The guardians of the global economy will gather this week, one year into the pandemic, to assess the damage and chart a path forward.

The International Monetary Fund and World Bank spring meetings will take place virtually for a second year starting on Monday. The IMF will release its updated World Economic Outlook on Tuesday, with Managing Director Kristalina Georgieva already indicating that it will include an upgrade to January’s forecast for 5.5% global economic growth for 2021.

What Bloomberg Economics Says:

“A shrinking virus threat, expanding U.S. stimulus boost, and trillions of dollars in pent-up savings ready to be spent mean the world economy is poised for the fastest expansion on record back to the 1960s.”

–Tom Orlik, chief economist. For full analysis, click here

Beyond the much-watched economic report, attention will focus on a Group of 20 finance ministers’ meeting on Wednesday, where officials may decide to extend the Debt Service Suspension Initiative, set to expire in June, through the end of this year. The program has provided $5 billion in debt relief for low-income nations since it began last May, according to World Bank data.

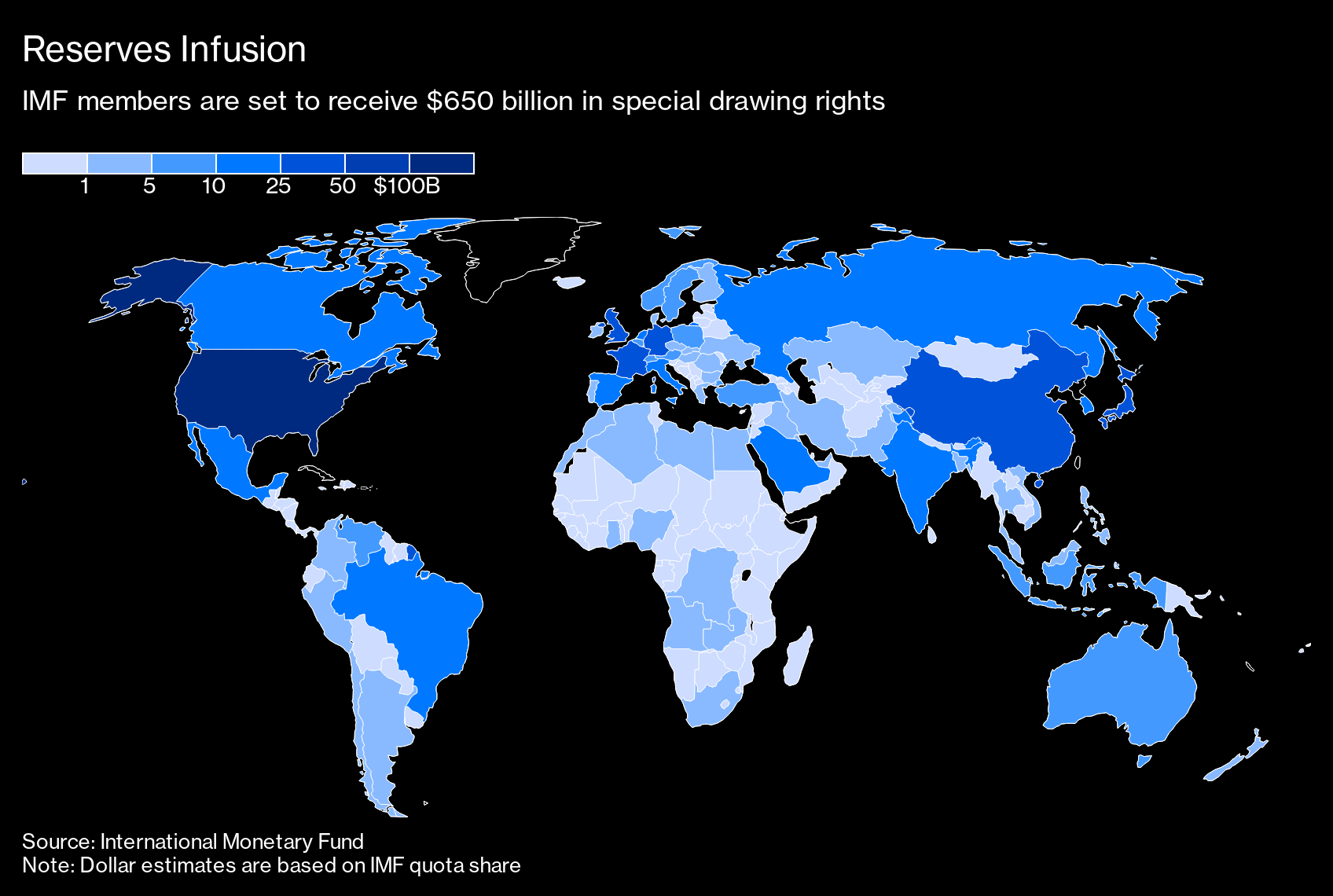

Another focus of conversation will be the IMF’s proposed $650 billion issuance of reserve assets known as special drawing rights. While the official proposal won’t come until June, Georgieva last month touted broad support for the idea among IMF members.

Reserves Infusion

IMF members are set to receive $650 billion in special drawing rights

Source: International Monetary Fund

Note: Dollar estimates are based on IMF quota share

.chart-js display: none;

The plan would help send more than $20 billion to poor countries. U.S. Treasury Secretary Janet Yellen last week told U.S. Congress that President Joe Biden’s administration intends to support the idea, starting a countdown of at least 90 days before a formal vote in favor at the IMF.

