IN HIS NEW book Casey Mulligan offers an intriguing explanation for why President Donald Trump makes outlandish economic claims. Mr Trump knows he is hyberbolising when he says that America has enjoyed “the greatest economy in the history of the world” on his watch, suggests Mr Mulligan, who was until recently the chief economist on the president’s Council of Economic Advisers. It is a “strategy for getting the press to cover a new fact, which is to exaggerate it so that the press might enjoy correcting him and unwittingly disseminate the intended finding”. Journalists’ dislike for Mr Trump, according to Mr Mulligan, blinds them to many of the administration’s genuine economic successes. He may have a point.

Assessing leaders’ economic records is fraught with difficulty. Presidents typically get credit when the economy is doing well and blame when it does badly—but short-term economic outcomes are usually more influenced by central banks, demography and what is happening in the rest of the world, among other factors. Even today, political scientists continue to argue over whether the economy in the 20th century did better under Democratic or Republican administrations. All this is of little use to the American public, whose vote for a president must be based, in part, on a real-time assessment of economic competence.

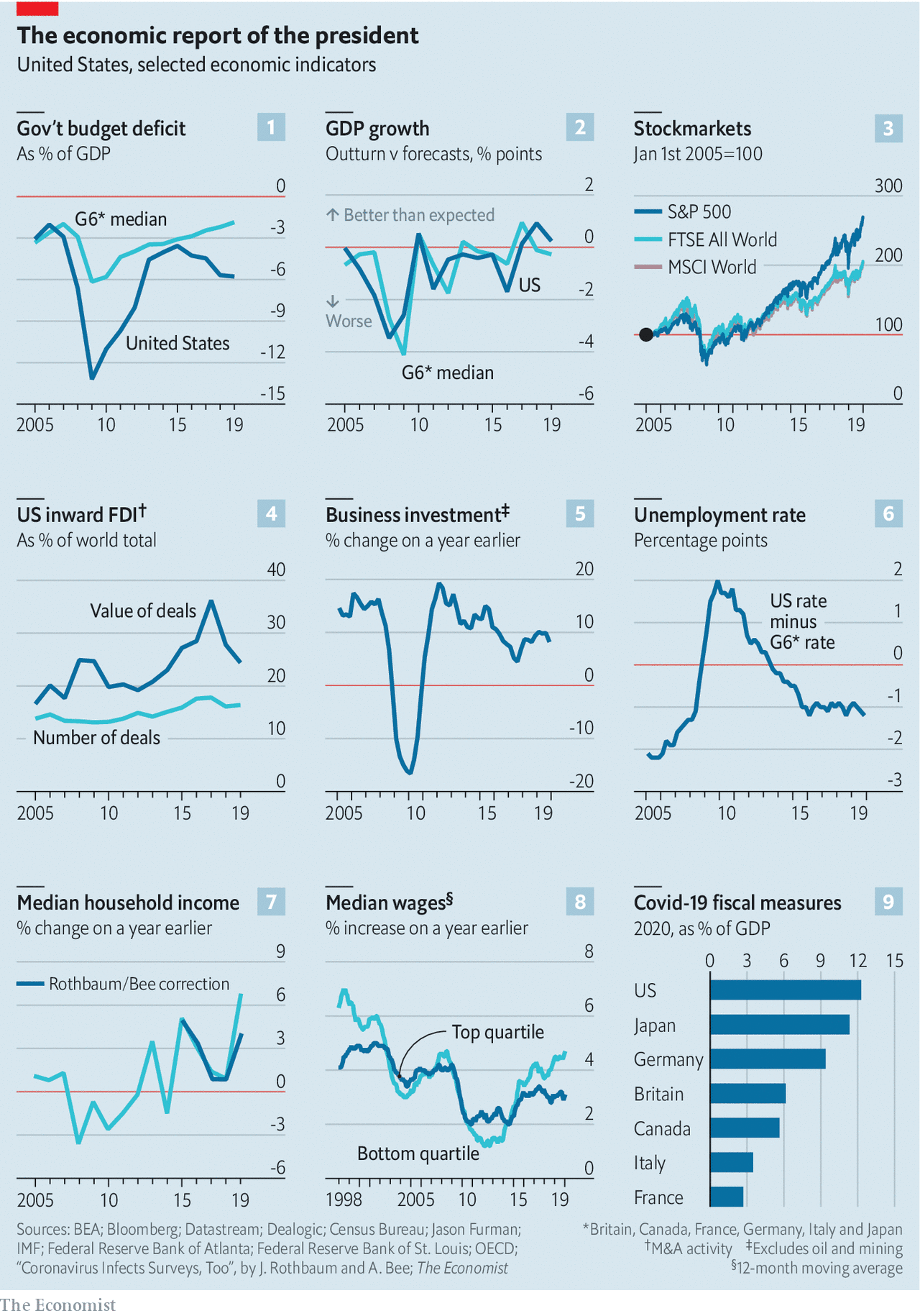

Mr Trump came to power with unrealistic promises to create 25m jobs and supercharge economic growth, and to that end cut taxes and boosted spending, widening the fiscal deficit (see chart 1). Economists will continue to weigh up the specific costs and benefits of those policies. A true evaluation will take some time. At present, however, it is possible to assess whether the American economy overall did better or worse under Mr Trump. That involves comparing actual American economic performance, on the one hand, with what an impartial spectator could reasonably have expected, on the other. To that end The Economist has gathered a range of economic data, from business investment to wage growth, wherever possible comparing American economic performance to that of other rich countries.

The bulk of the analysis covers the period from 2017, when Mr Trump took office, to the end of 2019. We stop in 2019 in part because some data are released only annually, and in part because the pandemic has turned economies across the world upside down. Our conclusion is that, in 2017-19, the American economy performed marginally better than expected. (That conclusion remains if we follow the practice of some political economists, who argue that the influence of presidents on the economy can be discerned only after a year in office, and limit our analysis to 2018-19.)

Take gross domestic product (GDP), a measure of output which is the most common yardstick of economic performance. GDP growth was somewhat faster in 2017-19 than it was in either Barack Obama’s first or second term, according to official data. America also did well relative to other countries. The world economy peaked in 2017. In 2018 it slowed but America accelerated. In 2019 America slowed too, but stayed ahead of others.

Another way to look at this question is to assess whether America in 2017-19 exceeded or fell short of economists’ expectations (see chart 2). In October 2012 the IMF forecast that in the subsequent four years (those of Mr Obama’s second term), the American economy would grow by an annual average of 3%. In fact that proved to be too optimistic; it actually grew by closer to 2% a year. But the IMF was too pessimistic in its projections for 2017-19, released shortly before the election of 2016. In those years America outperformed the forecasts.

