Economy

Confused by the economy during the COVID-19 pandemic? Don't worry, so are the economists – CBC.ca

The numbers can be so big, they’re hard to get your head around. The swings are so volatile, you can lose your footing.

And yet, with millions of Canadians struggling through the COVID-19 crisis, many of us want to understand what is going on with the economy.

“My head is spinning, too,” said Benjamin Tal, deputy chief economist at CIBC. “So I don’t blame people, because we’ve never seen anything like this.”

Every week, a flood of new data comes out. This week, we were inundated with the federal government’s fiscal update, GDP figures and job numbers. All trying to shape the story of the economy. Sometimes the numbers contradict each other. Sometimes they give a sort of head-fake and contradict themselves.

The fiscal update that came out on Monday had built all its projections on an average of the forecasts from the big banks. The next morning, Statistics Canada released quarterly GDP numbers that missed the forecast by a staggering seven points. By the end of the week, jobs data came out showing Canadian employers added three times as many jobs as expected.

Every economist is trying to figure out what those numbers are telling us. And they’re not always getting it right.

“Economists have never been more wrong about where the data would come through,” said Frances Donald, chief economist and head of macro strategy at Manulife Investment Management in Toronto.

New methods

Most of the time, she said, economists rely on data such as job growth and retail sales numbers to make sense of the situation. The problem is those statistics tell us what was happening months ago.

“This is a daily crisis that requires daily data points,” she said.

To combat that, economists have turned to higher frequency data such as google mobility trends, restaurant reservation tallies and public transit numbers.

But Donald said the bigger issue is the unique, unprecedented nature of this crisis.

“We don’t have a functional precedent for what is happening,” she said.

There may be other moments in the past that share some similarities, but nothing experts can use to model probable outcomes.

Change of perspective

Tal said he understands why more Canadians than usual seem to be following economic updates with bated breath. But he said the best option is to focus less on the details and think of the broader economic themes.

So, while the short term is bad, he said, the medium term looks better.

“We are buying time at this point,” he said, until the virus comes under control.

Yes, the world is headed into a long and dark winter, he said. Yes, COVID-19 cases are rising and government-imposed restrictions could spread. And, yes, households and businesses will need government support and record-low interest rates to provide them a bridge to the second half of next year, he said.

But if you zoom out and look at the longer-term forecasts, the second half of next year shows a lot of promise. Tal said the economic crisis is largely due to the fact that people aren’t spending as much as they normally would.

Some of that is because of government-mandated closures.

But some of it is also a question of confidence.

Even if the movie theatres were open, how many people would pay to sit in close contact with strangers for a two-hour film?

Looking ahead

That spending issue is a large source of the hope for 2021. Tal calculates that Canadian households and businesses are sitting on $170 billion in savings. And once the virus comes under control, he predicts that money will spill back into the economy.

“I see this unleashing of potential demand in the economy,” he said. “Most of it will be in the services sector. And that will benefit employment for people that are struggling. It’s just a question of time.”

So, in the interim, he recommends not getting too caught up in the minutiae of the daily economic data.

That’s advice financial markets seem to be following. As COVID-19 case counts soar and government-imposed restrictions spread, the major stock market indexes are all climbing. Donald said markets seem to be looking past the short- and medium-term unknowns and banking on a solid return next year.

WATCH | The National’s report on the fall economic update:

The government unveiled a record deficit of $381 billion in its fiscal update, along with spending plans for more pandemic relief and a huge stimulus plan to jolt the economy post-pandemic. 2:18

She said the markets don’t seem to be too caught up in the daily barrage of economic information.

“The markets are thinking ahead to where we are going to be in 6, 12, 48 months,” she said. “Not where we are at this very moment.”

Besides, she said, one of the best indicators available is to just look around and see how people around you are acting. Are people nervous and scared? Are they staying home or are they out shopping? The data will catch up to our behaviour eventually.

“You don’t need a PhD in economics to look around at your friends and family and get a sense of what their behaviour is,” she said. “We don’t need numbers and releases, we just need to look out our front doors.”

Economy

Opinion: Higher capital gains taxes won't work as claimed, but will harm the economy – The Globe and Mail

Canada’s Prime Minister Justin Trudeau and Finance Minister Chrystia Freeland hold the 2024-25 budget, on Parliament Hill in Ottawa, on April 16.Patrick Doyle/Reuters

Alex Whalen and Jake Fuss are analysts at the Fraser Institute.