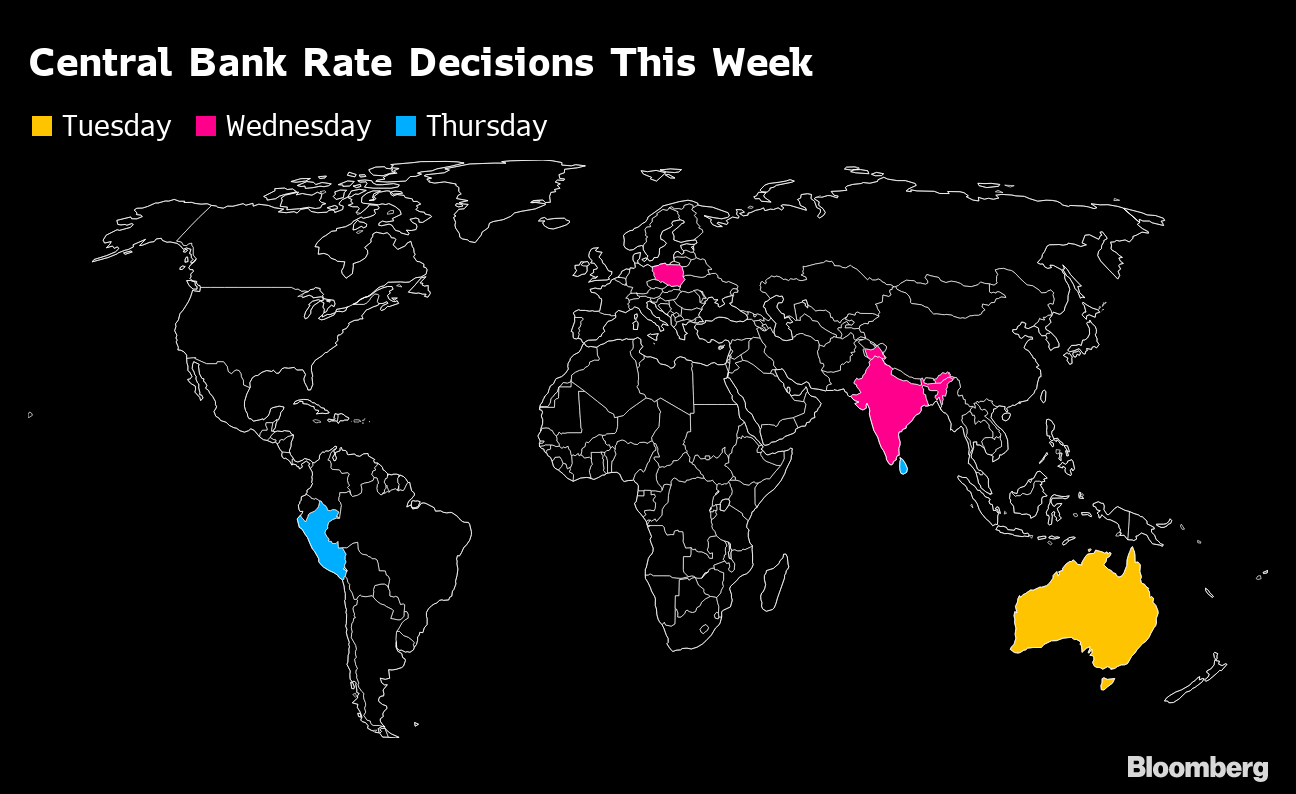

Elsewhere, minutes of the latest Federal Reserve and European Central Bank meetings will shed insight on policy makers’ thinking and central banks in India, Australia and Poland are predicted to keep policy unchanged.

Click here for what happened last week and below is our wrap of what is coming up in the global economy.

U.S. and Canada

Investors will be watching out for the latest data on services activity, job openings and producer prices for signs of the economy’s progress and developing inflationary pressures.

On Wednesday, Fed watchers will also have minutes of the central bank’s last meeting to pour through and Fed Chair Jerome Powell is scheduled to speak at an event Thursday in time with the IMF’s meeting.

Asia

Japan releases household and wage data on Tuesday that will offer more insight into the hit to the economy from a second state of emergency amid signs it was less brutal than first feared.

Central Bank Rate Decisions This Week

.chart-js display: none;

Australia has an interest rate meeting on Tuesday and India on Wednesday. With neither central bank expected to move their main policy tools, the focus will be on their outlooks.

China releases data on Friday that’s likely to show consumer price inflation climbed back into positive territory while factory costs are starting to swell.

Europe, Middle East, Africa

The health of Europe’s manufacturing base as it weathers the coronavirus crisis will focus economists’ attention in the coming week as they gauge the underlying strength of growth drivers during the quarter that just finished.

German factory orders and industrial production data for February are among the more significant reports, and both are anticipated to show output increases during the month.

A shorter week than usual in much of the region because of the Easter holiday on Monday features fewer scheduled remarks by ECB officials to guide investors on the state of policy.

But the institution’s account of its decision on March 11 will pique interest, perhaps signaling a spectrum of opinion among governors on the risks to economic growth at a meeting when they ratified new quarterly forecasts.

Poland may announce a new fiscal stimulus program, largely paid for by EU funds. Meanwhile, the country’s central bank is set to keep policy unchanged.

Turkey may report that inflation rose to above 16% in March, when the firing of Naci Agbal and appointment of Sahap Kavcioglu as central bank governor sent the lira plunging by more than 10% as foreign investors sold Turkish assets at the fastest pace in 15 years.

Russia is expected to report that inflation accelerated to the highest since 2016 at 5.8% in March, when the central bank raised interest rates to try and combat the effects of ruble weakness and rising food prices.

