Canada is one of the largest agricultural producers and exporters in the world. According to Statistics Canada, the country is the fifth-largest agricultural exporter.

Simple economics suggest that if demand increases while holding supply constant, prices will rise. That means increased demand for food and constraints on arable land will lead to appreciating farmland values.

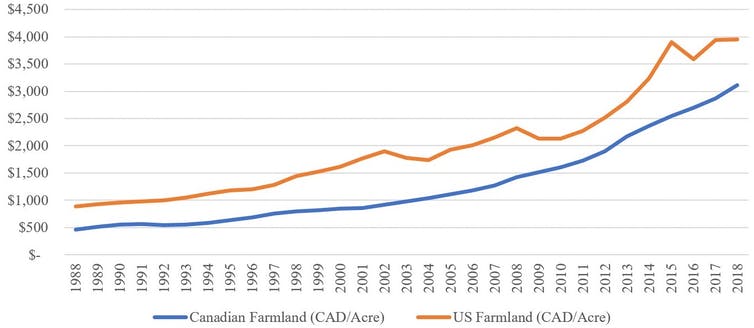

Over a 30-year period of significant population growth, the value of farmland in both Canada and the United States grew steadily. See below:

Canadian and U.S. farmland appreciation (Canadian dollars), 1988 to 2018. (Created by Grant Alexander Wilson based on data from Statistics Canada and U.S. Department of Agriculture)

According to Statistics Canada, the average price of farmland per acre in 1988 was $464. At the same time, according to the U.S. Department of Agriculture, American farmland was the equivalent of C$885 per acre. In 2018, the average of farmland per acre in Canada exceeded $3,000, and in the U.S., it exceeded $4,000. Based on this historical data and the future outlook, investment in farmland is promising.

A looming Saskatchewan boom

My experience as a senior manager of an agriculture company for the better part of a decade gave me perspective of the unique value of Saskatchewan agriculture. Farmland appreciation in the Canadian Prairies, where agriculture is a core economic driver, has shown greater increases than other areas of the country.

Saskatchewan farmland ownership has been more restricted than other provinces, resulting in a historically lower price per acre. Given the high soil quality and relaxation of purchase provisions over the past decade, the price per acre in Saskatchewan is on the rise. That means forthcoming investments are likely to provide fruitful returns and capital appreciation.

A farm tractor is silhouetted against a setting sun near Mossbank, Sask. THE CANADIAN PRESS/Adrian Wyld

Based on Farm Credit Canada’s 2018and 2019 reports, the three-year average increase in Saskatchewan farmland values was 6.2 per cent compared to 4.9 per cent in British Columbia, 3.3 per cent in Alberta and 4.2 per cent in Manitoba.

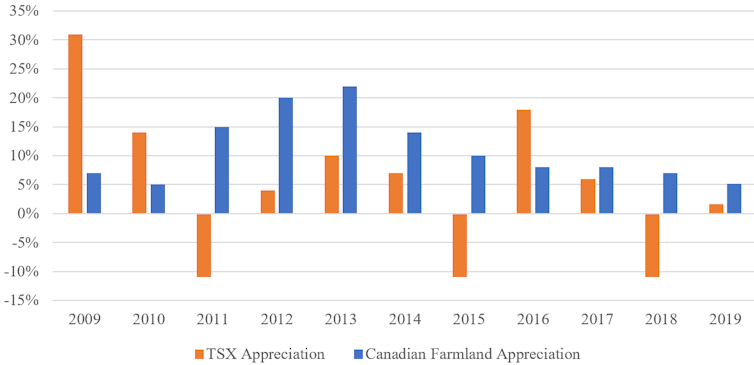

Comparing farmland to the appreciation of Canada’s primary stock exchange, the Toronto Stock Exchange (TSX), over an 11-year period from 2009 to 2019 shows the consistency and stability of farmland over stocks.

Even though the TSX showed more than 30 per cent appreciation in 2009, three of the those years produced depreciations exceeding 10 per cent. Conversely, farmland consistently appreciated, ranging from five per cent to more than 20 per cent, throughout the same 11-year period.

TSX vs. Canadian farmland appreciation 2009-19. (Created by Grant Alexander Wilson based on Farm Credit Canada and Yahoo Finance)

Given the expected global population growth, food demand and current arable land constraints, farmland investments will likely continue to yield lucrative returns.

Farmland in Canada and the U.S. has historically appreciated as population and global food demand has increased. Farmland has also served as a value-add to portfolios and has proven to be more predictable with respect to its appreciation than equity markets.

There are few storms on the horizon for Canadian farmland in terms of future investment yields. (Joshua Reddekopp/Unsplash)

Further opportunity for investment in farmland remains, with substantial value to be extracted. Specifically, regions of Canada like Saskatchewan have been historically undervalued and as a result, are appreciating.

As such, there is a compelling opportunity for profit. Due to long-term projections, now more than ever it is strategic to incorporate farmland into investment equations. To quote Mark Twain:

TORONTO – Canada’s main stock index was up more than 100 points in late-morning trading, helped by strength in base metal and utility stocks, while U.S. stock markets were mixed.

The S&P/TSX composite index was up 103.40 points at 24,542.48.

In New York, the Dow Jones industrial average was up 192.31 points at 42,932.73. The S&P 500 index was up 7.14 points at 5,822.40, while the Nasdaq composite was down 9.03 points at 18,306.56.

The Canadian dollar traded for 72.61 cents US compared with 72.44 cents US on Tuesday.

The November crude oil contract was down 71 cents at US$69.87 per barrel and the November natural gas contract was down eight cents at US$2.42 per mmBTU.

The December gold contract was up US$7.20 at US$2,686.10 an ounce and the December copper contract was up a penny at US$4.35 a pound.

This report by The Canadian Press was first published Oct. 16, 2024.

TORONTO – Canada’s main stock index was up more than 200 points in late-morning trading, while U.S. stock markets were also headed higher.

The S&P/TSX composite index was up 205.86 points at 24,508.12.

In New York, the Dow Jones industrial average was up 336.62 points at 42,790.74. The S&P 500 index was up 34.19 points at 5,814.24, while the Nasdaq composite was up 60.27 points at 18.342.32.

The Canadian dollar traded for 72.61 cents US compared with 72.71 cents US on Thursday.

The November crude oil contract was down 15 cents at US$75.70 per barrel and the November natural gas contract was down two cents at US$2.65 per mmBTU.

The December gold contract was down US$29.60 at US$2,668.90 an ounce and the December copper contract was up four cents at US$4.47 a pound.

This report by The Canadian Press was first published Oct. 11, 2024.

TORONTO – Canada’s main stock index was little changed in late-morning trading as the financial sector fell, but energy and base metal stocks moved higher.

The S&P/TSX composite index was up 0.05 of a point at 24,224.95.

In New York, the Dow Jones industrial average was down 94.31 points at 42,417.69. The S&P 500 index was down 10.91 points at 5,781.13, while the Nasdaq composite was down 29.59 points at 18,262.03.

The Canadian dollar traded for 72.71 cents US compared with 73.05 cents US on Wednesday.

The November crude oil contract was up US$1.69 at US$74.93 per barrel and the November natural gas contract was up a penny at US$2.67 per mmBTU.

The December gold contract was up US$14.70 at US$2,640.70 an ounce and the December copper contract was up two cents at US$4.42 a pound.

This report by The Canadian Press was first published Oct. 10, 2024.