On January 19, 2022, the Canadian Securities Administrators (the “CSA”) published guidance, CSA Staff Notice 81-334 – ESG-Related Investment Fund Disclosure (the “Guidance”), for investment funds in dealing with ESG-related considerations, particularly around disclosure issues.

Below we briefly outline the background, as set out by the CSA, which has led to the development of this Guidance, and then discuss in more detail the specific clarifications that the CSA has put forth in its Guidance. For the sake of clarity, any views set out in this bulletin are solely those of the CSA, as presented in the Guidance, and not those of Fasken.

Before we dive into the discussion, it is worth highlighting here that the CSA has stated that the Guidance “does not create any new legal requirements or modify existing ones” [emphasis added]; rather, it “clarifies and explains how the current securities regulatory requirements apply to ESG-related investment fund disclosure”, and provides best practices for such funds.

As the CSA notes, there is growing interest in ESG investing in Canada from both retail and institutional investors. On the international front, the CSA highlights certain work being undertaken with respect to “ESG or sustainability-related disclosure for investment funds” by various international securities regulators (e.g., the European Union in its Sustainable Finance Disclosure Regulation), by IOSCO (International Organization of Securities Commissions) (including noting its recommendation for the “improvement of product-level disclosure”), and by the CFA Institute (including its publication of the “CFA Institute Global ESG Disclosure Standards for Investment Products to provide greater transparency and comparability to investors by enabling asset managers to clearly communicate the ESG-related features of their investment products”).

On the domestic front, the CSA explains the review (the “Review”) of regulatory disclosure documents and sales communications published by certain ESG-Related Funds (defined below) and other funds that market themselves as ESG-Related Funds that its staff (“CSA Staff”) undertook. “ESG-Related Funds” is comprised of both funds whose investment objectives reference ESG factors (“ESG Funds”) and funds that use ESG strategies (“ESG Strategy Funds”). As part of the Review, the CSA staff evaluated 32 funds managed by 23 different investment fund managers (“IFMs”).

From its review of both the international and domestic landscape, the CSA notes its concern regarding the “increased potential for ‘greenwashing’”, and specifically notes as a result of the findings from its Review, that although the current regulatory landscape is “broad enough” to capture disclosure aspects applicable to ESG-Related Funds, additional guidance is necessary to “improve the quality of ESG-related disclosure and sales communications”.

Taking all of the above into consideration, the CSA published the Guidance to address these various concerns. More specifically, according to the CSA, the Guidance clarifies the existing legislation with respect to the following aspects: (i) investment objectives and fund names; (ii) fund types; (iii) investment strategies disclosure; (iv) proxy voting and shareholder engagement policies and procedures; (v) risk disclosure; (vi) suitability; (vii) continuous disclosure; (viii) sales communications; (ix) ESG-related changes to existing funds; and (x) ESG-related terminology.

We walk through the key takeaways from the Guidance for each item below.

Two notes worth mentioning here are that for the sake of conciseness, we primarily focus on the clarifications provided by the Guidance, and have intentionally omitted including the existing laws or regulations where applicable (on the assumption that readers would be familiar with such concepts, such as continuous disclosure requirements). Additionally, where guidance below is described as being “encouraged”, then such guidance is not required; instead, it reflects best practices according to the CSA Staff.