Latin America

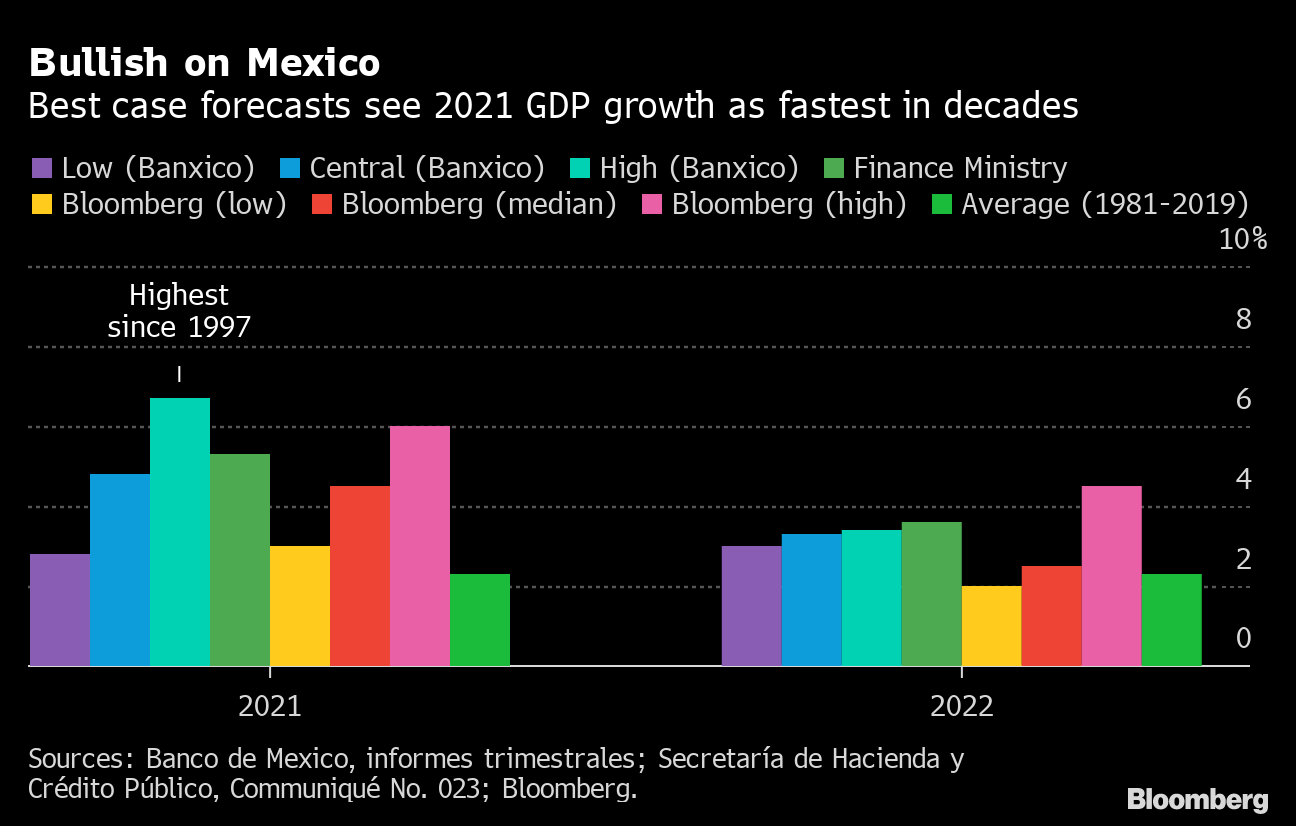

Reports on Mexico’s industrial output and manufacturing this week should point to the negative output gap of early 2021. On Thursday, the consumer price reports and the central bank minutes may boil down to this: Inflation’s above target, but the data-dependent Banxico is ready to wait, expecting it to slow in line with their forecasts. Bear in mind that the most recent GDP forecasts from Banxico and the Finance Ministry are quite upbeat too.

Bullish on Mexico

Best case forecasts see 2021 GDP growth as fastest in decades

Sources: Banco de Mexico, informes trimestrales; Secretaría de Hacienda y Crédito Público, Communiqué No. 023; Bloomberg.

