capitalism")

From December 6 to 11, 2020, China and the EU held the 35th round of negotiations on the Comprehensive Agreement on Investments (“CAI”), a bilateral treaty that will replace the 26 existing bilateral investment treaties between 27 individual EU Member States and China, thus providing a uniform legal framework for EU-China investment ties.

The necessity of this agreement is due to the increased cooperation between China and the EU, and to the high volumes of bilateral trade and investments (especially from the EU to China), that makes the urgency of shared principles and rules more and more appreciable.

According to Eurostat data, in 2019 the EU had exported goods worth approximately €198 billion (US$242 billion) to China and imported goods worth €362 billion (US$442 billion) from China, with a bilateral trade worth some US$650 billion last year, according to Bloomberg.

With reference to investments in 2019, Chinese foreign direct investment in the EU continued to decline, mirroring the decline in Chinese outbound investments globally. However, China continued to be the second largest FDI recipient after the US counting – according to Rhodium Group – US$1.6 billion of newly announced FDI projects by EU companies in China in the last quarter of this year.

The CAI’s main objectives would be an enhanced protection of EU investments in China and vice versa, improved legal certainty regarding the treatment of EU investors in China, reduction of barriers to investing in China, and as a result, increasing bilateral investment flows and improved access to the Chinese market.

CAI core focus

Notwithstanding the fact that the content of the articles of the investment agreement has not yet been disclosed to the public, the cornerstones of the agreement can be summarized as follows:

- Provide for new opportunities and improved conditions for access to the EU and Chinese markets for Chinese and EU investors (more specifically, broadening the EU investors’ access to the Chinese market by eliminating quantitative restrictions, equity caps, or joint venture requirements);

- Address key challenges of the regulatory environment, including those related to transparency, predictability, and legal certainty of the investment environment (with reference to the Chinese market, by allowing EU investors to have access to information affecting their business, but also giving them opportunity to comment on relevant laws and regulations, as well as ensuring clear, fair, and transparent procedures);

- Establish guarantees regarding the treatment of EU investors in China and of Chinese investors in the EU, including protection against unfair and inequitable treatment, unlawful discrimination, and unhindered transfer of capital and payments linked to an investment;

- Ensure a level playing field by pursuing, inter alia, non-discrimination as a general principle subject to a limited number of clearly defined situations;

- Support to sustainable development initiatives by encouraging responsible investment and promoting core environmental and labour standards;

- Allow for the effective enforcement of commitments through investment dispute settlement mechanisms available to the contracting Parties and to investors.

It shall be noted that the main content of the agreement will be based on specific EU requests towards China regarding reforms and amendments of its investments’ legal framework. This is because under the EU perspective and based on the EU companies’ experiences in China, the Chinese laws do not grant the same rights and obligations to both, domestic and foreign companies, thus creating asymmetries between enterprises based on their nationality. Hence, with the CAI, the EU seeks to create new investment opportunities for European companies by opening China’s market and eliminating discriminatory laws and practices.

In the light of above, it is clear how the innovation brought by the CAI lies in the wide scope of this agreement, that, unlike the BITs that cover only the post-entry protection of investment, should also include provisions for the pre-entry phase (ensuring that foreign investors have the same market access as domestic investors), as well as provisions on investment-related sustainable development, level playing field issues, such as transparency of subsidies and rules on SOEs and forced technology transfer.

