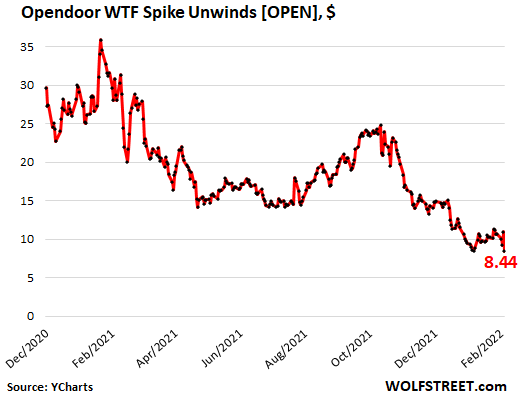

Even on Glorious Friday, the second day of a big rally after five days of sharp declines, the shares of a real-estate “tech” stock, house-flipper Opendoor, collapsed 23%, after having already collapsed in the months before.

Opendoor Technologies [OPEN], on Thursday evening, had reported a loss of $191 million for Q4, which brought its net loss for the year 2021 to $662 million, which brought its total losses for the four years that have been publicly disclosed to $1.5 billion. How can a house flipper lose $1.5 billion in four years? I don’t know either. But it isn’t over yet. And the company ended the year with an inventory of 17,009 unsold houses.

Opendoor went public in December 2020, at the IPO price of $31.47 amid enormous hoopla. By February 2021, shares had reached $39. If “February 2021” sounds familiar, it’s because that’s the month the stock market started coming unglued beneath the surface as highfliers started collapsing one at a time, each on its own schedule. The damage was such that I started reporting on it in May 2021. And this is just another chapter as it just keeps getting worse. On Friday, she shares closed at $8.44, down 78% from the February 2021 peak and 73% below its IPO price (data via YCharts):

Opendoor reported that it purchased 36,908 houses in 2021 but sold only 21,725 houses (for $8 billion) during the year, leaving it with 17,009 unsold homes ($6.1 billion) in inventory.

Opendoor financed this inventory with $6.1 billion in “non-recourse” debt backed by its houses. Non-recourse means if Opendoor defaults, its lenders get the house and cannot go after Opendoor’s other assets. If Opendoor cannot sell those homes and pay off the debt with the proceeds, it can hand the properties to the lenders and let them worry about selling the homes.

In addition, Opendoor was under contract to purchase 5,411 more homes for $1.9 billion.

About two-thirds of these 17,009 homes are finished and ready for resale. About one-third (about 5,500 homes) are “work-in-process” and are not for sale. Any of these 17,000 homes that haven’t been listed for sale, including all of the 5,500 homes that are work-in-process, are in the unknown pile of vacant homes that don’t show up in the official “supply” of homes and that don’t show up as vacant homes either.

Zillow did the same thing with a big portion of its 7,000 homes that were stuck in the pipeline before it quit the business last November and sold those homes mostly to institutional investors, who’re now trying to figure out what to do with them. These homes that are stuck in the house-flipper pipeline and that are shuffled around are vacant, but don’t show up as vacant, and they are not for sale, and don’t show up as “supply.”

House-flipping is easy – the first part, buying the house, when money is no objective, and your algo can spend as much as it wants. The rest is hard, and making money at it is even harder, especially if you overpaid in the first place. The activity is not suited for people who write algos, it turns out.

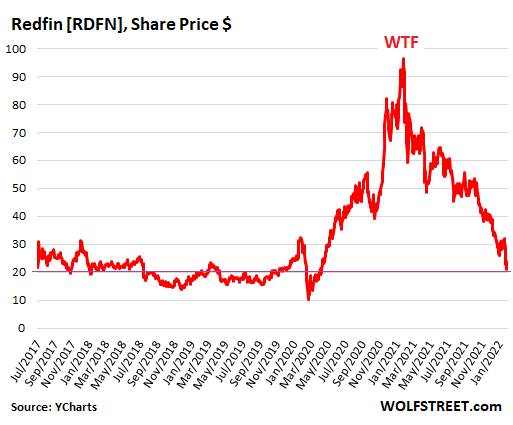

Redfin, originally an online real estate broker, also rode up the algo-based house-flipper craze starting in 2020. And its shares [RDFN] rocketed higher amid endless hoopla by the crazed crowd of stock jockeys and hit a high of $98.44 in February 2021 – yup, that February again.

