Article content

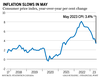

Inflation in Canada slowed in May to 3.4 per cent, matching economist estimates, but many don’t think that will be enough to convince the Bank of Canada to back away from another interest rate hike at its next meeting on July 12.

Inflation accelerates in May to 3.4 per cent, the slowest pace since June 2021

Inflation in Canada slowed in May to 3.4 per cent, matching economist estimates, but many don’t think that will be enough to convince the Bank of Canada to back away from another interest rate hike at its next meeting on July 12.

May’s consumer price index (CPI) increase was the smallest since June 2021, Statistics Canada said in a release on June 27. The CPI slowed a full percentage point from an unexpected acceleration in April of 4.4 per cent. Monthly inflation grew 0.4 per cent in May, or 0.1 per cent on a seasonally adjusted basis.

“The Bank (of Canada) will still be pleased to see that the CPI rose by just 0.1 per cent month over month this May and that the monthly gains in CPI-trim and CPI-median (the bank’s preferred inflation measures) each slowed to 0.2 per cent,” Stephen Brown, deputy chief North American economist at Capital Economics, said in a note.

There were other signs of inflation retreating, Charles St-Arnaud, chief economist with Alberta Central, said in a note.

For example, the number of components included in the CPI that rose between three and five per cent in May continued to shrink meaning inflation is less broad-based in the economy, St-Arnaud said.

However, economists said the year-over-year readings for the Bank of Canada’s preferred inflation measures remain stuck well above the bank’s two per cent target.

“No matter how you slice it, inflation remains a serious issue for the BoC,” Benjamin Reitzes of BMO Economics said in a note.

Prior to the inflation release, markets were pricing in a 70 per cent chance of an increase at the central bank’s July meeting. Post-announcement, that fell to 60 per cent, according to Bloomberg.

There is still plenty of important data to come that will factor into the Bank of Canada’s decision-making on July 12 including GDP for April and the central bank’s Business Outlook Survey, both out on June 30. The June jobs report will be released on July 7.

Here’s what economists are saying about the latest inflation numbers and what they could mean for the Bank of Canada.

“While the steep declines in both headline and core inflation in May were partly due to favourable base effects, the monthly gains in each also slowed compared to April. That probably won’t be enough to persuade the Bank of Canada to stand pat at its meeting next month, but it does add to our sense that the bank will not be forced to raise interest rates beyond five per cent, implying just one more 25 basis-point hike.

“Canadian inflation continued to cool in May, but progress is unlikely to be enough to prevent the Bank of Canada from raising rates in July. Improvements in core inflation are slow, particularly on the services side, with inflation picking up in discretionary areas like travel services and restaurant meals (6.8 per cent year over year in May). Cooler goods inflation is welcome, but the BoC has likely been counting on that already as supply chain snarls improve.

“Looking at the bank’s core measures, governor (Tiff) Macklem may have a Bon Jovi earworm, humming, ‘whoa, we’re half way there.’ But, there is still a ways to go to get inflation all the way back to two per cent. And the bank would rather not be ‘livin’ on a prayer,’ and is likely to take rates another quarter point higher in July to ensure demand, and hence price pressures cool further.”

“While the softer-than-expected core prints are a bit of good news, every inflation metric remains far above the two per cent inflation target. Accordingly, Bank of Canada policymakers won’t breathe a huge sigh of relief after this report as core inflation remains sticky and has yet to show signs of a durable slowdown. The odds of a July rate hike might be slightly lower now, but if the rest of the data hold up over the next two weeks, a hike still looks likely.”

“The breadth of inflation fell, with around half of the components running above target in May, compared to roughly three-quarters when averaged over the past three months. This could be an early sign of cooling price pressures after months of re-acceleration, but the fact remains that the monthly pace of price increases was still twice as strong as it would be if inflation were back to normal and the underlying core measures remain too high for comfort. For this reason, we do not think this single improved report is enough to prevent the Bank of Canada from hiking rates again in July, but it reduces the risk that they will take the overnight rate above five per cent. This merely confirms our view on the BoC’s implied rate path, with the risk of inaction at July’s meeting now centred on the data released over the next two weeks.”

“The ‘headline’ inflation rate is likely to fall further in June – potentially down to the top end of the Bank of Canada’s one per cent to three per cent target range – as energy prices this year continue to compare to very high year-ago levels. Beyond that, further slowing in broader inflation readings all the way back to the two per cent target will be much harder to come by.