I. Investment Objectives and Fund Names

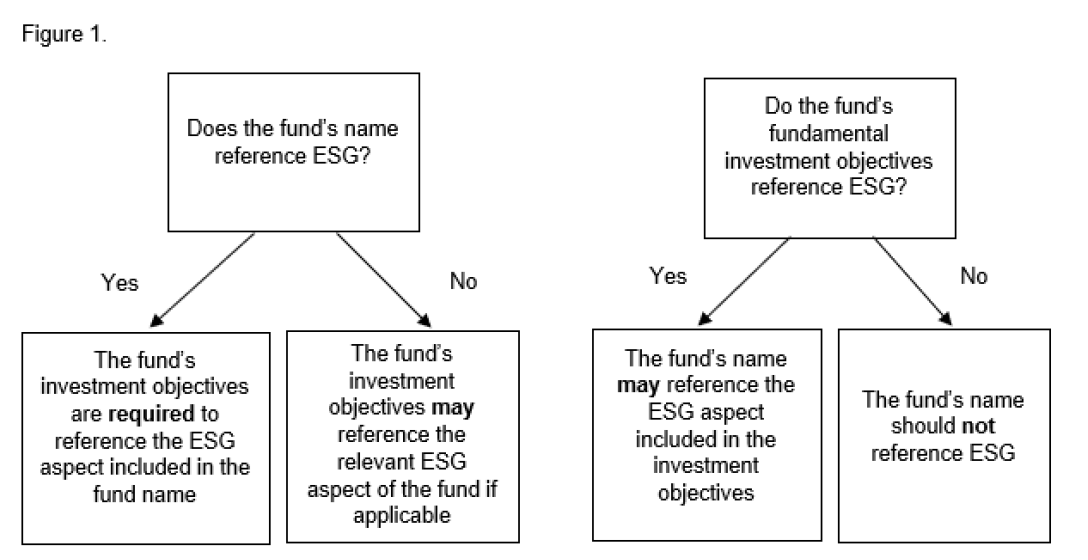

Both a fund’s name, and its objectives, should “accurately reflect the primary focus of the fund,” including the “extent to which a fund is focused on ESG, where applicable, including the particular aspect(s) of ESG that the fund is focused on.”

As illustrated in Figure 1, to the extent a fund does not reference ESG in its investment objectives, then it should not have “ESG” (or any related terms, e.g., “sustainability”, “green”) in its name. Conversely, if a fund does reference ESG in its name, then it is required to include ESG-considerations in its investment objectives.

Source: Guidance, page 10

II. Fund Types

For non-ETF mutual funds required to identify its fund type in its prospectus, a mutual fund that includes ESG in its fundamental objectives (i.e., an ESG Fund) “may wish to characterize itself as a fund that is focused on ESG…,” while a fund that does not include such objectives, according to the CSA Staff’s view, “should not characterize itself as a fund that is focused on ESG as it would not be an accurate identification of the fund type” [emphasis added].

III. Investment Strategies Disclosure

With respect to disclosure about a funds’ investment strategy, we first discuss clarifications applicable to all funds, followed by those clarifications applicable only to funds employing certain strategies (e.g., proxy voting).

(1) Guidance Applicable to All Funds

For funds that use one or more ESG strategies (i.e., an ESG Strategy Fund), whether such strategy is employed as the principal investment strategy or as part of the process in selecting an investment, disclosure of the ESG-related aspects of the funds’ process and strategy is required. Such disclosure “must be written using plain language”.

Additionally, according to the CSA Staff’s view, for any ESG factors used, the disclosure should identify such factors, explain their meaning (e.g., what is meant by “clean air”), and explain how they are evaluated (e.g., whether quantitative or qualitative evaluation) and monitored; and for any specific ESG-related metrics used as targets (e.g., carbon emissions), funds are encouraged to disclose identify the targets and how such targets “may change over time”.

Where a fund “may invest in companies that appear to be inconsistent with ESG values”, the CSA Staff’s view is that an ESG Fund should “disclose whether it may, at any point in time, hold such investments, what those holdings would include (including examples), and how such holdings meet the fund’s investment objectives”; where such holdings are not permitted, clearly state such prohibition along with describing how such exclusion is monitored to ensure compliance; and where the ESG Fund has discretion as to whether such holdings can be included, then similarly disclose such discretion.

(2) Guidance Applicable Only To Funds Employing Certain Strategies

For funds using proxy voting and/or shareholder engagement as part of their ESG strategy, the investment strategy disclosure should include, with respect to such proxy voting and/or shareholder engagement, the criteria used, the goal of the use of such strategy and the “extent of the monitoring process used to assess the success of such strategy.”

For funds using multiple ESG strategies, the investment strategy disclosure must explain “how the different ESG strategies are applied during the investment selection process”, and according to the CSA Staff’s view, “should include the order in which the strategies are applied, if the strategies are not applied simultaneously” (e.g., first negative screening followed by ESG integration).

For funds using ESG ratings, scores, indices or benchmarks (the “Ratings”), the investment strategy disclosure should “explain how […such Ratings] are used,” and according to the CSA Staff’s view, also both identify the “provider of the ratings or scores” or “index or benchmark used”, as applicable, and describe “the methodology used to create the company-level ESG ratings or scores, or ESG-related indices or benchmarks” (e.g., whether based on “quantitative or qualitative data” and the “level of subjectivity involved in the methodology.”)