Then shares began their long collapse. On Friday, they closed at $21.83, having collapsed by 78% in one year. They’re now below where they’d been after the first day of trading following its IPO in July 2017:

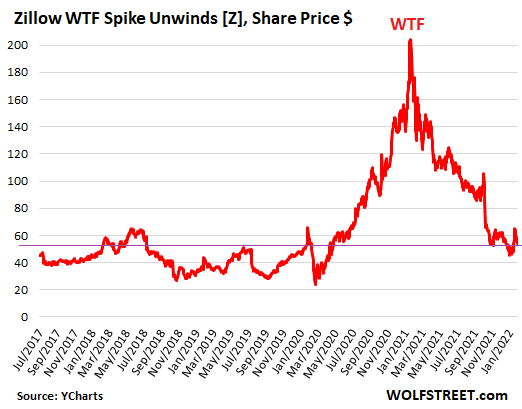

Zillow [ZG] had a brief respite in its collapse when it announced on February 10 that it lost $881 million in 2021 on its home-flipping escapade, which came unglued in November 2021, when it disclosed that it would lay off 25% of its staff and get out of the house-flipping business, and dump the 7,000 homes it had bought.

Later it disclosed that it had sold most of these houses to institutional investors – rather than to people who might have wanted to live in them. Until those vacant houses are listed for sale they don’t show up in the official “supply,” and many of them may eventually show up on the rental market. And while all this is going on as they’re being shuffled around, they don’t show up as vacant either.

The $881 million loss was less than feared, and shares bounced magically over the following three trading days, but have since then given up a portion of it. On Friday, shares closed at $57.95, down 73% from their high a year ago, and about level with where they’d been in February 2020 before the crash:

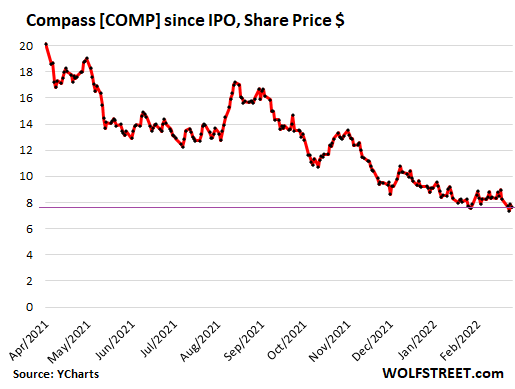

Compass, a real-estate broker that calls itself “a tech company reinventing the space,” is one of those examples – one of very many – when you realize something is seriously wrong with Wall Street. But OK, people have fun with their trading apps, and if they get cleaned out, so be it.

Compass grew by using Softbank’s money, and the money of other investors, to buy up real estate brokerages around the country. Over the five years of publicly disclosed financial statements, Compass has lost $1.44 billion. How can a real estate broker in the red-hottest no-questions-asked housing market lose $1.44 billion? That was a rhetorical question.

Compass shares [COMP] peaked on their first day of trading, following the IPO in April last year, at $22.11 and have declined ever since. On Friday, they closed at $7.65, having plunged 65% in 10 months since the high on the first day of trading, and are now 58% below the IPO price of $18 a share:

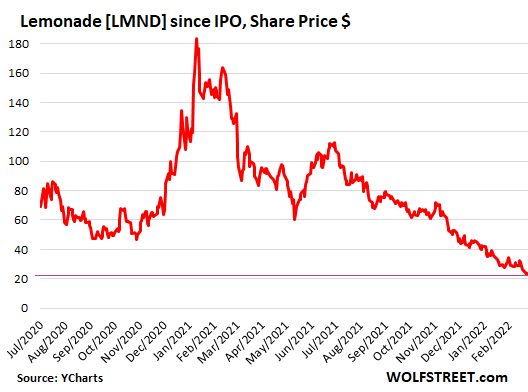

Lemonade [LMND], which is hyped as an “insurance tech company” and sells insurance for renters, homeowners, pet owners, etc., went public in July 2020 at $29 a share and in the first day of trading, amid immense hoopla, spiked 139%. It then continued spiking until it reached $182 in January 2021. And then came said February 2021, when this whole show started unraveling.

On Friday, shares closed at $23.48, down 83% from the high, and 19% below the IPO price at which the shares never even traded because the first trade was at $50 a share, causing the tech stock pundits to lament how the company “mispriced” the IPO and how much money it “left on the table.” Yup, that’s how crazy this show was at the time.

Waiting for a share-price collapse is Better.com, a “tech” mortgage lender, backed by Softbank. It’s not yet a publicly traded stock because its merger with a SPAC was postponed in December 2021 after the CEO fired 900 employees, most of them in India, via a Zoom meeting that went viral, that idiot.

With the SPAC merger, and therefore the inflow of cash, having been delayed, the company raised $750 million from Softbank and its SPAC backers because, you know, these kinds of companies constantly burn large amounts of cash and constantly need new cash to burn.

So I’m looking forward to the moment the stock finally starts trading so I can add it to this list of collapsing real-estate “tech” stocks. This should be a goodie. So let’s hope that the merger with the SPAC goes through.