Long-lasting negotiations

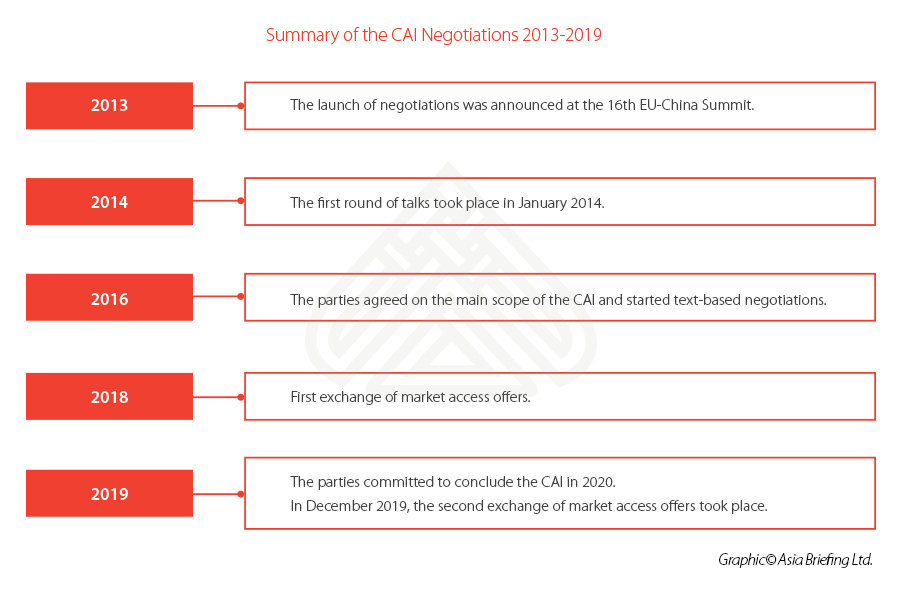

The negotiations of the EU-China CAI were first announced in October 2013, when the European Council adopted a mandate for the Commission to negotiate an investment agreement with China on behalf of the EU, and, in November 2013 the launch of negotiations was announced at the 16th EU-China Summit.

The first round of talks took place in January 2014, but only in 2016 the parties agreed upon the main scope of the CAI and moved on to specific text-based negotiations.

At the 20th EU-China Summit in July 2018, the parties had a first exchange of market access offers against the backdrop of persisting policy divergences on core investment provisions, and at the 21st EU-China Summit in April 2019, the parties committed to conclude the CAI in 2020.

During this phase of negotiations, from the 20th to 24th rounds, the parties discussed some major topics, including rules on financial services, capital transfer, national treatment related commitments, state-to-state dispute settlement, and investment-related issues concerning sustainable development.

At the 25th round in December 2019, the second exchange of market access offers took place.

Here below a short summary of the negotiations from 2013 to 2019:

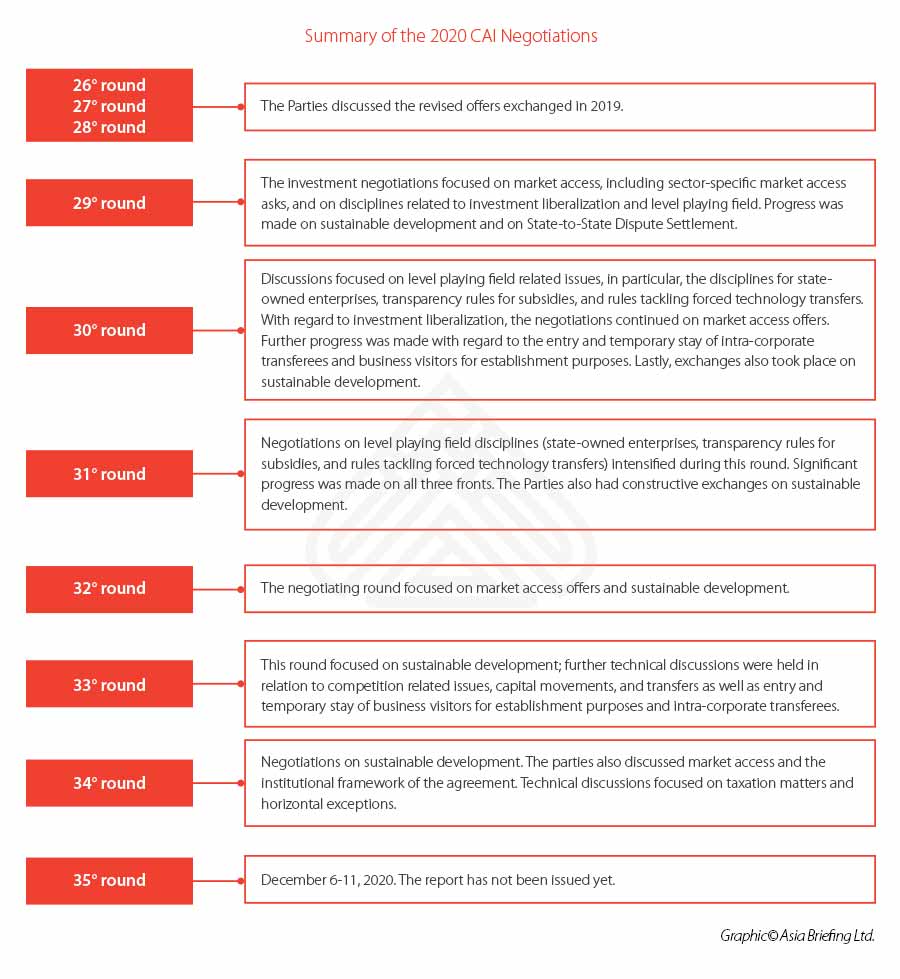

Since the decision made by the parties to conclude the CAI within 2020, the number of rounds intensified and from January to December 2020 China and EU held several meetings.

