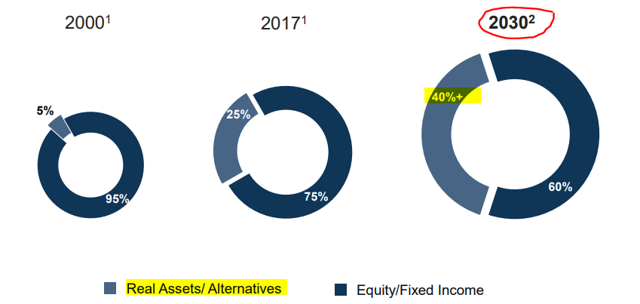

The second point to consider here is that asset allocations have changed drastically over the past decades and we are not going back.

Institutional investors have realized that including real assets in a portfolio helps them reduce risk via diversification, increase yield, and hedge against inflation and some other black swans.

The allocations to real assets have grown from 5% in 2000 to 25% today and it is expected to rise closer to 40% by 2030.

Brookfield

Today, there is more cash in real estate funds that’s waiting to be deployed than ever before, and by 2030, there will be many more trillions of additional capital chasing a limited number of assets.

With that in mind, I think that it is very unlikely that we see any significant cap rate expansion, especially in popular property sectors like industrial and multifamily.

3. The banking crisis will only make it harder for landlords to refinance

This is true in some cases.

There are a lot of office buildings that were purchased with too much debt leading up to the pandemic and refinancing these deals will be very problematic.

Brookfield (BAM) and Blackstone (BX) have already returned the keys of some office buildings to their lenders because their equity value had turned negative.

But generally speaking, this does not apply to other property sectors, and especially not to REITs because:

REIT balance sheets are today the strongest they have ever been with LTVs as low as 30% on average.

REITs own top-quartile properties.

REITs focus on desirable property sectors.

The 3 bank failures are not reflective of most banks.

This is nothing like 2008-2009.

REITs have today many more alternative capital sources.

The response by the government has been swift and strong.

The Fed is so confident that it has even kept hiking interest rates.

JPMorgan’s (JPM) Jamie Dimon himself recently said that the banking sector is “extraordinarily sound” and that it was “getting near the end” of recent troubles. He also noted that the current conditions were “nothing like 2008 and 2009 for a lot of different reasons”.

J.P Morgan

Put simply, the few recent bank failures were primarily the result of poor management in the face of a historic surge in interest rates, which led to large losses and eventually, sparked a bank run on deposits.

It is not a systemic problem and therefore, the “banking crisis” shouldn’t have a major impact on most landlords, especially REITs.

If anything, this could benefit some REITs as they are able to pick up some properties at firesale prices as overleverage private equity players default on some of their holdings.

The Opportunity: the devil lies in the details

Investors have been quick to extrapolate these narratives across the entire REIT sector and it explains why they have crashed in value over the past year:

Nothing was immune to the collapse, not even the strongest REITs that enjoy fortress balance sheets and rapidly growing cash flows.

They all dropped in association with the highly leveraged office REITs that are facing severe pain.

We think that this is an exceptional opportunity.

The market has painted all REITs with the same brush, not understanding that this is a vast and versatile sector with some winners and some losers.

To give you a few examples:

I probably wouldn’t buy a NYC-focused office REIT that’s heavily leveraged like SL Green (SLG) despite its low valuation. The pain could persist for a long time to come and this could easily turn it into a value trap.

SL Green

On the flip side, I will happily invest in a Texas-focused apartment REIT like BSR REIT (OTCPK:BSRTF / HOM.U), which enjoys rapidly growing rents and has a strong balance sheet, but is now priced at a 37% discount to its net asset value following the recent crash. The implied cap rate based on normalized NOI is now in the 6.5-7% range, but these assets continue to trade at a 4.5-5% range in the private market. The huge discount provides both: margin of safety and significant upside potential. Just to return to its net asset value, it would need to rise by 75%, and a year ago, it was actually priced at a premium to it.

BSR REIT

The low valuation may be deserved in the case of SLG, but it isn’t in the case of BSR, and quite frankly, I think that some of these opportunities are truly exceptional.

If you were offered to buy Texan apartment communities at ~60 cents on the dollar, net of debt, you would likely jump on the opportunity, but there is so much fear in today’s market that most investors are failing to see these opportunities.

Closing Note: follow the smart money

All while the unsophisticated investors ran away from REITs, the big private equity groups have been loading up on them.