Enjoy reading WOLF STREET and want to support it? Using ad blockers – I totally get why – but want to support the site? You can donate. I appreciate it immensely. Click on the beer and iced-tea mug to find out how:

Would you like to be notified via email when WOLF STREET publishes a new article? Sign up here.

TORONTO – The Toronto Regional Real Estate Board says home sales in October surged as buyers continued moving off the sidelines amid lower interest rates.

The board said 6,658 homes changed hands last month in the Greater Toronto Area, up 44.4 per cent compared with 4,611 in the same month last year. Sales were up 14 per cent from September on a seasonally adjusted basis.

The average selling price was up 1.1 per cent compared with a year earlier at $1,135,215. The composite benchmark price, meant to represent the typical home, was down 3.3 per cent year-over-year.

“While we are still early in the Bank of Canada’s rate cutting cycle, it definitely does appear that an increasing number of buyers moved off the sidelines and back into the marketplace in October,” said TRREB president Jennifer Pearce in a news release.

“The positive affordability picture brought about by lower borrowing costs and relatively flat home prices prompted this improvement in market activity.”

The Bank of Canada has slashed its key interest rate four times since June, including a half-percentage point cut on Oct. 23. The rate now stands at 3.75 per cent, down from the high of five per cent that deterred many would-be buyers from the housing market.

New listings last month totalled 15,328, up 4.3 per cent from a year earlier.

In the City of Toronto, there were 2,509 sales last month, a 37.6 per cent jump from October 2023. Throughout the rest of the GTA, home sales rose 48.9 per cent to 4,149.

The sales uptick is encouraging, said Cameron Forbes, general manager and broker for Re/Max Realtron Realty Inc., who added the figures for October were stronger than he anticipated.

“I thought they’d be up for sure, but not necessarily that much,” said Forbes.

“Obviously, the 50 basis points was certainly a great move in the right direction. I just thought it would take more to get things going.”

He said it shows confidence in the market is returning faster than expected, especially among existing homeowners looking for a new property.

“The average consumer who’s employed and may have been able to get some increases in their wages over the last little bit to make up some ground with inflation, I think they’re confident, so they’re looking in the market.

“The conditions are nice because you’ve got a little more time, you’ve got more choice, you’ve got fewer other buyers to compete against.”

All property types saw more sales in October compared with a year ago throughout the GTA.

Townhouses led the surge with 56.8 per cent more sales, followed by detached homes at 46.6 per cent and semi-detached homes at 44 per cent. There were 33.4 per cent more condos that changed hands year-over-year.

“Market conditions did tighten in October, but there is still a lot of inventory and therefore choice for homebuyers,” said TRREB chief market analyst Jason Mercer.

“This choice will keep home price growth moderate over the next few months. However, as inventory is absorbed and home construction continues to lag population growth, selling price growth will accelerate, likely as we move through the spring of 2025.”

This report by The Canadian Press was first published Nov. 6, 2024.

HALIFAX – A village of tiny homes is set to open next month in a Halifax suburb, the latest project by the provincial government to address homelessness.

Located in Lower Sackville, N.S., the tiny home community will house up to 34 people when the first 26 units open Nov. 4.

Another 35 people are scheduled to move in when construction on another 29 units should be complete in December, under a partnership between the province, the Halifax Regional Municipality, United Way Halifax, The Shaw Group and Dexter Construction.

The province invested $9.4 million to build the village and will contribute $935,000 annually for operating costs.

Residents have been chosen from a list of people experiencing homelessness maintained by the Affordable Housing Association of Nova Scotia.

They will pay rent that is tied to their income for a unit that is fully furnished with a private bathroom, shower and a kitchen equipped with a cooktop, small fridge and microwave.

The Atlantic Community Shelters Society will also provide support to residents, ranging from counselling and mental health supports to employment and educational services.

This report by The Canadian Press was first published Oct. 24, 2024.

Housing affordability is a key issue in the provincial election campaign in British Columbia, particularly in major centres.

Here are some statistics about housing in B.C. from the Canada Mortgage and Housing Corporation’s 2024 Rental Market Report, issued in January, and the B.C. Real Estate Association’s August 2024 report.

Average residential home price in B.C.: $938,500

Average price in greater Vancouver (2024 year to date): $1,304,438

Average price in greater Victoria (2024 year to date): $979,103

Average price in the Okanagan (2024 year to date): $748,015

Average two-bedroom purpose-built rental in Vancouver: $2,181

Average two-bedroom purpose-built rental in Victoria: $1,839

Average two-bedroom purpose-built rental in Canada: $1,359

Rental vacancy rate in Vancouver: 0.9 per cent

How much more do new renters in Vancouver pay compared with renters who have occupied their home for at least a year: 27 per cent

This report by The Canadian Press was first published Oct. 17, 2024.