But if the American economy did better than expected in some respects, it disappointed in others. Take the corporate sector, which Mr Trump helped with lighter taxes. Corporation-tax cuts did increase post-tax earnings, one reason why the American stockmarket has done relatively well since Mr Trump came to power (see chart 3). America has also become a more favoured destination for foreign direct investment (see chart 4). But there is little evidence of the promised business-investment boom (see chart 5).

America’s labour-market performance is similarly nuanced. Though Mr Trump particularly likes to boast about monthly employment figures, it is hard to make the case that in 2017-19 the jobs machine was whirring. Jobs growth was slower than it had been during Mr Obama’s second term. In 2009-16 America’s unemployment rate fell relative to the average for other G7 economies (see chart 6). Under Mr Trump unemployment did fall to the lowest since the 1960s, but this was not internationally exceptional. America’s improvement relative to employment in other countries stopped under Mr Trump.

The lot of working-class Americans, however, definitely improved in 2017-19. Comparing household incomes between countries is difficult, certainly for recent years. But though there is some dispute about the reliability of the data for 2019, where the pandemic made it difficult for researchers to conduct surveys, there is clear evidence of an acceleration in the growth of America’s median household income from 2017 onwards (see chart 7). A tight labour market also helped raise the wage growth of the lowest-paid Americans, relative to others, to a degree not seen since Bill Clinton was president (see chart 8).

And what of the economy in 2020? Mr Trump’s loose fiscal policy before the pandemic left America with much higher debt going into the crisis. On top of that splurge, this year America has implemented the world’s largest fiscal package (see chart 9), posting stimulus cheques worth up to $1,200 per person and temporarily bumping up unemployment-insurance payments by $600 a week. It is possible, though unlikely, that Congress will pass even more stimulus before the election. Even without another package, however, and even though it is enduring a deep recession, America will probably be the best-performing G7 economy in 2020—perhaps by some margin. Just before the pandemic, the American economy looked slightly stronger than other rich countries. Before long, the gap may be more impressive.

OTTAWA – Canada’s unemployment rate held steady at 6.5 per cent last month as hiring remained weak across the economy.

Statistics Canada’s labour force survey on Friday said employment rose by a modest 15,000 jobs in October.

Business, building and support services saw the largest gain in employment.

Meanwhile, finance, insurance, real estate, rental and leasing experienced the largest decline.

Many economists see weakness in the job market continuing in the short term, before the Bank of Canada’s interest rate cuts spark a rebound in economic growth next year.

Despite ongoing softness in the labour market, however, strong wage growth has raged on in Canada. Average hourly wages in October grew 4.9 per cent from a year ago, reaching $35.76.

