A new analysis by realtor firm Re/Max says the Toronto real estate market may be better positioned than previously thought to weather the financial downturn expected this year, though there still may be some choppy waters ahead.

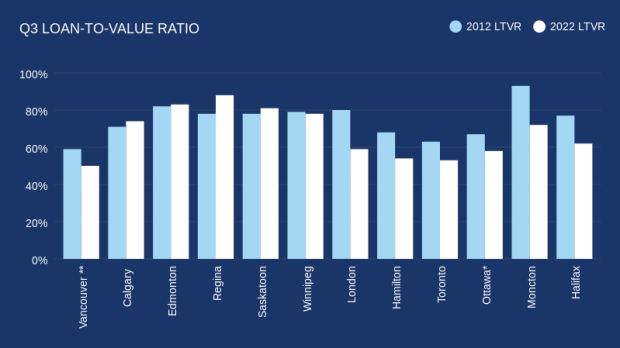

The new report compared average price and new mortgage values in different markets across the country between the third quarter of 2012 and the third quarter of 2022.

Loan to value ratios are used to express how much debt a person holds on an asset compared to its value. The higher the percentage, the greater the debt level on the asset.

Back in the third quarter of 2012, the average Toronto home price was $483,900, while the average new mortgage amount was $305,776, yielding a loan-to-value ratio of about 63 per cent.

In the third quarter of last year, the average Toronto home price was 1,079,957 while the average amount for a new mortgage was $567,441, yielding a loan-to-value ratio of about 53 per cent.

So what explains the fact that homebuyers in Toronto are putting down more money even as prices have skyrocketed over the last number of years?

Rising prices, Re/Max Canada President Christopher Alexander told CP24, are in fact part of the answer.

“Some people have generated a lot of equity over the years,” he said, alluding to people who have made hundreds of thousands of dollars from properties as the housing market took off.

A few other factors have also contributed to people having more money to put toward a home, the report says, including large profits realized in the stock market over a lengthy bull run.

“You’ve had the remote work phenomenon, people are allowed to keep their jobs and move to more affordable markets,” Alexander said.

“And the big, big story is the transition of generational wealth that’s been going on. The ‘bank of mom and dad,’ as we like to call it in the industry, has played a huge role in supporting — whether they’re first time homebuyers or move-up buyers — into purchasing homes at much higher down payment rates with chunks so that they can manage payments a lot easier.”

But while people in the Toronto area may be putting down a higher percentage of a home’s value than they were 10 years ago, there is no getting around the fact that the loans are nevertheless much larger than they were a decade ago — nearly double the size on average.

The report notes that given the steady climb in interest rates last year, “banks are tightening their own lending practices and proceeding with caution when qualifying today’s borrowers.”

The report says some bank appraisals are coming in lower than values paid in recent months, “sending buyers scrambling to make up the difference.”

“With overnight rates poised to climb on at least two more occasions the first half of 2023, market stability will undoubtedly be tested, but the latter half of the year is forecast to improve as homebuyers and sellers continue to acclimatize to new market realities.”

Limited supply of housing and a steady flow of new immigrants to the GTA are expected to buoy the housing market in the next year, the report says.

Alexander said that supply remains “shockingly low” and that some potential sellers may be holding back now because they perceive that they won’t get top dollar for their properties.

“I think the majority of sellers are hoping to get the most for their money just like buyers want to pay the least,” he said. “So you have a lot of them that don’t need to move, just wait. And right now what you’re really seeing is situational transactions. People that have kids, or have gotten married, divorced — the ones that really need to make a move are the ones you’re seeing bringing product to the market right now.”

He said potential job losses triggered by an economic downturn could also send more homes to market if people can no longer afford their payments.

The report noted that mortgage delinquency rates remain low in Canada.

“While challenges certainly exist in today’s high interest rate environment, risk factors for the overall housing market are greatly reduced when homeowners own a larger proportion of their homes,” Alexander said in a statement with the report. “With half of loan-to-value ratios within the 50- and 60-per cent range in Canadian markets, homeowners are better able to withstand downward pressure on housing values and fewer will find themselves underwater, carrying upside down loans.”

TORONTO – One expert predicts Ottawa‘s changes to mortgage rules will help spur demand among potential homebuyers but says policies aimed at driving new supply are needed to address the “core issues” facing the market.

The federal government’s changes, set to come into force mid-December, include a higher price cap for insured mortgages to allow more people to qualify for a mortgage with less than a 20 per cent down payment.

The government will also expand its 30-year mortgage amortization to include first-time homebuyers buying any type of home, as well as anybody buying a newly built home.

CIBC Capital Markets deputy chief economist Benjamin Tal calls it a “significant” move likely to accelerate the recovery of the housing market, a process already underway as interest rates have begun to fall.

However, he says in a note that policymakers should aim to “prevent that from becoming too much of a good thing” through policies geared toward the supply side.

Tal says the main issue is the lack of supply available to respond to Canada’s rapidly increasing population, particularly in major cities.

This report by The Canadian Press was first published Sept. 17,2024.

OTTAWA – The Canadian Real Estate Association says the number of homes sold in August fell compared with a year ago as the market remained largely stuck in a holding pattern despite borrowing costs beginning to come down.

The association says the number of homes sold in August fell 2.1 per cent compared with the same month last year.

On a seasonally adjusted month-over-month basis, national home sales edged up 1.3 per cent from July.

CREA senior economist Shaun Cathcart says that with forecasts of lower interest rates throughout the rest of this year and into 2025, “it makes sense that prospective buyers might continue to hold off for improved affordability, especially since prices are still well behaved in most of the country.”

The national average sale price for August amounted to $649,100, a 0.1 per cent increase compared with a year earlier.

The number of newly listed properties was up 1.1 per cent month-over-month.

This report by The Canadian Press was first published Sept. 16, 2024.

MONTREAL – Two Quebec real estate brokers are facing fines and years-long suspensions for submitting bogus offers on homes to drive up prices during the COVID-19 pandemic.

Christine Girouard has been suspended for 14 years and her business partner, Jonathan Dauphinais-Fortin, has been suspended for nine years after Quebec’s authority of real estate brokerage found they used fake bids to get buyers to raise their offers.

Girouard is a well-known broker who previously starred on a Quebec reality show that follows top real estate agents in the province.

She is facing a fine of $50,000, while Dauphinais-Fortin has been fined $10,000.

The two brokers were suspended in May 2023 after La Presse published an article about their practices.

One buyer ended up paying $40,000 more than his initial offer in 2022 after Girouard and Dauphinais-Fortin concocted a second bid on the house he wanted to buy.

This report by The Canadian Press was first published Sept. 11, 2024.