“Although slowing, underlying inflation trends in Canada are still running well-above the BoC’s two per cent target. Higher interest rates are cutting into household purchasing power, but spending to-date has been firm. Labour market conditions are also more resilient than expected in 2023 to-date. GDP data and the BoC’s own Q2 Business Outlook Survey later this week will be watched closely for signs that the economy is losing momentum. But absent a large downside surprise from those data releases, we continue to expect the bank to hike the overnight rate by another 25 basis points in July, before stepping back the sideline for the rest of this year.”

“Inflation continues to moderate but remains well above the BoC’s target of two per cent, while inflation expectations remain elevated and inflationary pressures remain broad and likely sticky. The BoC is likely to consider the recent inflation dynamic, as measured by the three-month annualized changes, slightly concerning and could support another increase in interest rates at the July meeting.

“However, higher interest rates are having a significant impact on inflation. We estimate that inflation excluding food, energy and mortgage interest payments is about 2.3 per cent and its three-month over three-month annualized change is around 2.5 per cent. This means that excluding the impact of the rate hikes, underlying inflation is in line with the BoC’s target and would not support further rate increases.

“Ultimately, whether the BoC hikes in July may hinge on the strong momentum in the economy, with the strong labour market and consumer spending, and the desire of the BoC to restore its credibility as an inflation fighter and influence inflation expectations.”

“Inflation is coming in lower than expected for May 2023. The month-over-month variation (0.4 per cent) is more indicative of the remaining inflation than the year-over-year variation due to the inflationary spike of May 2022. The pressure on prices is coming from service industries: strong service consumption is driving demand and constrained labour is impairing supply. It remains a coin toss whether the Bank of Canada will implement an additional hike in July.”

Digital platforms like Uber, Airbnb and Etsy have made it easier than ever to make some extra cash on the side, but experts say you need to be diligent about tracking and reporting that additional income, or risk the consequences.

“Especially in the first year … make sure that if you’re not familiar with how to report self-employed income, seek assistance and get it right, rather than take the risk of getting it wrong. It’ll take a lot longer and cost a lot more to fix it,” said Bruce Goudy, director of BDO Canada’s indirect tax practice.

More and more Canadians are earning income from websites and apps, whether they’re renting out a property on Airbnb, delivering food through Uber Eats, or doing graphic design on Fiverr.

In December 2023, 927,000 people ages 15 to 69 years old said they had earned money from a digital platform in the preceding year, said Statistics Canada. This included platforms that pay workers directly and those that connect workers with clients.

If you earn money through a digital platform, you are considered self-employed, said Stefanie Ricchio, a chartered professional accountant and spokesperson for TurboTax Canada.

Instead of the standard T4 tax form you get from an employer, you’ll need to report your self-employment income on a T2125 form when you file your taxes.

As well as your income, you also need to report your expenses, said Ricchio. These expenses can include home office costs, car maintenance, and even the fees you pay to the digital platform — there are hundreds of deductions available, she said.

“The more eligible deductions that you apply to that income, the less that tax bill is going to be when you file.”

Because you’re generally not collecting taxes when you earn money on a digital platform, you need to be prepared to pay those taxes when you file, said Ricchio. She recommends setting aside about a quarter of your income for this purpose.

For those who are new to being self-employed, it can require a big mindset change, she said.

Once you’re earning $30,000 or more over four consecutive quarters, you have to register for a GST/HST account, said Ricchio, though you can voluntarily do it earlier.

But if you are providing rideshare services, you have to sign up right at the beginning, she said.

“It’s immediate because you start charging GST, HST immediately.”

This threshold might take some sellers by surprise, said Goudy, which is why it’s important to monitor your revenues closely so you’re not caught off guard.

Goudy noted that since Canada has several different sales tax jurisdictions, sellers should make sure they’re aware of those implications — tax obligations are based on where the customer is located, not the seller.

Canada recently introduced new reporting rules for digital platform operators, which came into effect this year. The rules themselves target the platforms, but could affect people working through those platforms too.

Certain platforms are now required to collect and report information to the Canada Revenue Agency on sellers who live in Canada or in countries that have implemented the same rules, and who sell to people in Canada or those countries, according to the CRA. This information may include identifying details like names and addresses, platform fees, property locations (if applicable) and payment details.

“What pre-empted this is obviously the rise of e-commerce, digital, the digital transaction community,” said Ricchio.

“They know that they have been missing transactions that have gone unknown to the CRA … so this is now the mechanism to help them capture it, to ensure that everyone is paying tax where they should be on that income.”