Blackstone (BX) has bought about $30 billion worth of REITs since the beginning of 2022. Starwood, another major private equity group, has also been buying REITs, and here is what its CEO, billionaire Barry Sternlicht, said in a recent interview:

“By the way, when credit comes back, you are gonna see REITs take off… There are some unbelievable bargains in REITs. We did the same thing during the pandemic. We bought a dozen stocks all over the world and we had a 70% IRR on that stuff. We are already buying some stuff in the public market…” – Barry Sternlicht, CEO/Chairman, Starwood Q3 2023 CNBC Interview

The key is to be selective and buy those REITs that have been unfairly beaten down and wait patiently for the recovery.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

TORONTO – The Toronto Regional Real Estate Board says home sales in October surged as buyers continued moving off the sidelines amid lower interest rates.

The board said 6,658 homes changed hands last month in the Greater Toronto Area, up 44.4 per cent compared with 4,611 in the same month last year. Sales were up 14 per cent from September on a seasonally adjusted basis.

The average selling price was up 1.1 per cent compared with a year earlier at $1,135,215. The composite benchmark price, meant to represent the typical home, was down 3.3 per cent year-over-year.

“While we are still early in the Bank of Canada’s rate cutting cycle, it definitely does appear that an increasing number of buyers moved off the sidelines and back into the marketplace in October,” said TRREB president Jennifer Pearce in a news release.

“The positive affordability picture brought about by lower borrowing costs and relatively flat home prices prompted this improvement in market activity.”

The Bank of Canada has slashed its key interest rate four times since June, including a half-percentage point cut on Oct. 23. The rate now stands at 3.75 per cent, down from the high of five per cent that deterred many would-be buyers from the housing market.

New listings last month totalled 15,328, up 4.3 per cent from a year earlier.

In the City of Toronto, there were 2,509 sales last month, a 37.6 per cent jump from October 2023. Throughout the rest of the GTA, home sales rose 48.9 per cent to 4,149.

The sales uptick is encouraging, said Cameron Forbes, general manager and broker for Re/Max Realtron Realty Inc., who added the figures for October were stronger than he anticipated.

“I thought they’d be up for sure, but not necessarily that much,” said Forbes.

“Obviously, the 50 basis points was certainly a great move in the right direction. I just thought it would take more to get things going.”

He said it shows confidence in the market is returning faster than expected, especially among existing homeowners looking for a new property.

“The average consumer who’s employed and may have been able to get some increases in their wages over the last little bit to make up some ground with inflation, I think they’re confident, so they’re looking in the market.

“The conditions are nice because you’ve got a little more time, you’ve got more choice, you’ve got fewer other buyers to compete against.”

All property types saw more sales in October compared with a year ago throughout the GTA.

Townhouses led the surge with 56.8 per cent more sales, followed by detached homes at 46.6 per cent and semi-detached homes at 44 per cent. There were 33.4 per cent more condos that changed hands year-over-year.

“Market conditions did tighten in October, but there is still a lot of inventory and therefore choice for homebuyers,” said TRREB chief market analyst Jason Mercer.

“This choice will keep home price growth moderate over the next few months. However, as inventory is absorbed and home construction continues to lag population growth, selling price growth will accelerate, likely as we move through the spring of 2025.”

This report by The Canadian Press was first published Nov. 6, 2024.

HALIFAX – A village of tiny homes is set to open next month in a Halifax suburb, the latest project by the provincial government to address homelessness.

Located in Lower Sackville, N.S., the tiny home community will house up to 34 people when the first 26 units open Nov. 4.

Another 35 people are scheduled to move in when construction on another 29 units should be complete in December, under a partnership between the province, the Halifax Regional Municipality, United Way Halifax, The Shaw Group and Dexter Construction.

The province invested $9.4 million to build the village and will contribute $935,000 annually for operating costs.

Residents have been chosen from a list of people experiencing homelessness maintained by the Affordable Housing Association of Nova Scotia.

They will pay rent that is tied to their income for a unit that is fully furnished with a private bathroom, shower and a kitchen equipped with a cooktop, small fridge and microwave.

The Atlantic Community Shelters Society will also provide support to residents, ranging from counselling and mental health supports to employment and educational services.

This report by The Canadian Press was first published Oct. 24, 2024.

Housing affordability is a key issue in the provincial election campaign in British Columbia, particularly in major centres.

Here are some statistics about housing in B.C. from the Canada Mortgage and Housing Corporation’s 2024 Rental Market Report, issued in January, and the B.C. Real Estate Association’s August 2024 report.

Average residential home price in B.C.: $938,500

Average price in greater Vancouver (2024 year to date): $1,304,438

Average price in greater Victoria (2024 year to date): $979,103

Average price in the Okanagan (2024 year to date): $748,015

Average two-bedroom purpose-built rental in Vancouver: $2,181

Average two-bedroom purpose-built rental in Victoria: $1,839

Average two-bedroom purpose-built rental in Canada: $1,359

Rental vacancy rate in Vancouver: 0.9 per cent

How much more do new renters in Vancouver pay compared with renters who have occupied their home for at least a year: 27 per cent

This report by The Canadian Press was first published Oct. 17, 2024.