Cognitive dissonance has hit the real estate market as people simultaneously love real estate and hate REITs. Physical real estate properties are presently selling for all-time highs while the REITs that own them are selling at fear mongering, recession level multiples. We discussed the cheapness of share prices more thoroughly here, but today I want to discuss the expensiveness of the physical real estate.

When these two facts are put together it creates a rather odd opportunity in which one can buy a REIT at 70 cents on the dollar and then sell its assets at full price.

Allow me to begin by taking a look at a variety of actual real estate transactions.

Real world transactions

The office market has been written off as dead, but big money has come in and paid quite a price tag in the recent SL Green (SLG) Office sale.

“New York City’s largest office landlord, said on Monday it sold a 49.9% stake in 245 Park Avenue to a U.S. affiliate of Mori Trust Co. Ltd. at a gross asset valuation of $2.0B.”

I highly doubt Mori Trust spent a billion dollars without doing extensive homework. This particular deal came in at about flat to SLG’s cost basis, but that is far better than what the market is pricing in.

Office is of course the most fundamentally troubled REIT sector and as we move on to other sectors I think it is clear that real estate values are up substantially.

“It has completed the sale of an unfarmed parcel in Florida for $9.6 million. This provided a 343% return on investment and resulted in a capital gain of approximately $6.4 million.”

As this particular land was unfarmed it had no revenues associated with it making the sale clearly accretive to shareholder value. The 343% return on investment was made possible by the HBU style of the sale as this land was well located for development. As such it is not indicative of general farmland throughout the country.

However, a series of sales from Farmland Partners (FPI) demonstrates that farmland has broadly appreciated to all-time highs even when it is sold to remain as farmland.

“Farmland Partners Inc. announced that it sold 862 acres of farmland in White County, Arkansas, for $3.7 million – an approximate gain of 24% over net book value.”

announced that it sold 2,426 acres of farmland in Nebraska and South Carolina to the tenants who rented the properties. The transactions totaled $16.2 million and represented a total gain on sale of more than $3.1 million, or approximately 24% over net book value.”

announced that it has sold 1,370 acres of farmland stretching across four farms in Arkansas, Georgia, Illinois, and South Carolina. The transactions totaled $8.9 million and resulted in a cumulative gain on sale of $3.7 million – approximately 73% over net book value.”

“farmland transactions include sale of ~$19.9M worth of seven farms, which helped the company achieve a gain of more than 26%.”

Keep in mind that in GAAP accounting, farmland does not depreciate. So a 26% gain on sale literally means they sold it for 26% more than they bought it for.

