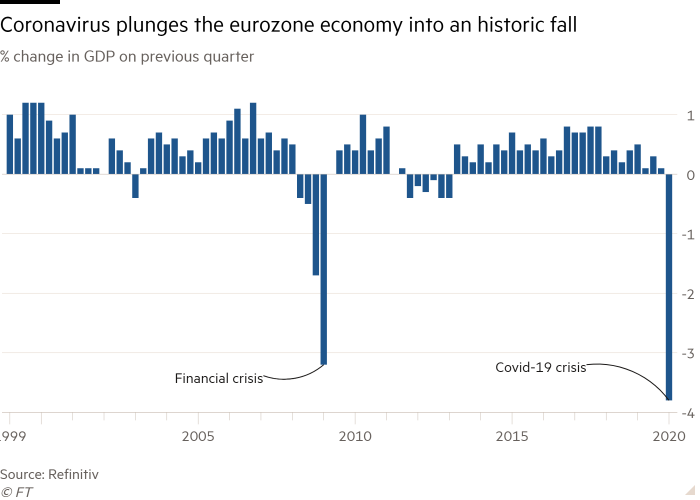

The eurozone’s economy shrank by the fastest rate on record in the first quarter of 2020 as measures to contain the coronavirus pandemic froze business and household activity, figures published on Thursday showed.

The gross domestic product of the eurozone fell by 3.8 per cent in the first quarter compared with the previous quarter, preliminary estimates from Eurostat found. This is the largest drop since the series began in 1995, and a deeper drop than the worst of the financial crisis.

The contraction in the eurozone was worse than that experienced by the US, where the economy contracted by 1.2 per cent quarter on quarter, or 4.8 per cent at an annualised rate, according to data published on Wednesday.

The grim economic news is likely to add to pressure on the European Central Bank to step up its measures to shield the eurozone economy from the full force of the pandemic when it announces its latest monetary policy decision on Thursday afternoon. Christine Lagarde, ECB president, warned EU leaders last week that eurozone GDP could fall 15 per cent this year.

France, Spain and Italy — three of the bloc’s four biggest economies — all experienced record quarterly contractions in GDP in the first three months of 2020, figures published separately on Thursday showed, and two of the three entered recession.

France’s GDP dropped 5.8 per cent in the first quarter compared with the previous quarter, according to preliminary estimates from Insee, the country’s national statistics office, the biggest fall since records began in 1949. The French economy contracted by 0.1 per cent in the final quarter of 2019, which means it has now entered a recession, defined as two consecutive quarters of output contraction.

Italy’s GDP fell 4.7 per cent in the first quarter compared with the previous quarter, according to data from Istat, the national statistics office. This was less than economists had predicted but was still the largest contraction since records began in 1996 and steeper than the 2.8 per cent contraction in the first quarter of 2009.

The Italian economy had contracted 0.3 per cent in the final quarter of 2019, which means Italy is also in recession, its fourth in just over a decade.

Meanwhile, Spain’s gross domestic output shrank 5.2 per cent in the same period, according to preliminary estimates from the national statistics institute INE, ending more than six years of uninterrupted growth, most of which was well above the pace of the eurozone average. This was the largest fall since the series began in 1995.

The region’s economy is expected to fall even further in the second quarter, given that most European governments only started to impose a lockdown on households and businesses in early March. The pandemic is expected to trigger the worst recession in the global economy since the Great Depression of the 1930s.

Christoph Weil, economist at Commerzbank, said: “The second quarter is likely to be even more catastrophic, as it will be even more affected by the lockdown.”

The risk of Europe’s economy entering a deflationary spiral increased as falling energy prices dragged eurozone inflation down from 0.7 per cent in March to 0.4 per cent in April — the lowest level of price growth for almost four years. Spain, Greece, Slovenia and Finland all reported falling prices.

Separate data from Germany’s Federal Employment Agency (BA) showed that more than 10m German workers have been registered to have part of their wages paid by the state while they are idled by their employers in response to the coronavirus crisis. That means almost a quarter of all German workers have been sent home or put on partial hours during the pandemic.