Starting from the beginning of this year, from the 26th round to 28th round, the parties discussed the revised offers exchanged in 2019, while during the 30th and 31st rounds, the dialogues continued and covered level-playing field issues, including disciplines on SOEs, transparency of subsidies, and forced technology transfers – bringing a significant progress in the negotiations.

Despite this, according to the press release on the 8th EU-China High-level Economic Dialogue (July 28, 2020), much work remained to be done on market access in the telecommunication sectors, health, biotechnology, new energy vehicles, and sustainable development.

The 32nd round, held from 21st to 25th September 2020, focused on sector-specific market access and the mechanism for addressing differences on sustainable development, but some progress was also registered with reference to the rules on entry and stay of business visitors and intra-corporate transferees.

The 33rd and 34th rounds negotiations – held respectively on October 19-23, 2020 and November 16-20, 2020 – focused, among others, on sustainable development, competition related issues, capital movements, and transfers as well as entry and temporary stay of business visitors for establishment purposes and intra-corporate transferees. In addition, they discussed about taxation matters and horizontal exceptions.

The 35th round held from December 6-11, 2020 will likely not be the last one, but according to state media Xinhua, the Chinese Ministry of Commerce had released a statement announcing that positive progress was made in the negotiations with the EU.

Here we provide a short summary of the 2020 CAI Negotiations:

What are the main obstacles to concluding the CAI?

China and the EU made considerable progress on the CAI negotiations, but there are still some important topics on which the parties have not reached an agreement yet, and that will have to be further discussed.

The negotiations are now focused on some EU major requests concerning the opening of Chinese market (which is still restricted to foreign investors in key sectors, such as telecommunication services, information and communication technology, health, biotechnology, financial services, and manufacturing), and sustainable development.

Considering the broad content of the CAI and the positive impact that it may have on the flow of investments, the signature of the CAI would be a turning point in China-EU relations, indeed leaders of both parties have expressed several times their will to reach such an agreement.

However, EU leaders remarked that China must commit to implement concrete reforms in its legal system to remove the asymmetries existing on the Chinese market – for instance, the more favourable treatment granted to SOEs compared to private companies, or the restricted access to certain industries to foreign investors – thus posing this as a condition for the signature of the CAI.

On the other side, to quote President Xi Jinping’s words: “the two sides should adopt a positive and pragmatic attitude, speed up negotiations on the China-EU investment agreement to achieve the goal of completing the negotiations by the end of this year, working to upgrade cooperation, facilitate the post-epidemic world economic recovery and jointly safeguard an open trade and investment environment”.

Looking forward, what can we expect?

In light of the above, the relevance of such agreement is clear, but there are doubts that the parties will be able to reach an agreement by the end of this year. The delay may also be attributed to the election of the new US president; once Joe Biden gets sworn into office in January, China and the EU will likely have to re-evaluate their relations with the US and this may have an impact on CAI negotiations.

To this regard, the Biden White House’ approach towards both China and the EU will have a significant impact on the global economy and international relations. If the three major economies can find an alignment, this will be for the benefit of the whole world. In this context, the CAI may represent not only a strong foundation towards a sustainable cooperation between China and the EU but can also provide a reference point for China-US bilateral negotiations about issues, such as the Phase Two trade deal. If this will be the case, the relations among China, EU and the US will be based on similar principles and will tend to achieve similar goals, thus curtailing both current and potential conflicts in the future.

About Us

China Briefing is written and produced by Dezan Shira & Associates. The practice assists foreign investors into China and has done so since 1992 through offices in Beijing, Tianjin, Dalian, Qingdao, Shanghai, Hangzhou, Ningbo, Suzhou, Guangzhou, Dongguan, Zhongshan, Shenzhen, and Hong Kong. Please contact the firm for assistance in China at [email protected].

We also maintain offices assisting foreign investors in Vietnam, Indonesia, Singapore, The Philippines, Malaysia, Thailand, United States, and Italy, in addition to our practices in India and Russia and our trade research facilities along the Belt & Road Initiative.