Amid a federal budget riddled with red ink and tax hikes, the Trudeau government has increased capital gains taxes. The move will be disastrous for Canada’s growth prospects and its already-lagging investment climate, and to make matters worse, research suggests it won’t work as planned.

Currently, individuals and businesses who sell a capital asset in Canada incur capital gains taxes at a 50-per-cent inclusion rate, which means that 50 per cent of the gain in the asset’s value is subject to taxation at the individual or business’s marginal tax rate. The Trudeau government is raising this inclusion rate to 66.6 per cent for all businesses, trusts and individuals with capital gains over $250,000.

The problems with hiking capital gains taxes are numerous.

First, capital gains are taxed on a “realization” basis, which means the investor does not incur capital gains taxes until the asset is sold. According to empirical evidence, this creates a “lock-in” effect where investors have an incentive to keep their capital invested in a particular asset when they might otherwise sell.

For example, investors may delay selling capital assets because they anticipate a change in government and a reversal back to the previous inclusion rate. This means the Trudeau government is likely overestimating the potential revenue gains from its capital gains tax hike, given that individual investors will adjust the timing of their asset sales in response to the tax hike.

Second, the lock-in effect creates a drag on economic growth as it incentivizes investors to hold off selling their assets when they otherwise might, preventing capital from being deployed to its most productive use and therefore reducing growth.

Budget’s capital gains tax changes divide the small business community

And Canada’s growth prospects and investment climate have both been in decline. Canada currently faces the lowest growth prospects among all OECD countries in terms of GDP per person. Further, between 2014 and 2021, business investment (adjusted for inflation) in Canada declined by $43.7-billion. Hiking taxes on capital will make both pressing issues worse.

Contrary to the government’s framing – that this move only affects the wealthy – lagging business investment and slow growth affect all Canadians through lower incomes and living standards. Capital taxes are among the most economically damaging forms of taxation precisely because they reduce the incentive to innovate and invest. And while taxes on capital gains do raise revenue, the economic costs exceed the amount of tax collected.

Previous governments in Canada understood these facts. In the 2000 federal budget, then-finance minister Paul Martin said a “key factor contributing to the difficulty of raising capital by new startups is the fact that individuals who sell existing investments and reinvest in others must pay tax on any realized capital gains,” an explicit acknowledgment of the lock-in effect and costs of capital gains taxes. Further, that Liberal government reduced the capital gains inclusion rate, acknowledging the importance of a strong investment climate.

At a time when Canada badly needs to improve the incentives to invest, the Trudeau government’s 2024 budget has introduced a damaging tax hike. In delivering the budget, Finance Minister Chrystia Freeland said “Canada, a growing country, needs to make investments in our country and in Canadians right now.” Individuals and businesses across the country likely agree on the importance of investment. Hiking capital gains taxes will achieve the exact opposite effect.

Nigeria’s economy, which ranked as Africa’s largest in 2022, is set to slip to fourth place this year and Egypt, which held the top position in 2023, is projected to fall to second behind South Africa after a series of currency devaluations, International Monetary Fund forecasts show.

The IMF’s World Economic Outlook estimates Nigeria’s gross domestic product at $253 billion based on current prices this year, lagging energy-rich Algeria at $267 billion, Egypt at $348 billion and South Africa at $373 billion.

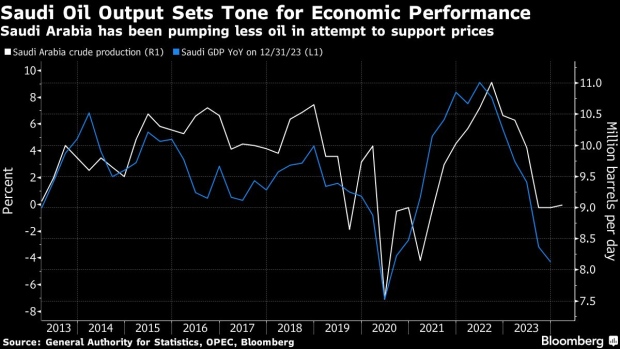

(Bloomberg) — The International Monetary Fund expects OPEC and its partners to start increasing oil output gradually from July, a transition that’s set to catapult Saudi Arabia back into the ranks of the world’s fastest-growing economies next year.

