Investors around the globe are bracing for tomorrow’s Federal Reserve decision, while wading through the latest batch of corporate earnings.

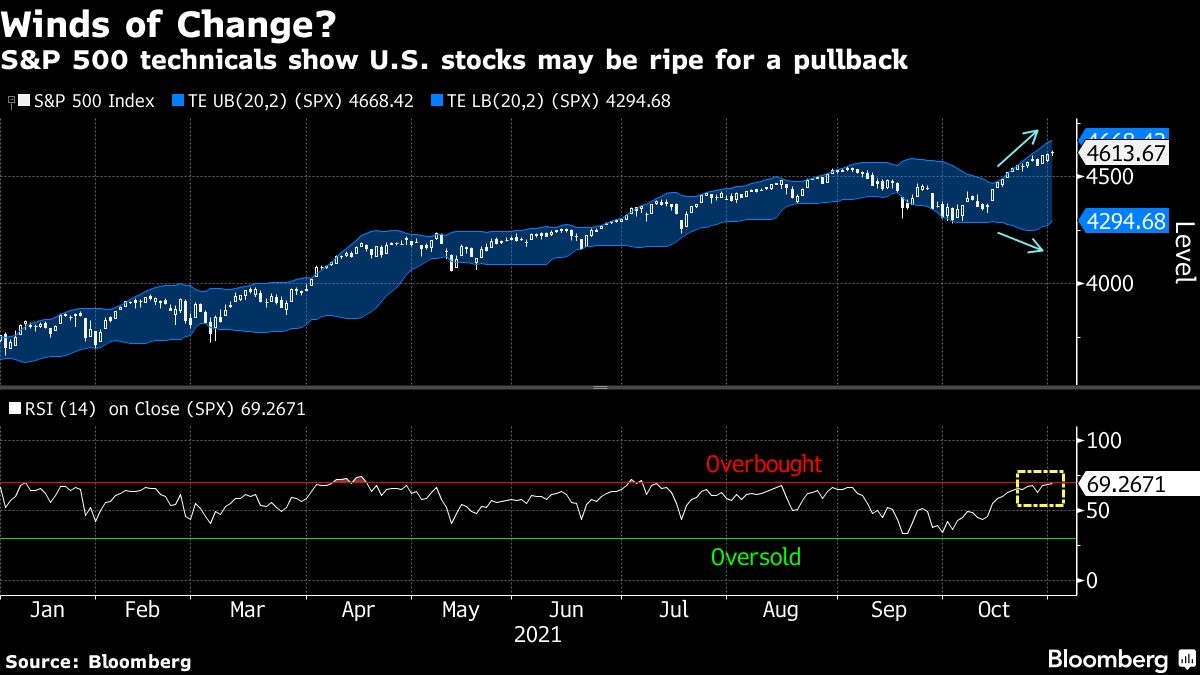

Equities were mixed as a third straight record close for the S&P 500 — its 60th this year — had some technical indicators flashing signs of caution. With policy makers expected to announce they will start scaling back their massive asset-purchase program, economists surveyed by Bloomberg are closely divided on whether a rate hike will be next year or early 2023, with a slim majority estimating the latter timing.

“The Fed has managed expectations perfectly in terms of preparing the markets for what is likely to be speed tapering,” said Win Thin, global head of currency strategy at Brown Brothers Harriman. “Most officials seem to agree that it’s better to get tapering over as quickly as possible in order to leave the Fed maximum flexibility to hike rates when needed.”

Some corporate highlights:

- Tesla Inc. is giving back some the gains since Hertz Global Holdings Inc. announced a massive order for its electric vehicles after Elon Musk cast doubt on the deal and downplayed its potential.

- Pfizer Inc. raised its forecast for the year on the strength of sales of its COVID-19 vaccine, although the company sees revenue from the shot falling in 2022.

- Under Armour Inc. surged after raising its full-year outlook and reporting quarterly revenue that surpassed analysts’ predictions, with strong consumer demand for athletic gear offsetting widespread issues in the global supply chain.

- Rogers Corp. surged after chemical company DuPont de Nemours Inc. agreed to buy the engineering materials maker for US$5.2 billion.

Not only is the S&P 500 pushing the limits of its trading envelope — built around moving price averages — but the widening of its upper and lower bands can also be a precursor to greater swings. Furthermore, the S&P 500’s 14-day relative strength index is on the cusp of breaching 70, seen by some traders as a threshold for being considered overbought.

Here are some events to watch this week:

- Fed rate decision, U.S. factory orders and durable goods, Wednesday

- OPEC+ meeting on output, Thursday

- Bank of England rate decision, Thursday

- U.S. trade, initial jobless claims, Thursday

- U.S. unemployment, nonfarm payrolls, Friday

Some of the main moves in markets:

Stocks

- The S&P 500 rose 0.1 per cent as of 9:33 a.m. New York time

- The Nasdaq 100 was little changed

- The Dow Jones Industrial Average rose 0.1 per cent

- The Stoxx Europe 600 was little changed

- The MSCI World index was little changed

Currencies

- The Bloomberg Dollar Spot Index was little changed

- The euro was little changed at US$1.1598

- The British pound fell 0.1 per cent to US$1.3649

- The Japanese yen rose 0.2 per cent to 113.79 per dollar

Bonds

- The yield on 10-year Treasuries was little changed at 1.55 per cent

- Germany’s 10-year yield declined five basis points to -0.15 per cent

- Britain’s 10-year yield declined two basis points to 1.04 per cent

Commodities

- West Texas Intermediate crude fell 0.9 per cent to US$83.32 a barrel

- Gold futures fell 0.2 per cent to US$1,791.60 an ounce