IV. Proxy Voting and Shareholder Engagement Policies and Procedures

For funds using proxy voting and/or shareholder engagement as part of their ESG strategy, in addition to specifically disclosing that in the investment strategy (as described above in Section C. III.2), the following considerations are also applicable:

funds using proxy voting must “include a summary of the ESG aspects of the fund’s proxy voting policies and procedures” in the prospectuses and/or annual information form, as applicable; and

though funds using shareholder engagement is not required to disclose its shareholder engagement policies and procedures, the CSA Staff encourages such disclosure to be made for the sake of transparency.

V. Risk Disclosure

In evaluating what material risks to disclose, the following risk factors should be considered and disclosed where applicable:

for all funds, any applicable “material ESG-related risk factors” – e.g., “climate change risk and bribery and corruption risk”; and

specifically for ESG-Related Funds, any applicable “material risk factors” which arise as a “result of the fund’s ESG-related investment objectives and/or its use of ESG strategies” – e.g., concentration risk or potential over-reliance on third-party ESG ratings.

VI. Suitability

In drafting the suitability statement, a fund should “accurately reflect the extent of the fund’s focus on ESG as well as the particular aspect(s) of ESG that the fund is focused on, but only if applicable.” Furthermore, as per the CSA Staff’s view:

to the extent funds are “only focused on a particular” ESG issue – e.g., gender diversity in leadership – then the suitability statement should “accurately reflect” that issue; and

ESG Strategy Funds “should not state that the fund is particularly suitable for investors who have ESG-related investment objectives, as the fund does not have ESG-related investment objectives.”

VII. Continuous Disclosure

In preparing the MRFP’s (management report of fund performance) summary of the results of operations for the financial year-end, funds should consider the following disclosures:

for ESG-Related Funds, disclosure should include “how the composition and changes to the composition of the investment portfolio relate to the fund’s ESG-related investment objectives and/or strategies – e.g., disclosing the divestment, and rationale, of certain holdings with ESG issues;

for ESG Funds, in addition to the required financial performance disclosure, the CSA Staff encourages disclosing “ESG-related aspects” when describing the fund’s results of operations – e.g., the progress or outcome of the ESG issues that the fund listed in its objectives, such as climate change;

for funds using proxy voting as an ESG strategy, the CSA Staff encourages “disclosure about how the past proxy voting records during that period align with the ESG-related investment objectives and/or strategies of the fund”, in addition to making all (and not just the prior year) historical proxy voting records available on the funds’ website; and

for funds using shareholder engagement as an ESG strategy, the CSA Staff encourages disclosing “how the fund’s past shareholder engagements during that period align with the ESG-related investment objectives and/or strategies of the fund”, in addition to listing “past shareholder engagement activities” on the funds’ website.

VIII. Sales Communications

Funds should ensure that ESG-related sales communications (“Communications”) are “not untrue or misleading” and are “consistent with a fund’s regulatory offering document.” To achieve this, the Guidance first describes various issues related to Communications generally, and then provides suggestions as to how to avoid potential issues specifically related to Communications that include fund-level ESG ratings, scores or rankings. We discuss these in turn.

(1) Potential issues with ESG-Related Communications

(a) Communications Indicating That a Fund is Focused on ESG

Communications should “accurately reflect the extent to which the fund is focused on ESG, as well as the particular aspect(s) of ESG”. This means that Communications should not state that a fund is “focused on ESG” unless, in the CSA Staff’s views, that focus is reflected in the fund’s investment objectives, and if absent from the objectives but included in the investment strategies, then the fund’s focus on ESG “should not be exaggerated.” If absent from both the investment objectives and strategies, then the fund should not “include any ESG-related claims about what the fund is trying to achieve.”

The Guidance lists the following examples of misleading Communications in this respect: “(i) suggest that a fund is focused on ESG when it is not; (ii) suggest that a fund is focused on all three components of ESG when it is only focused on one component, such as governance; (iii) misrepresent the extent and nature of the fund’s use of ESG strategies, including: (1) in the case of a fund that has a discretionary or optional screening strategy, stating that the fund uses a negative or exclusionary screening strategy without clearly disclosing that the screening is discretionary or optional; or (2) failing to: (A) disclose that there is a maximum limit to the fund’s use of those strategies; (B) actually use the advertised ESG strategies, including using different types of ESG strategies altogether; or (C) prominently disclose material aspects of the ESG strategies” [notations added].

(b) Communications Referencing a Fund’s ESG Performance

Communications should not include “misleading statements […] about the ESG performance of the fund.”

The Guidance lists the following examples of misleading Communications in this respect: “(i) make inaccurate claims about the fund’s ESG performance or results; (ii) make inaccurate claims about the existence of a direct causal link between the fund’s investment strategies and ESG performance or results; or (iii) manipulate elements of disclosure to present the fund’s ESG performance or results in a positive light, such as cherry-picking data” [notations added].