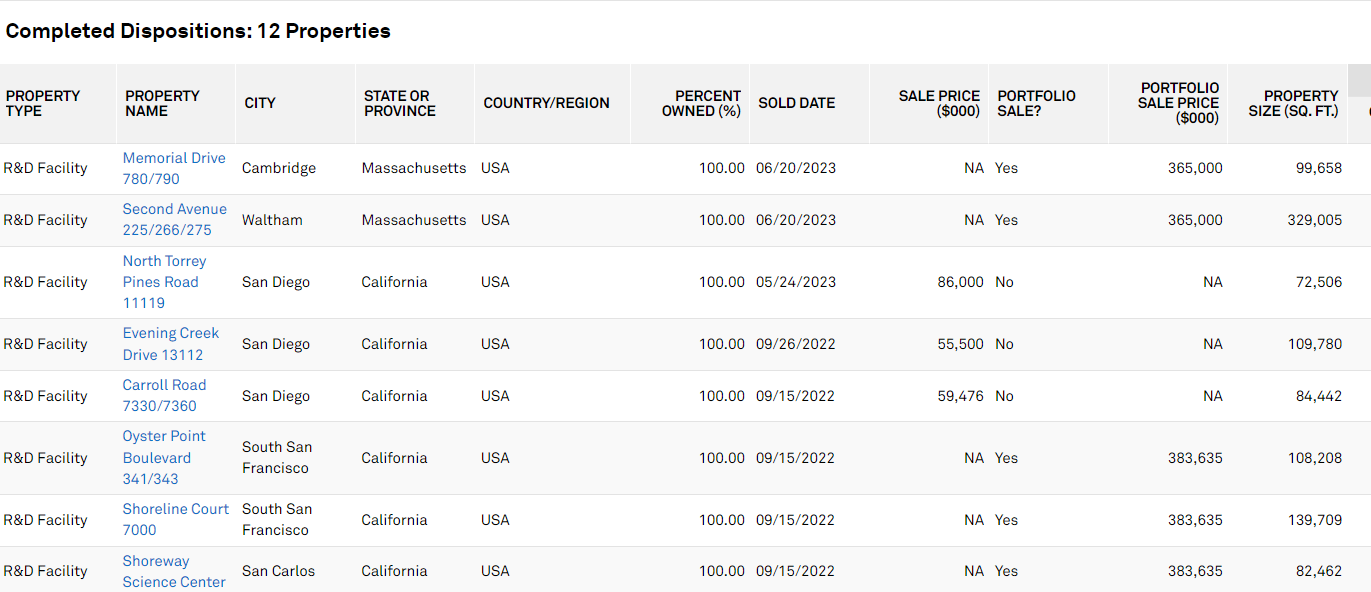

Life Science Real Estate Gains

Alexandria (ARE) has been an active seller to internally fund its development pipeline. Even as ARE stock is surrounding by doom and gloom, the company’s AFFO/share continues to rise at a good clip, rental rates are increasing and their disposition activity shows a clear demand for life science real estate.

S&P Global Market Intelligence

That is $1.015 Billion of sales at an average sale price of $989 per square foot and a cap rate in the high 4s. Why might one buy at a cap rate in the 4s when parts of the Treasury curve are north of 5%?

Because the buyers anticipate long term growth.

Multifamily real estate

Apartments have raised rents substantially over the past few years which has taken property values to close to all-time highs.

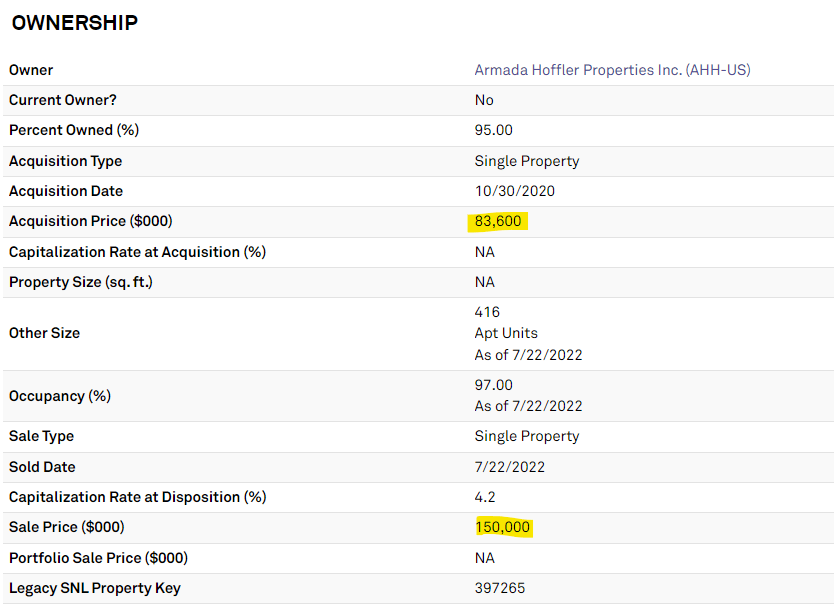

Armada Hoffler (AHH) sold Annapolis Junction for $150 million. Records show a cost basis of $83.6 million highlighted below.

S&P Global Market Intelligence

The sale price represents a 4.2% exit cap rate.