“We are assuming the full reversal of cuts is happening at the beginning of 2025,” Amine Mati, the lender’s mission chief to the kingdom, said in an interview in Washington, where the IMF and the World Bank are holding their spring meetings.

The view explains why the IMF is turning more upbeat on Saudi Arabia, whose economy contracted last year as it led the OPEC+ alliance alongside Russia in production cuts that squeezed supplies and pushed up crude prices. In 2022, record crude output propelled Saudi Arabia to the fastest expansion in the Group of 20.

Under the latest outlook unveiled this week, the IMF improved next year’s growth estimate for the world’s biggest crude exporter from 5.5% to 6% — second only to India among major economies in an upswing that would be among the kingdom’s fastest spurts over the past decade.

The fund projects Saudi oil output will reach 10 million barrels per day in early 2025, from what’s now a near three-year low of 9 million barrels. Saudi Arabia says its production capacity is around 12 million barrels a day and it’s rarely pumped as low as today’s levels in the past decade.

Mati said the IMF slightly lowered its forecast for Saudi economic growth this year to 2.6% from 2.7% based on actual figures for 2023 and the extension of production curbs to June. Bloomberg Economics predicts an expansion of 1.1% in 2024 and assumes the output cuts will stay until the end of this year.

Worsening hostilities in the Middle East provide the backdrop to a possible policy shift after oil prices topped $90 a barrel for the first time in months. The Organization of Petroleum Exporting Countries and its allies will gather on June 1 and some analysts expect the group may start to unwind the curbs.

After sacrificing sales volumes to support the oil market, Saudi Arabia may instead opt to pump more as it faces years of fiscal deficits and with crude prices still below what it needs to balance the budget.

Saudi Arabia is spending hundreds of billions of dollars to diversify an economy that still relies on oil and its close derivatives — petrochemicals and plastics — for more than 90% of its exports.

Restrictive US monetary policy won’t necessarily be a drag on Saudi Arabia, which usually moves in lockstep with the Federal Reserve to protect its currency peg to the dollar.

Mati sees a “negligible” impact from potentially slower interest-rate cuts by the Fed, given the structure of the Saudi banks’ balance sheets and the plentiful liquidity in the kingdom thanks to elevated oil prices.

The IMF also expects the “non-oil sector growth momentum to remain strong” for at least the next couple of years, Mati said, driven by the kingdom’s plans to develop industries from manufacturing to logistics.

The kingdom “has undertaken many transformative reforms and is doing a lot of the right actions in terms of the regulatory environment,” Mati said. “But I think it takes time for some of those reforms to materialize.”

©2024 Bloomberg L.P.

U of T Engineering PhD student is working to improve the sustainable treatment of Ontario's drinking water – U of T Engineering News – U of T Engineering News

Scientists Say They Have Found New Evidence Of An Unknown Planet… – 2oceansvibe News

Opinion: Higher capital gains taxes won't work as claimed, but will harm the economy – The Globe and Mail

Silver investment demand jumped 12% in 2019

12 Bizarre Things People Did Just To Make Social Media Content

Global Media Markets, 2015-2020, 2020-2025F, 2030F – TV and Radio Broadcasting, Film and Music, Information Services, Web Content, Search Portals And Social Media, Print Media, & Cable – GlobeNewswire

-

Investment23 hours ago

Investment23 hours agoUK Mulls New Curbs on Outbound Investment Over Security Risks – BNN Bloomberg

-

Sports21 hours ago

Auston Matthews denied 70th goal as depleted Leafs lose last regular-season game – Toronto Sun

-

Media2 hours ago

DJT Stock Rises. Trump Media CEO Alleges Potential Market Manipulation. – Barron's

-

Business20 hours ago

BC short-term rental rules take effect May 1 – CityNews Vancouver

-

Media4 hours ago

Trump Media alerts Nasdaq to potential market manipulation from 'naked' short selling of DJT stock – CNBC

-

Art20 hours ago

Collection of First Nations art stolen from Gordon Head home – Times Colonist

-

Investment20 hours ago

Benjamin Bergen: Why would anyone invest in Canada now? – National Post

-

Tech23 hours ago

Save $700 Off This 4K Projector at Amazon While You Still Can – CNET

{kind=link}