A goldilocks approach to investment risk, where your portfolio is neither too hot nor too cold, becomes more important the closer you get to retirement.

Take too much risk, and you could blow up your portfolio and experience lean years rather than golden years in retirement.

Conversely, by avoiding risk you may fail to generate the wherewithal to sustain your lifestyle during your later years.

“You can lock in a term deposit or fixed income investments, but if you’re a retiree with 25 years to live, if you go too conservative, you’re not going to get a nice outcome,” says Fidelity International’s Richard Dinham.

And the current market environment, where interest rates are at historic lows and real investment returns – when factoring in inflation – are hovering below 1 per cent. Inflation is now running at around 1.6 per cent and annual GDP growth is below 1.4 per cent.

There’s also rising speculation that central banks could cut rates again in 2020.

With interest rates falling, the return from cash-based investments alone could be expected to also be lower. People can be locking in negative or very low real rates of return if relying too heavily on cash, says Dinham.

“You need a diversified form of risk – including equity risk and credit risk – to smooth your outcomes. Equities inevitably dominates here, but it’s taking the right amount of risk is vital.”

Back to basics

A large part of the problem for those nearing retirement, or already retired, is the concept of sequencing risk. Dinham refers to this as a core concept, “a 101 of financial planning” for retirees.

This refers to the risk that market volatility will erode an individual’s superannuation balance, particularly around retirement when these amounts are at their highest.

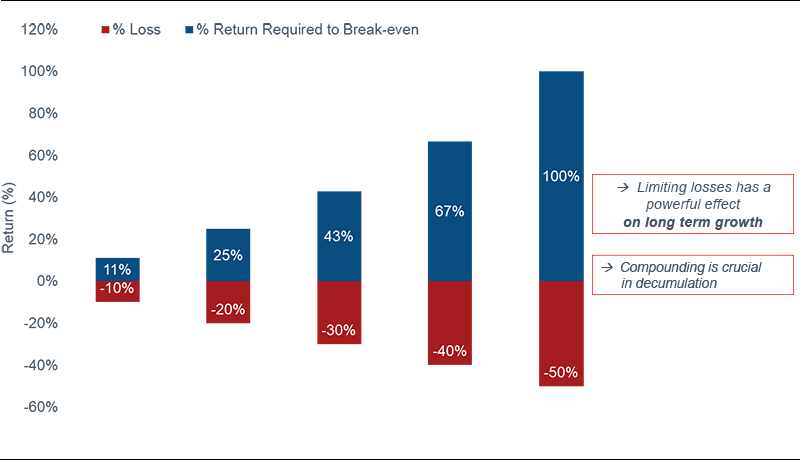

Compounding is a key element here – again, something that is generally well understood when we think about earning income and investing, but not so much in the context of retirement.

For example, let’s say you invest $100 in shares, and the share market declines by 10 per cent in the first year, and then increases by 10 per cent in the second year.

After the first year, the investment of $100 is only worth $90. At the end of the second year, that $90 in turn only grows to $99 – an overall loss of 1 per cent, or 0.5 per cent a year.

For the total amount to return to $100 again, the portfolio must return 11 per cent in the second year, not 10 per cent. The size of the returns must be large enough to offset the earlier losses.

Recovering after market losses

Source: Fidelity International

Though markets will generally recover at some point, the losses may be permanent for investors who don’t have the benefit of time to wait for this.

“It’s about finding a way of minimising the impact of markets while still remaining invested in them.”

A bucket approach to asset allocation is one commonly used method. The premise is that assets needed to fund near-term living expenses should remain in cash, as explained by Morningstar’s Christine Benz.

Assets that won’t be needed for several years or more can be parked in a diversified pool of long-term holdings, with the cash buffer enabling you to ride out periodic downturns in the long-term portfolio.

Benz recommends cash allocations should be tailored depending on your life-stage. In general, people still earning an income require less cash than those who are retired and drawing from their portfolio.

The right amount of cash also depends on your investment approach. If you’re an opportunistic investor, you may want more cash on hand to put into the market during a dip.

It’s also worth shopping around for the most attractive term deposit or other cash vehicle.