KIEV, UKRAINE – 2020/09/03: A man wearing a face mask with US dollar print as a preventive measure … [+] walk on the street. In Ukraine, 54 people have died from complications caused by coronavirus per day, which is the largest number of deaths from coronavirus since the beginning of the pandemic in the country, reportedly by media. (Photo by Pavlo Gonchar/SOPA Images/LightRocket via Getty Images)

SOPA Images/LightRocket via Getty Images

It has now become clear, and mainstream, that the economy weakened significantly in November, and that such weakness will carry forward to year’s end, at a minimum. The weakness occurred primarily in the services sector as the virus’ resurgence caused some governors to mandate new or additional service business restrictions.

As a result, jobless claims have spiked, travel and hotel occupancy fell to even lower levels, and restaurant and other retail activity faded.

Yet, despite the economic weakness, and the inability of the Congress to craft a new stimulus package, inflation expectations are on the rise.

The Data

Jobless claims spiked +229K the week ended December 5th;

Open Table data show a falloff of -58.1% Y/Y in restaurant reservations (12/4/20);

TSA checkpoint data was off -71.0% in the three days ended December 10th (Tuesday to Thursday). For the same weekdays ended November 12th, that number was -67.5%; back in September (9/15-9/17), that was -64.5%. So, it appears that travel has been cut back;

Recent hotel data also show additional weakness in occupancy rates.

In addition, as of this writing, the Congress has been unable to produce a second stimulus package. The unemployment insurance programs of the CARES Act (Pandemic Unemployment Assistance and its emergency provisions (PUA and PUEA), all abruptly end on 12/31. This will impact more than 13 million recipients. The drop-off in assistance comes at a time when newly imposed business restrictions have intensified due the virus’ resurgence.

Then we have the continuing political drama over vote counting. On Friday, December 11th, the U.S. Supreme Court refused to hear Texas’ case regarding irregularities of vote counts in certain states, causing the Texas GOP to threaten what I will call “T-exit” (i.e., similar to “Brexit” which, by the way, is still impacting markets due to the inability to finally agree on how relations between Britain and the Continent will work). By the time you read this, Mr. Biden will “officially” be President-Elect as the Electoral College is scheduled to vote on Monday, December 14. He is going to have one heck of a job trying to “heal” the existing political scars, if, indeed, he even tries.

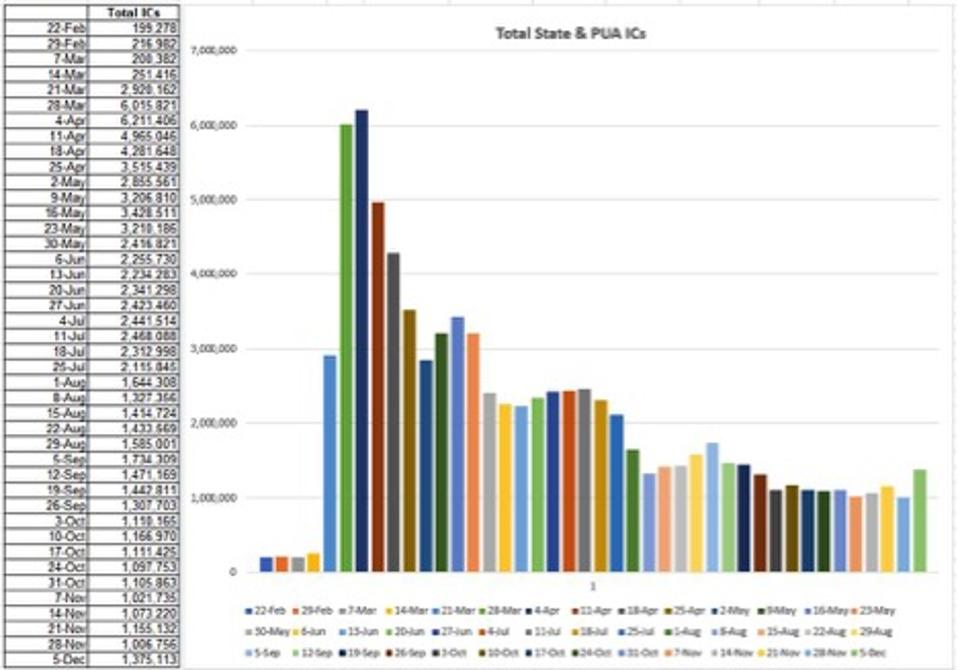

As always, basic economic trends are best seen through the lens of the labor market. Initial Unemployment Claims (ICs) in the state unemployment programs spiked in the first week of December. Using non-seasonally adjusted data, they spiked 229K, the largest uptick since the pandemic began in March! PUA claims also spiked by 139K, so together, the spike exceeded +368K. To put this in perspective, total new weekly unemployment claims have been higher than one million every week since March! The week ended December 5th saw 1.375 new claims (layoffs!), a significant rise from the awful 1.006 million the last week of November. Look at the right-hand side of the chart – no progress since early August!

