Vancouver real estate agent David Hutchinson pulls out some bright blue medical gloves and tugs them onto his hands before entering a condo that’s coming onto the market.

“It’s uncharted territory, a completely different ballgame, and we’re learning everything on the go,” he said as he got his cellphone ready to do a virtual showing from the empty unit.

Welcome to selling real estate during a pandemic.

While Hutchison continues to work, albeit with adjustments, Canada’s real estate industry appears to be heading into a deep freeze despite the warming spring weather. Though sales figures started off relatively strong in March in many parts of the country, they fell swiftly as the COVID-19 pandemic grew and stricter protective measures were put in place.

Greater Vancouver’s real estate board, for example, released figures showing sales for the month overall were up 46 per cent compared to last March.

But by the end of the month, weekly statistics showed a dramatic slowdown, falling by about half compared to the first part of the month.

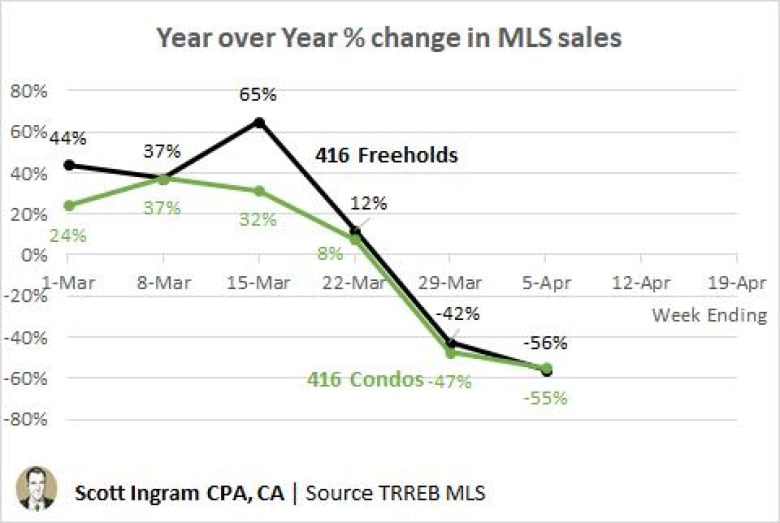

It was the same in Toronto, where home sales were up 49 per cent in the first 14 days of March compared to last year, but they plummeted by 16 per cent as the month closed.

This graphic shows how real estate sales tumbled in Toronto’s 416 area code as the epidemic took hold. (Scott Ingram)

Hutchison thinks April “is just going to fall off a cliff.”

Toronto chartered accountant and real estate agent Scott Ingram agrees. He expects April sales to be “far below historical averages.”

“Not in my time watching the Toronto real estate market have I seen sales slow right down as quickly as this,” he wrote in an email exchange. “Not even back in April 2017, when the Ontario government brought in its Ontario Fair Housing Plan with the 15 per cent non-resident speculation tax,” among other measures.

Lower prices predicted

Hutchison is worried values will fall along with the number of transactions.

“We don’t know where prices are going to go. I mean, why would you buy something now if you perceive prices are going to go down in the future, which may very well be.”

An April 3 report by RBC predicts housing sales could fall to a 20-year low, dropping 30 per cent over the coming year, and prices will indeed go down, in the short term at least.

With millions of people suddenly turning to financial aid from the government, personal finances that looked healthy a few months ago are suddenly shrouded in doubt.

WATCH | Answering viewer questions about the Canada Emergency Response Benefit

CBC News Network’s Carole MacNeil spoke with personal finance expert Lesley-Anne Scorgie to answer viewer questions about the Canada Emergency Response Benefit (CERB). 13:14

“In a matter of weeks or months, surging unemployment and the market’s illiquidity will compel a growing number of tight-squeezed sellers to make price concessions,” wrote RBC’s Robert Hogue.

Legal headaches for buyers and landlords

Across Canada about 65,000 homes traded hands in the first two months of the year, and many of those sales are now closing in a completely different environment than when the deals were made.

Vancouver real estate lawyer Ken Pazder is already seeing the fallout.

He says some clients are wondering if they have to close on deals made before the pandemic.

He has to tell them that, under the law, a deal is still a deal.