.chart-js display: none;

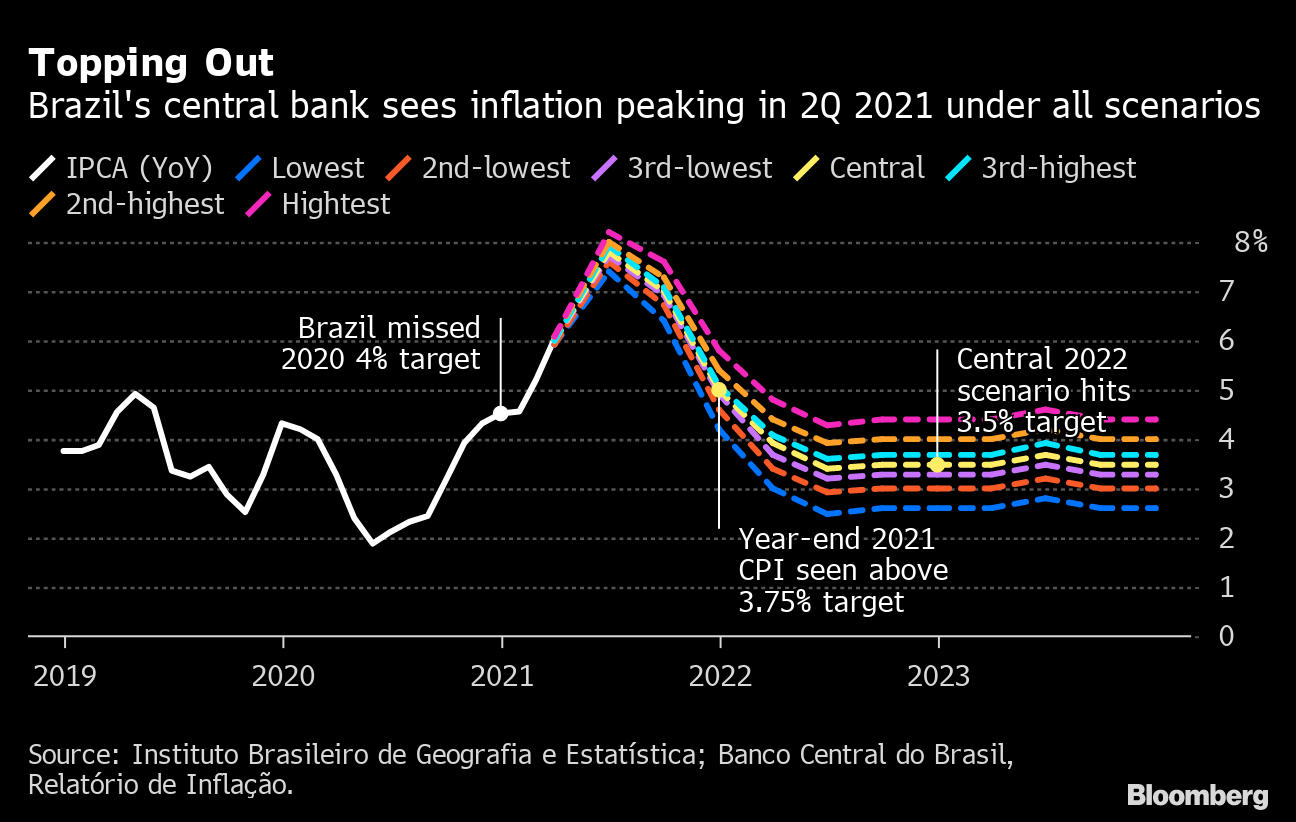

In contrast, gloom pervades the region’s biggest economy. One of the country’s largest hedge fund managers says Brazil may be nearing a “perfect inflationary storm.” Data out Friday may show consumer prices are well over the 5.25% target range ceiling and consistent with the more dire central bank scenarios.

Topping Out

Brazil’s central bank sees inflation peaking in 2Q 2021 under all scenarios

Source: Instituto Brasileiro de Geografia e Estatística; Banco Central do Brasil, Relatório de Inflação.

.chart-js display: none;

Among the Andean nations, inflation in Chile should come in right around 3% whereas analysts see Colombia’s setting a record-low of 1.45%. Rounding out the week, look for Peru’s central bank to keep the key rate at a record-low 0.25% for a 12th straight meeting.

— With assistance by Peggy Collins, Benjamin Harvey, Robert Jameson, Malcolm Scott, and Michael Winfrey