Do you make a clear distinction between a credit report and a credit score? It’s easy to mistake these two connected things for the same.

Key Upshots

- Your credit report is a chronicle of your indebtedness. It features your personally identifiable information including a record of your past and present obligations. It also indicates if you have always paid your debts on time or if you have ever missed a payment.

- Your credit score is a 3 number figure calculated using information from your credit report. The greater your score, the more enticing you are to lenders. A lower figure may reflect negatively on your credit situation.

- Your credit score does not ensure that you will be approved or denied for credit. Individual credit issuers often evaluate you based on their criteria, which may include your previous contact with them.

If you pay attention, you will see numerous significant differences between the two. We highlight how your credit score and credit report differ and how they interact to give a picture of your financial health. While the terms credit score and credit report are frequently used alike, they are not synonymous. Credit scores and credit reports are both dependent on how effectively you’ve managed credit in the past, but there are some key differences to be cognizant of.

What is a Credit Report, precisely?

A credit report comprises information on your observed in previous and present credit agreements, such as credit card accounts, mortgages, and student loans, as well as credit history checks. It reveals how much you owe creditors, how long every account has been open, and how often you make on-time repayments. Credit reports also include information from public records such as receivables or bad debts. Having secured credit cards Canada and making repayments on time have positive impacts on your credit history.

Parts of a Credit Report

Your credit report is divided into three sections:

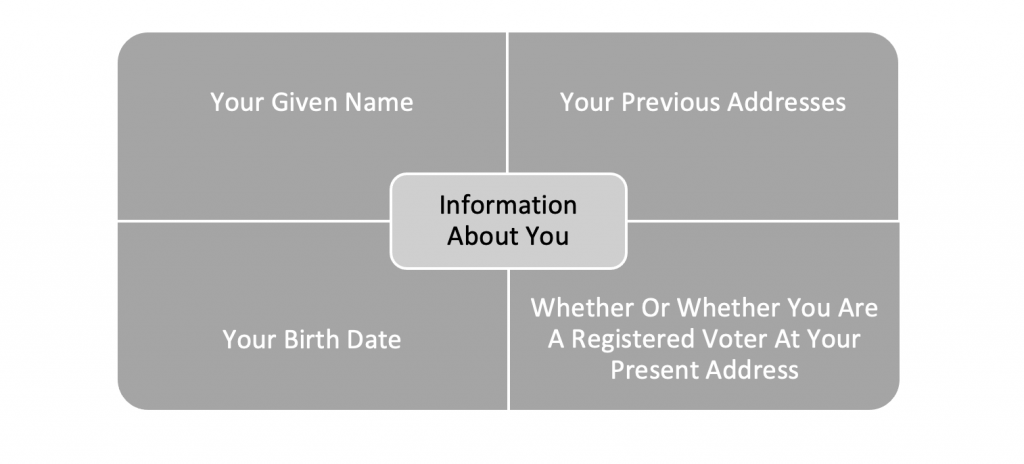

- Information about you

This section includes the following items:

Since credit bureaus use your address to match up all of your credit history, it is critical. As an outcome, it is vital that you register all of your bank accounts at a single location. Notify your lenders as soon as possible if you migrate so that they can update your information. This guarantees that your credit report is complete and correct.

2.History of credit accounts

This is a list of your credit and current accounts (for example, a credit card or a bank account). You will indeed be capable to see how much liabilities you currently have (your balance). This section will display your current accounts (which will have a £0 amount unless you have an overdraft), secured credit cards, short-term loans, and long-term debts, such as a mortgage.

It may, however, include less apparent information, such as accounts with energy providers, internet service providers (ISPs), and mobile phone networks. If you use secured credit cards Canada, then it may help you in maintaining a great credit history.

In a formal sense, these are also credit accounts. You are receiving a service today and will be charged later. It is up to the individual supplier whether they will appear on your credit record. Not all service providers provide reports to credit bureaus.

- History of Payment

Your credit report will indicate if you have paid your obligations on time each month, whether you have made late payments, or if you have skipped any payments completely. At the risk of repeating myself, paying your obligations on time is a good thing. Missed payments reflect poorly on you.

What Is The Protocol For Obtaining A Copy Of Credit Report?

| Every year, you are eligible for a free copy of each of your credit reports; you may get them through the government-approved website AnnualCreditReport.com |

Monitoring your credit reports might help youdiscover what lenders will look for when you apply for a loan.

IMPORTANT

Do you still need a clarification of what a credit report is? Well you have it now!

A credit report is a record of all your obligations including repayments and installments from secured credit cards Canada. It’s similar to a curriculum vitae or a school report. Only this time, instead of information about your prior work or academic achievement, it includes information on how you borrowed and repaid money.

The majority of the information in your report is provided by lenders. Credit reference agencies, which generate credit reports, compile this information.

What precisely is a Credit Score?

A credit score is akin to a test score issued to your credit report. This three-digit figure, which is based on the conventional FICO® Score, generally runs from 300 to 850. Equifax®, Experian®, and TransUnion® are the three credit reporting companies that issue you a credit score. It includes you credit behaviours from unsecured or secured credit cards Canada.

When you seek your credit score, you will receive three numbers in response, which may all be different because the figures come from various reporting agencies. When you obtain your free yearly credit report, your credit score will not be included.

| Your credit score is a three-digit figure that is calculated based on the financial history contained in your credit report. Monitor your credit report to ensure it is up to date and correct in order to safeguard your credit score. |

PRO TIP

Each credit bureau will charge you a fee to see your credit score. If some of your credit scores change drastically from the others after getting them from all three agencies, you should carefully check your credit report to determine if there are any inaccuracies that you may dispute. A high credit score indicates a lesser likelihood of financial distress, and clients with a high credit score are much more likely to qualify for a loan.