(c) Communications Including Fund-Level ESG Ratings, Scores or Rankings

Communications disclosing fund-level ESG ratings, scores or rankings (the “Metrics”) deemed to be “performance data” or a “performance rating or ranking”, and/or comparisons of such Metrics deemed to be “comparison of performance” risk being noncompliant with Part 15 of National Instrument 81-102.

Notwithstanding the foregoing, the CSA Staff’s view is that, from what they have observed to date, Portfolio-Based ESG Ratings and Portfolio-Based ESG Rankings (both defined below), and comparisons of each, are neither “performance data” nor “performance ratings or rankings”, nor “comparisons of performance.”

“Portfolio-Based ESG Ratings” means “fund-level ESG ratings or scores that are primarily weighted averages of the company-level ESG ratings or scores of the underlying portfolio holdings of the fund”; and “Portfolio-Based ESG Rankings” means “fund-level ESG rankings based solely on Portfolio-Based ESG Ratings”.

In addition to concerns around performance-related requirements, the Guidance lists the following four examples of additional issues (the “Four Issues”) which may result in misleading Communications in this respect: “(i) there are conflicts of interest involving the provider that prepares the fund-level ESG rating, score or ranking; (ii) the selection of the specific fund-level ESG rating, score or ranking is the result of cherry-picking fund-level ESG ratings, scores or rankings in order to present the fund’s ESG characteristics or performance in a positive light; (iii) the selected fund-level ESG rating, score or ranking is not representative of the ESG characteristics or performance of the fund; [and] (iv) the sales communication does not include explanations, qualifications, limitations or other statements necessary or appropriate to make the inclusion of the fund-level ESG ratings, scores or rankings in the sales communication not misleading” [notations added].

(2) Avoiding Misleading Communications Including Fund-Level ESG Metrics

The CSA has provided the following suggestions which, in the CSA Staff’s view, can help to avoid misleading Communications with respect to each of the Four Issues:

To avoid conflicts of interest, the ESG Metrics provider should consistently apply an objective methodology when determining such Metrics, disclose such methodology, not be a “member of the organization” of the fund, not be “paid to assign a fund-level ESG rating, score or ranking to the fund by the promoter, manager, portfolio adviser, principal distributor or participating dealer of any fund or any of their affiliates”; and specifically for ESG rankings, such rankings “should be based on a published category of funds, such as Canadian equity funds.”

To avoid “cherry-picking”, the following parameters should be considered when selecting Metrics:

IFMs need to evaluate whether the Metric is “an accurate representation of the fund (and its portfolio, if the fund-level ESG rating, score or ranking is based on the fund’s portfolio) during the time period that the […Communication] appears or is in use”;

“for a fund-level ESG ranking, the ranking should be based on a published category of funds, such, as for example, Canadian fixed income funds, that provides a reasonable basis for evaluating the ESG characteristics or performance of the fund;”

where a non-ESG Fund discloses a Metric on its website, “the IFM should disclose the same type of fund-level ESG rating, score or ranking from the same provider, if available, for all of the funds that it manages”;

where an ESG Fund, other than those with a specialized ESG focus (e.g., climate change), discloses a Metric on its website, “the IFM should disclose the same type of fund-level ESG rating, score or ranking from the same provider, if available, for all of the ESG Funds that it manages”; and

where funds want to disclose Metrics in their Communications, the CSA Staff “encourages” disclosing such Metrics from “at least 2 different providers.”

To avoid inaccurately representing the fund’s ESG characteristics or performance, where “only a certain percentage [i.e., less than 100%] of a fund’s underlying portfolio has been rated” or ranked, then IFMs should evaluate whether the non-rated portion of the portfolio “has substantially similar ESG characteristics” to the remaining portfolio, and relatedly, whether the Portfolio-Based ESG Rating or Portfolio-Based ESG Ranking is “an accurate representation […] of the entire portfolio.”

To avoid misleading Communications, the CSA sets out on pages 22-24 of its Guidance various accompanying disclosures to include, such as the date or time period covered by the Metric or certain cautionary language.

IX. ESG-Related Changes to Existing Funds

Depending on the change, prior approval of securityholders is required in certain instances where a fund changes either its fund name or investment objectives to reference ESG considerations. Whether such approval is required in illustrated by Figure 2, as follows:

Source: Guidance, page 25.