“You’re not going to be able to say ‘I don’t want to close because I’ve just lost my job, I don’t want to close because my company is shutting down or I have to shut down my business.’ That’s not going to be a legal excuse that would fly in the courts.”

In addition, his landlord clients are facing other legal issues, including tenants who suddenly aren’t paying rent.

Further complicating the situation is so-called vacant possession — a legal obligation to ensure that a sold property is in a state fit to be occupied, which can include requiring tenants to vacate when the new owner takes possession.

A moratorium on evictions in B.C. means those provisions can’t be enforced in all situations, leaving some new owners unable to access homes they have purchased.

Alberta hit by double whammy

Alberta markets could be facing the strongest head winds.

On top of the pandemic, the province has been slammed by additional layoffs caused by dramatically lower oil prices.

Calgary real estate agent Alicia Ryan says there are always some people in circumstances that force them to buy or sell, but others should consider waiting.

“Not everybody needs to sell right now, and if you don’t need to sell, we’re telling our clients hold off until things settle down a bit.”

Calgary real estate agent Alicia Ryan says the city is being hit by crashing oil prices as well as the pandemic. (Submitted by Alicia Ryan)

RBC’s Hogue says Calgary is in a tough spot. “We believe property values are at risk of a more sizable decline.

The bright spot in all of this appears to be a long way off, with Hogue predicting an eventual rebound that will come in “stages,” fuelled by low interest rates and pent-up demand from buyers currently on the sidelines.

“The timing and speed of the recovery is uncertain at this point.”

In the meantime, agents are still showing properties, but any potential buyers who want to look will likely have to sign a waiver acknowledging they may be exposing themselves to COVID-19 and accept risks that include illness and death.

TORONTO – One expert predicts Ottawa‘s changes to mortgage rules will help spur demand among potential homebuyers but says policies aimed at driving new supply are needed to address the “core issues” facing the market.

The federal government’s changes, set to come into force mid-December, include a higher price cap for insured mortgages to allow more people to qualify for a mortgage with less than a 20 per cent down payment.

The government will also expand its 30-year mortgage amortization to include first-time homebuyers buying any type of home, as well as anybody buying a newly built home.

CIBC Capital Markets deputy chief economist Benjamin Tal calls it a “significant” move likely to accelerate the recovery of the housing market, a process already underway as interest rates have begun to fall.

However, he says in a note that policymakers should aim to “prevent that from becoming too much of a good thing” through policies geared toward the supply side.

Tal says the main issue is the lack of supply available to respond to Canada’s rapidly increasing population, particularly in major cities.

This report by The Canadian Press was first published Sept. 17,2024.

OTTAWA – The Canadian Real Estate Association says the number of homes sold in August fell compared with a year ago as the market remained largely stuck in a holding pattern despite borrowing costs beginning to come down.

The association says the number of homes sold in August fell 2.1 per cent compared with the same month last year.

On a seasonally adjusted month-over-month basis, national home sales edged up 1.3 per cent from July.

CREA senior economist Shaun Cathcart says that with forecasts of lower interest rates throughout the rest of this year and into 2025, “it makes sense that prospective buyers might continue to hold off for improved affordability, especially since prices are still well behaved in most of the country.”

The national average sale price for August amounted to $649,100, a 0.1 per cent increase compared with a year earlier.

The number of newly listed properties was up 1.1 per cent month-over-month.

This report by The Canadian Press was first published Sept. 16, 2024.

MONTREAL – Two Quebec real estate brokers are facing fines and years-long suspensions for submitting bogus offers on homes to drive up prices during the COVID-19 pandemic.

Christine Girouard has been suspended for 14 years and her business partner, Jonathan Dauphinais-Fortin, has been suspended for nine years after Quebec’s authority of real estate brokerage found they used fake bids to get buyers to raise their offers.

Girouard is a well-known broker who previously starred on a Quebec reality show that follows top real estate agents in the province.

She is facing a fine of $50,000, while Dauphinais-Fortin has been fined $10,000.

The two brokers were suspended in May 2023 after La Presse published an article about their practices.

One buyer ended up paying $40,000 more than his initial offer in 2022 after Girouard and Dauphinais-Fortin concocted a second bid on the house he wanted to buy.

This report by The Canadian Press was first published Sept. 11, 2024.