Still not sure what is a credit score? Here is a simple explanation.

If your credit report was a report card, your credit score would be your total grade. In all other terms, it measures the likelihood that you will be sanctioned for credit based on the information in your credit report, as well as the attractiveness of your credit conditions.

So, What Exactly Constitutes A “Fair” Credit Score?

Normally, the higher your score, the better. A decent credit score shows moneylenders that you are more responsible, and hence more ‘technically qualified.’ This is data from report of Equifax, which assigns the following scores:

| Very poor | 0 to 278 |

| Poor | 279 to 366 |

| Fair | 367 to 419 |

| Good | 420 to 466 |

| Excellent | 467 and Above |

Credit reference agencies have varying maximum scores as well. Experian has a score of 999, Equifax has a score of 700, and Callcredit has a score of 710. They also come in many different scales. Your credit score may be 459 with Equifax, 999 with Experian, and 609 with Callcredit based on the same information.

And here is a more in-depth look at credit ratings, how they’re calculated, and what factors may affect your score.

How Can I Determine My Credit Score?

You may call the credit reporting bureaus to obtain your credit score for a charge. There are many websites where you may get a free Vantage Score. A Vantage Score and a FICO® Credit Score are not quite the same thing, as they are derived uniquely. Some banks and credit card firms offer credit ratings to qualified clients. You can make responsible choices about your financial future by knowing your credit report and credit score and verifying them for accuracy on a regular basis.

What Is The Distinction Between A Credit Score And A Credit Report, And How Are They Connected?

Your credit report is a thorough record of all your financial transactions. A credit score is a number generated by credit bureaus and lenders that outlines the details in a credit report.

“According to the FTC (Federal Trade Commission), one out of every five consumers discovers a mistake on their credit report. These mistakes have an impact on your credit score and ability to apply for loans, leases, credit cards, and other services.”

Your credit report indicates how you’ve historically handled unsecured and secured credit cards Canada. When credit companies look at your report, they can answer crucial questions about your financial habits, such as:

- How much debt do you already have?

- Do you pay down the bills in a timely manner?

- Do you have a tendency of taking out loans than you can handle?

These and other considerations assist credit lenders in making decisions:

- If to give you credit what so ever

- On what conditions to give you credit (specifically, what interest rate and repayment plan they will offer you).

When you look at all of the information in your credit report, it’s difficult to predict how a lender would take it. Your score combines all of the information in your report into a single number. This allows you to assess how you’re performing in relation to what lenders are searching for.

But here’s a word to the savvy.

Your credit record isn’t the only information a creditor will consider when making a decision. The information you offer in your application, their previous interactions with you, and other criteria such as your income are all significant.

Different suppliers also have their credit ratings. So, while a high Experian, Equifax, or CallCredit score is not a guarantee of credit, it is a good sign. Similarly, just because one supplier turned you down does not guarantee that others will follow suit. If you want to have another layer of cushion, then having secured credit cards Canada can be of great help.

Key Differences between Credit Report and Credit Score

| Credit Report | Credit Score |

| A thorough text-based report containing personal information, employment information, public records, accounts under collection, payment history, and other information like outstanding balances, Age of credit accounts, New credit accounts, assortment of credit kinds. | A comprehensive score demonstrating your overall solvency based on the information in your credit report. |

| Experian, Equifax, and TransUnion credit bureau data are often used to create this report. | Can only be computed using information from a credit report. |

| Creditworthiness is determined based on the specifics of your present financial commitments and credit history, including any prior negative marks. | Creditworthiness is determined by five weighted factors: Payment history, amounts owing, duration of credit history, credit mix, and current activity are all factors to consider. |

| Can be obtained directly from credit bureaus or via AnnualCreditReport.com. | Credit reports are available through a credit agency, your banker, your credit card issuer, or a credit consultant. |

| It is used by bankers, creditors, debt collectors, insurance providers, utility providers, employers, and property owners. | It is used by bankers, creditors, debt collectors, insurance providers, utility providers, and tenants. Employers cannot inspect your credit score created by FCRA. |

Why Does This Make Any Difference?

Comprehending the functions and roles of your credit score and credit report might be crucial to your economic well-being.

Inspect your free credit report and FICO score at least once every year. Pay close attention to credit report habits that are strongly weighted against your credit score. Investigate everything that appears to be out of the ordinary. Plan ahead of time since it might make the difference between permission and denial.

Frequently Asked Questions

- Is a good credit score more essential than a good credit report?

They are distinct, yet they are related since the score is generated from the report. Creditors can use either to decide to choose whether or not extend credit to you. Your credit score is vital, but you still need your credit reports if you want to dig deeper and assess your credit history.

- Which credit report is the most reliable?

Since FICO scores are employed in more than 90% of loan decisions, the FICO® Basic, Advanced, and Premier services are the most accurate for credit score updates. All services include access to 28 different versions of your FICO score, including credit card, mortgage, and auto loan scores.

- How can I raise my credit score swiftly?

The most significant actions you can take to improve your credit are to pay your bills on time and to pay off your credit card balances. Every 30 days, issuers record your payment activity to the credit bureaus, so taking good measures might boost your score rapidly.