X. ESG-Related Terminology

In addition to the requirement that disclosure be “written in plain language”, such disclosure should also “provide a clear explanation” of ESG-related terms which are used but “not commonly understood.”

XI. IFM-Level Commitments to ESG-Related Initiatives

For funds that have signed up or committed to certain international or regional ESG initiatives – e.g., United Nations Principles for Responsible Investment – the disclosure should clearly note that the initiative is “at the entity-level rather than at the fund-level and where applicable, that the funds managed by the IFM may not be focused on ESG.”

The Ontario Securities Commission, in its January 19, 2022 press release, summarizes the purpose of the Guidance and the direction in which ESG investing in Canada is heading:

“Interest in ESG investing is on the rise and this enhanced and practical guidance will play an important role in helping investors make informed decisions about ESG products, as well as preventing potential greenwashing,” said Louis Morisset, CSA Chair and President and CEO of the Autorité des marchés financiers.

This guidance is intended to help investment funds and their fund managers enhance the ESG-related aspects of the funds’ regulatory disclosure documents and ensure that sales communications of ESG-Related Funds are not untrue or misleading and are consistent with the funds’ regulatory offering documents.”

If you need any assistance in interpreting or applying the Guidance, or any other ESG-related queries, feel free to reach out to Stephen Erlichman, John Kruk, Dyna Zekaoui or any other member of Fasken’s ESG Group or Investment Products and Wealth Management Group.

Stephen Erlichman, LLM (NYU), MBA (Harvard), Responsible Investment Professional Certification (RIA), Certificate in Sustainable Capitalism & ESG (UC Berkeley Law). From 2011 to 2018 Stephen was the Executive Director of the Canadian Coalition for Good Governance.

John Kruk, LL.B (Toronto). John is a securities lawyer specializing in investment funds, structured products, and registrant compliance.

Dyna Zekaoui, JD and LLM-LE (Duke University). Dyna is a member of Fasken’s ESG team and advises clients regularly on ESG-related issues.

TORONTO – Canada’s main stock index was up more than 100 points in late-morning trading, helped by strength in base metal and utility stocks, while U.S. stock markets were mixed.

The S&P/TSX composite index was up 103.40 points at 24,542.48.

In New York, the Dow Jones industrial average was up 192.31 points at 42,932.73. The S&P 500 index was up 7.14 points at 5,822.40, while the Nasdaq composite was down 9.03 points at 18,306.56.

The Canadian dollar traded for 72.61 cents US compared with 72.44 cents US on Tuesday.

The November crude oil contract was down 71 cents at US$69.87 per barrel and the November natural gas contract was down eight cents at US$2.42 per mmBTU.

The December gold contract was up US$7.20 at US$2,686.10 an ounce and the December copper contract was up a penny at US$4.35 a pound.

This report by The Canadian Press was first published Oct. 16, 2024.

TORONTO – Canada’s main stock index was up more than 200 points in late-morning trading, while U.S. stock markets were also headed higher.

The S&P/TSX composite index was up 205.86 points at 24,508.12.

In New York, the Dow Jones industrial average was up 336.62 points at 42,790.74. The S&P 500 index was up 34.19 points at 5,814.24, while the Nasdaq composite was up 60.27 points at 18.342.32.

The Canadian dollar traded for 72.61 cents US compared with 72.71 cents US on Thursday.

The November crude oil contract was down 15 cents at US$75.70 per barrel and the November natural gas contract was down two cents at US$2.65 per mmBTU.

The December gold contract was down US$29.60 at US$2,668.90 an ounce and the December copper contract was up four cents at US$4.47 a pound.

This report by The Canadian Press was first published Oct. 11, 2024.

TORONTO – Canada’s main stock index was little changed in late-morning trading as the financial sector fell, but energy and base metal stocks moved higher.

The S&P/TSX composite index was up 0.05 of a point at 24,224.95.

In New York, the Dow Jones industrial average was down 94.31 points at 42,417.69. The S&P 500 index was down 10.91 points at 5,781.13, while the Nasdaq composite was down 29.59 points at 18,262.03.

The Canadian dollar traded for 72.71 cents US compared with 73.05 cents US on Wednesday.

The November crude oil contract was up US$1.69 at US$74.93 per barrel and the November natural gas contract was up a penny at US$2.67 per mmBTU.

The December gold contract was up US$14.70 at US$2,640.70 an ounce and the December copper contract was up two cents at US$4.42 a pound.

This report by The Canadian Press was first published Oct. 10, 2024.