Industrial

So far it has been REITs selling, but in this instance, it is a REIT buying. Prologis (PLD) recently bought $3.1B of industrial real estate at a 4% cap rate.

“Prologis to acquire nearly 14 million square feet of industrial properties from opportunistic real estate funds affiliated with Blackstone for $3.1 billion, funded by cash. The acquisition price represents an approximately 4% cap rate in the first year and a 5.75% cap rate when adjusting to today’s market rents.”

In all of these examples there is a recurring theme I am wanting to drive home. In every case it is a very well capitalized buyer who is under no obligation to transact.

Forced sales happen frequently and can result in adverse pricing.

Forced buys don’t really happen.

In each case, it is a sophisticated buyer coming in and after extensive underwriting they determine the properties will generate ample return even at these all-time high prices.

There is nobody on the planet that knows more about industrial real estate than Prologis, so if they are willing to buy today at a 4 cap, it makes me feel great about owning STAG Industrial (STAG) at a 6.5% FFO yield and owning Plymouth Industrial (PLYM) at an 8.1% FFO yield.

The gap between REIT pricing and real estate pricing

As of 6/28/23, the median REIT trades at 77% of net asset value (NAV). Some are trading at half of NAV. The market justifies this discount by saying property prices have come down since the most recent NAV estimates, but that just isn’t the case. Every week I see new transactions coming in at all-time high prices. I would estimate the new average is closer to 75% of today’s NAV.

With the rise in interest rates, cap rates are rising. The market has misinterpreted this to mean that NAV’s are falling.

Recall that NAV is net operating income divided by cap rate. So yes, the denominator is higher now, but so is the numerator. Rental rates are up across 18 of the 20 real estate sectors (office and malls are flattish in rent with occupancy down making NOI down). The rest are up in NOI.

The higher NOI balances out the higher cap rates and in the stronger sectors more than balances out the cap rate delta.

So what has happened is REITs have sold off while real estate continues to appreciate in value. The result is an enormous gap between stock prices and the value of the underlying assets.

How to take advantage of the dissonance between REIT pricing and real estate pricing

Leveraged buyouts (LBOs) will resurface in popularity. Private equity or other well capitalized entities are likely to start coming in, buying the discounted REITs and selling their properties to net the delta between NAV and market price.

As individual investors, the LBO business model is not feasible to execute. There are, however, some other ways to do it.

1) Buying REITs that LBO themselves.

Farmland Partners is actively selling assets and using the proceeds to buy back its stock. Last I calculated, it has bought back close to 1/3 of outstanding shares by selling assets at a premium to NAV and buying shares back at discounts to NAV ranging from 55% to 25%.

SL Green is another company LBOing itself. I still view office as too risky to want to do it personally, but for those who feel they can understand the trajectory and have the stomach for risk it could be quite opportunistic.

2) Buying REITs that are positioned to be subject to M&A

Top of our list for REITs positioned to get bought out are Plymouth Industrial, Global Medical REIT (GMRE), Broadstone Net Lease (BNL) and one of the cheap grocery anchored shopping center REITs, Brixmor (BRX), or Kite Realty (KRG).

3) Patience

Eventually, market prices move to intrinsic value. The patient investor can buy high quality discounted assets and wait until prices reflect asset values. Whether it takes months or years is unknown, but I am happy to collect dividends while I wait.

TORONTO – The Toronto Regional Real Estate Board says home sales in October surged as buyers continued moving off the sidelines amid lower interest rates.

The board said 6,658 homes changed hands last month in the Greater Toronto Area, up 44.4 per cent compared with 4,611 in the same month last year. Sales were up 14 per cent from September on a seasonally adjusted basis.

The average selling price was up 1.1 per cent compared with a year earlier at $1,135,215. The composite benchmark price, meant to represent the typical home, was down 3.3 per cent year-over-year.

“While we are still early in the Bank of Canada’s rate cutting cycle, it definitely does appear that an increasing number of buyers moved off the sidelines and back into the marketplace in October,” said TRREB president Jennifer Pearce in a news release.