Despite this, jobless numbers rose in Germany by 308,000 to 2.64m in April, pushing up the unemployment rate from 5.1 per cent to a three-year high of 5.8 per cent. Detlef Scheele, head of the BA, warned that the labour market was “under considerable pressure”.

Coronavirus business update

How is coronavirus taking its toll on markets, business, and our everyday lives and workplaces? Stay briefed with our coronavirus newsletter.

Germany this week forecast that over the whole year its economy would contract by 6.3 per cent, before rebounding next year. On Thursday, data showed that German retail sales fell 5.6 per cent in March, the fastest decline in more than a decade.

Italy’s unemployment rate fell to 8.4 per cent in March, Istat reported on Thursday. Yet, the figure “should not provide much comfort” said Andrew Kenningham, chief Europe economist at Capital Economics, “as it reflects the large number of people absorbed by government furlough schemes and a decline in labour force participation as people gave up on looking for a job”.

Florian Hense, an economist at Berenberg, said the first-quarter shrinkage in France’s economy had wiped out four years of growth, adding that the country’s “more stringent government measures should better contain the Covid-19 pandemic, but they also hit economic activity harder”.

Earlier this week, Edouard Philippe, prime minister of France, announced plans to reopen parts of the economy from May 11 to avoid the risk of economic “collapse”.

TORONTO – Strength in the base metal and technology sectors helped Canada’s main stock index gain almost 100 points on Friday, while U.S. stock markets also climbed higher.

The S&P/TSX composite index closed up 93.51 points at 23,568.65.

In New York, the Dow Jones industrial average was up 297.01 points at 41,393.78. The S&P 500 index was up 30.26 points at 5,626.02, while the Nasdaq composite was up 114.30 points at 17,683.98.

The Canadian dollar traded for 73.61 cents US compared with 73.58 cents US on Thursday.

The October crude oil contract was down 32 cents at US$68.65 per barrel and the October natural gas contract was down five cents at US$2.31 per mmBTU.

The December gold contract was up US$30.10 at US$2,610.70 an ounce and the December copper contract was up four cents US$4.24 a pound.

This report by The Canadian Press was first published Sept. 13, 2024.

OTTAWA – Statistics Canada says wholesale sales, excluding petroleum, petroleum products, and other hydrocarbons and excluding oilseed and grain, rose 0.4 per cent to $82.7 billion in July.

The increase came as sales in the miscellaneous subsector gained three per cent to reach $10.5 billion in July, helped by strength in the agriculture supplies industry group, which rose 9.2 per cent.

The food, beverage and tobacco subsector added 1.7 per cent to total $15 billion in July.

The personal and household goods subsector fell 2.5 per cent to $12.1 billion.

In volume terms, overall wholesale sales rose 0.5 per cent in July.

Statistics Canada started including oilseed and grain as well as the petroleum and petroleum products subsector as part of wholesale trade last year, but is excluding the data from monthly analysis until there is enough historical data.

This report by The Canadian Press was first published Sept. 13, 2024.

TORONTO – Canada’s main stock index was up more than 150 points in late-morning trading, helped by strength in the base metal and energy sectors, while U.S. stock markets were mixed.

The S&P/TSX composite index was up 172.18 points at 23,383.35.

In New York, the Dow Jones industrial average was down 34.99 points at 40,826.72. The S&P 500 index was up 10.56 points at 5,564.69, while the Nasdaq composite was up 74.84 points at 17,470.37.

The Canadian dollar traded for 73.55 cents US compared with 73.59 cents US on Wednesday.

The October crude oil contract was up $2.00 at US$69.31 per barrel and the October natural gas contract was up five cents at US$2.32 per mmBTU.

The December gold contract was up US$40.00 at US$2,582.40 an ounce and the December copper contract was up six cents at US$4.20 a pound.

This report by The Canadian Press was first published Sept. 12, 2024.