Sellers may be asked for additional information so the platform can fulfil these obligations, the agency added.

If a seller doesn’t provide their tax identification information to the platform, they can be fined $500, the CRA said.

Certain sellers are excluded from these obligations, including those with “less than 30 relevant activities for the sale of goods” and for whom the total amount paid or credited was below $2,800 during the reportable period, according to the CRA.

Sellers need to make sure they do their due diligence and comply with all their reporting requirements, said Goudy, as what they file has to match what the platform reports.

Non-compliance can result in penalties, he said, as well as any penalties or interest on unpaid taxes.

“The CRA is going to be able to cross-check this information readily available,” he said.

“If the sellers were not compliant before … then it’s going to be pretty obvious.”

Another change this year is that if you operate a short-term rental in a designated province or municipality where you’re not allowed to do so, the CRA will disqualify your business deductions, said Ricchio.

If you’re earning digital platform income on top of your regular employment income, Ricchio said the extra money could potentially push you into a higher tax bracket.

This will not only affect your rate of taxation but could also hit any benefits you’re used to receiving, such as the Canada Child Benefit or the GST/HST credit, she said. “That’s also sometimes a shock for people.”

This report by The Canadian Press was first published Oct. 17, 2024.

BURNABY, B.C. – Interfor Corp. is selling its three manufacturing facilities in Quebec and closing its corporate office in Montreal as the lumber producer plans to leave the province and focus on other parts of the company.

Interfor chief executive Ian Fillinger says the decision to exit its Quebec operations was influenced by recent developments that have restricted the availability of economic fibre, including record forest fires in 2023.

The company says it has signed a deal to sell its sawmills in Val-d’Or and Matagami as well as its Sullivan remanufacturing plant in Val-d’Or, along with all associated forestry and business operations, to Chantiers Chibougamau Ltée (CCL) for $30 million in cash.

Interfor and CCL will also enter into a multi-year contract for the supply of machine stress rated lumber to Interfor’s I-Joist engineered wood products facility in Sault Ste. Marie, Ont.

Interfor says it expects to take an impairment charge in its third quarter associated with the announcement.

The sale does not include any countervailing or anti-dumping duty deposits related to the ongoing U.S.-Canada softwood lumber trade dispute.

This report by The Canadian Press was first published Oct. 16, 2024.

Companies in this story: (TSX:IFP)

The Canadian Press. All rights reserved.

TORONTO – TD Bank Group says The Charles Schwab Corp.’s third-quarter results are expected to translate into about $178 million of reported equity in net income for the Canadian bank’s fourth quarter.

TD says that excluding about $2 million after-tax in acquisition-related charges and $27 million after-tax in amortization of acquired intangibles, its adjusted equity in net income from its investment in Schwab will be $207 million.

TD is expected to release its full fourth-quarter results on Dec. 5.

Schwab, which keeps its books in U.S. dollars, reported Tuesday a third-quarter profit of US$1.41 billion, up from US$1.13 billion a year earlier.

On an adjusted basis, Schwab says it earned US$1.53 billion in its latest quarter compared with US$1.52 billion in the same quarter last year.

TD announced in August that it had sold 40.5 million Schwab shares. The sale reduced its interest in Schwab to 10.1 per cent from 12.3 per cent.

This report by The Canadian Press was first published Oct. 16, 2024.

Companies in this story: (TSX:TD)

The Canadian Press. All rights reserved.

Defying Convention to Deepen Connections: Booking.com’s 8 Travel Predictions for 2025

After hurricane, with no running water, residents organize to meet a basic need

Canadian men to face Suriname in CONCACAF Nations League quarterfinal

Argonauts players Kelly, McManis earn CFL top performer awards

N.B. election debate: Tory leader forced to defend record on gender policy, housing

Buhai, Green and Shin lead in South Korea after 8-under 64s in first round

In The Rings: Curling Canada still looking for Canadian Curling Trials title sponsor

Alberta government shifts continuing care from Health to Seniors Ministry

Comments

Postmedia is committed to maintaining a lively but civil forum for discussion and encourage all readers to share their views on our articles. Comments may take up to an hour for moderation before appearing on the site. We ask you to keep your comments relevant and respectful. We have enabled email notifications—you will now receive an email if you receive a reply to your comment, there is an update to a comment thread you follow or if a user you follow comments. Visit our Community Guidelines for more information and details on how to adjust your email settings.

Join the Conversation