“The positive affordability picture brought about by lower borrowing costs and relatively flat home prices prompted this improvement in market activity.”

The Bank of Canada has slashed its key interest rate four times since June, including a half-percentage point cut on Oct. 23. The rate now stands at 3.75 per cent, down from the high of five per cent that deterred many would-be buyers from the housing market.

New listings last month totalled 15,328, up 4.3 per cent from a year earlier.

In the City of Toronto, there were 2,509 sales last month, a 37.6 per cent jump from October 2023. Throughout the rest of the GTA, home sales rose 48.9 per cent to 4,149.

The sales uptick is encouraging, said Cameron Forbes, general manager and broker for Re/Max Realtron Realty Inc., who added the figures for October were stronger than he anticipated.

“I thought they’d be up for sure, but not necessarily that much,” said Forbes.

“Obviously, the 50 basis points was certainly a great move in the right direction. I just thought it would take more to get things going.”

He said it shows confidence in the market is returning faster than expected, especially among existing homeowners looking for a new property.

“The average consumer who’s employed and may have been able to get some increases in their wages over the last little bit to make up some ground with inflation, I think they’re confident, so they’re looking in the market.

“The conditions are nice because you’ve got a little more time, you’ve got more choice, you’ve got fewer other buyers to compete against.”

All property types saw more sales in October compared with a year ago throughout the GTA.

Townhouses led the surge with 56.8 per cent more sales, followed by detached homes at 46.6 per cent and semi-detached homes at 44 per cent. There were 33.4 per cent more condos that changed hands year-over-year.

“Market conditions did tighten in October, but there is still a lot of inventory and therefore choice for homebuyers,” said TRREB chief market analyst Jason Mercer.

“This choice will keep home price growth moderate over the next few months. However, as inventory is absorbed and home construction continues to lag population growth, selling price growth will accelerate, likely as we move through the spring of 2025.”

This report by The Canadian Press was first published Nov. 6, 2024.

HALIFAX – A village of tiny homes is set to open next month in a Halifax suburb, the latest project by the provincial government to address homelessness.

Located in Lower Sackville, N.S., the tiny home community will house up to 34 people when the first 26 units open Nov. 4.

Another 35 people are scheduled to move in when construction on another 29 units should be complete in December, under a partnership between the province, the Halifax Regional Municipality, United Way Halifax, The Shaw Group and Dexter Construction.

The province invested $9.4 million to build the village and will contribute $935,000 annually for operating costs.

Residents have been chosen from a list of people experiencing homelessness maintained by the Affordable Housing Association of Nova Scotia.

They will pay rent that is tied to their income for a unit that is fully furnished with a private bathroom, shower and a kitchen equipped with a cooktop, small fridge and microwave.

The Atlantic Community Shelters Society will also provide support to residents, ranging from counselling and mental health supports to employment and educational services.

This report by The Canadian Press was first published Oct. 24, 2024.

Housing affordability is a key issue in the provincial election campaign in British Columbia, particularly in major centres.

Here are some statistics about housing in B.C. from the Canada Mortgage and Housing Corporation’s 2024 Rental Market Report, issued in January, and the B.C. Real Estate Association’s August 2024 report.

Average residential home price in B.C.: $938,500

Average price in greater Vancouver (2024 year to date): $1,304,438

Average price in greater Victoria (2024 year to date): $979,103

Average price in the Okanagan (2024 year to date): $748,015

Average two-bedroom purpose-built rental in Vancouver: $2,181

Average two-bedroom purpose-built rental in Victoria: $1,839

Average two-bedroom purpose-built rental in Canada: $1,359

Rental vacancy rate in Vancouver: 0.9 per cent

How much more do new renters in Vancouver pay compared with renters who have occupied their home for at least a year: 27 per cent

This report by The Canadian Press was first published Oct. 17, 2024.