Friday’s report also shed some light on the financial health of households.

According to the agency, 28.8 per cent of Canadians aged 15 or older were living in a household that had difficulty meeting financial needs – like food and housing – in the previous four weeks.

That was down from 33.1 per cent in October 2023 and 35.5 per cent in October 2022, but still above the 20.4 per cent figure recorded in October 2020.

People living in a rented home were more likely to report difficulty meeting financial needs, with nearly four in 10 reporting that was the case.

That compares with just under a quarter of those living in an owned home by a household member.

Immigrants were also more likely to report facing financial strain last month, with about four out of 10 immigrants who landed in the last year doing so.

That compares with about three in 10 more established immigrants and one in four of people born in Canada.

This report by The Canadian Press was first published Nov. 8, 2024.

The Canadian Institute for Health Information says health-care spending in Canada is projected to reach a new high in 2024.

The annual report released Thursday says total health spending is expected to hit $372 billion, or $9,054 per Canadian.

CIHI’s national analysis predicts expenditures will rise by 5.7 per cent in 2024, compared to 4.5 per cent in 2023 and 1.7 per cent in 2022.

This year’s health spending is estimated to represent 12.4 per cent of Canada’s gross domestic product. Excluding two years of the pandemic, it would be the highest ratio in the country’s history.

While it’s not unusual for health expenditures to outpace economic growth, the report says this could be the case for the next several years due to Canada’s growing population and its aging demographic.

Canada’s per capita spending on health care in 2022 was among the highest in the world, but still less than countries such as the United States and Sweden.

The report notes that the Canadian dental and pharmacare plans could push health-care spending even further as more people who previously couldn’t afford these services start using them.

This report by The Canadian Press was first published Nov. 7, 2024.

Canadian Press health coverage receives support through a partnership with the Canadian Medical Association. CP is solely responsible for this content.

As Canadians wake up to news that Donald Trump will return to the White House, the president-elect’s protectionist stance is casting a spotlight on what effect his second term will have on Canada-U.S. economic ties.

Some Canadian business leaders have expressed worry over Trump’s promise to introduce a universal 10 per cent tariff on all American imports.

A Canadian Chamber of Commerce report released last month suggested those tariffs would shrink the Canadian economy, resulting in around $30 billion per year in economic costs.

More than 77 per cent of Canadian exports go to the U.S.

Canada’s manufacturing sector faces the biggest risk should Trump push forward on imposing broad tariffs, said Canadian Manufacturers and Exporters president and CEO Dennis Darby. He said the sector is the “most trade-exposed” within Canada.

“It’s in the U.S.’s best interest, it’s in our best interest, but most importantly for consumers across North America, that we’re able to trade goods, materials, ingredients, as we have under the trade agreements,” Darby said in an interview.

“It’s a more complex or complicated outcome than it would have been with the Democrats, but we’ve had to deal with this before and we’re going to do our best to deal with it again.”

American economists have also warned Trump’s plan could cause inflation and possibly a recession, which could have ripple effects in Canada.

It’s consumers who will ultimately feel the burden of any inflationary effect caused by broad tariffs, said Darby.

“A tariff tends to raise costs, and it ultimately raises prices, so that’s something that we have to be prepared for,” he said.

“It could tilt production mandates. A tariff makes goods more expensive, but on the same token, it also will make inputs for the U.S. more expensive.”

A report last month by TD economist Marc Ercolao said research shows a full-scale implementation of Trump’s tariff plan could lead to a near-five per cent reduction in Canadian export volumes to the U.S. by early-2027, relative to current baseline forecasts.

Retaliation by Canada would also increase costs for domestic producers, and push import volumes lower in the process.

“Slowing import activity mitigates some of the negative net trade impact on total GDP enough to avoid a technical recession, but still produces a period of extended stagnation through 2025 and 2026,” Ercolao said.

Since the Canada-United States-Mexico Agreement came into effect in 2020, trade between Canada and the U.S. has surged by 46 per cent, according to the Toronto Region Board of Trade.

With that deal is up for review in 2026, Canadian Chamber of Commerce president and CEO Candace Laing said the Canadian government “must collaborate effectively with the Trump administration to preserve and strengthen our bilateral economic partnership.”

“With an impressive $3.6 billion in daily trade, Canada and the United States are each other’s closest international partners. The secure and efficient flow of goods and people across our border … remains essential for the economies of both countries,” she said in a statement.

“By resisting tariffs and trade barriers that will only raise prices and hurt consumers in both countries, Canada and the United States can strengthen resilient cross-border supply chains that enhance our shared economic security.”

This report by The Canadian Press was first published Nov. 6, 2024.