Total State & PUA ICs

Universal Value Advisors

Resurgence of Inflation Expectations

The virus isn’t the only phenomenon experiencing resurgence. Inflation is too! And we see it in the Treasury yield curve. There are two theoretical parts to interest rates; the “real” rate, and the “inflation premium.”

The U.S. Treasury yield curve is the international standard which serves as a reference point when examining yields elsewhere, as it is considered “risk free” as far as the return of one’s principal. Nevertheless, despite the U.S. Treasury curve as the standard bearer, we see that in today’s world, because of the money printing policies of the Bank of Japan (BOJ) and European Central Bank (ECB), nearly one-third of fixed income assets, globally, have negative yields. Yes, you pay them to invest your money in their bonds! These negative yielders include junk credit rated Greek 2-year notes, Italian 5-year notes, and Portuguese 10-years. Indeed, if the latest U.S. CPI (-1.2% Y/Y) is any indication of U.S. inflation, then “real” rates (i.e., inflation adjusted) along most of the U.S. Treasury yield curve, are also negative.

In early August, the nominal yield on 10-year U.S. Treasury Notes hit a low of 0.52% (i.e. 52 basis points – abbreviated 52bps). In early November, as inflation expectations were awakened, that rate nearly doubled to 98 bps, and it was as high as 94bps on December 7th. The rise in this rate is attributable to market expectations that all the stimulus and money printing being contemplated will result in rising inflation. (And, no doubt, it eventually will!)

It does seem contradictory that rates are rising at the same time the economy is weakening! But, that’s exactly what we have. And it is based on the perception that the Congress can and will enact new stimulus, if not immediately, then soon after Mr. Biden takes office. In addition, there is a relatively new economic notion called “Modern Monetary Theory” (MMT) that postulates that a sovereign nation can print as much money as it desires, the only barrier being the nation’s inflation tolerance. And, if there is no “inflation,” then no harm, no foul. (In the case of the U.S., this isn’t exactly correct, as the country benefits greatly from the dollar’s status as the world’s reserve currency. We already see the dollar’s value weakening, and excessive money printing will have a huge impact there – but, I digress; this is a topic for another blog.) Of course, today’s politicians have happily glommed onto this “Theory,” as they will no longer have to defend deficit spending.

There are two other circumstances influencing the markets’ future inflation perceptions:

When the pandemic first hit in Q1/Q2 2020, prices initially fell. As the economy began to recover (Q3), they snapped back. But when we get to Q1/Q2 2021, comparisons will be to the lower prices of a year earlier and this will show up as a higher level of inflation;

If the vaccines are successfully deployed, there will be an initial shot in the arm (pun intended) for the economy, as there is a high level of pent-up demand in the population from being shut-in for such a long period of time. So, expect a period of high consumption, especially of services that the public has gone without for so long. We will likely see (temporary) price hikes along the way.

Both will contribute to what will appear to be “higher prices.” And the CPI and other such indexes will move higher as a result. Interest rates and yield curves will likely follow.

Treasury Yield Volatility

In November, Treasury Secretary Mnuchin told a very disappointed Fed Chair Powell that the Fed’s special credit line from the Treasury and its authority to lend to the corporate sector would be shutdown at year’s end. Markets, however, have a very high level of confidence that those or similar programs will be reinstated by incoming Treasury Secretary Yellen. So, we have a unique phenomenon – the yields on Treasury paper, reflecting market inflation fears, appear to have become more volatile than the yields on corporate debt which have enjoyed Fed support well down the quality spectrum. Since August, Treasury yields have drifted upward. At the same time, corporate spreads on much lower quality paper, compressed. I expect that Yellen will reinstate the Fed’s corporate lending line, the Fed will continue to support junk/near junk corporate paper, and that this unusual volatility phenomenon will continue.

Conclusions

The lack of a stimulus package in the “lame duck” session of Congress has caused the Treasury yield curve to move a few basis points lower since the election. But, even as the economy weakens, near-term, don’t expect a test of that 52bps 10-year T-Note low. Upward pressure on the Treasury yield curve has now appeared, especially given the likely deficits in a Biden Administration and the adoption of MMT as a convenient excuse. At the same time, the protection of a large swath of corporate America by the Fed and the expected continuation of that policy under the incoming Administration will keep corporate spreads to Treasuries at record lows. The continuation of the unique phenomenon of higher volatility in Treasury yields than in the corporate world is likely.

FREDERICTON – New Brunswick‘s finance minister says the province recorded a surplus of $500.8 million for the fiscal year that ended in March.

Ernie Steeves says the amount — more than 10 times higher than the province’s original $40.3-million budget projection for the 2023-24 fiscal year — was largely the result of a strong economy and population growth.

The report of a big surplus comes as the province prepares for an election campaign, which will officially start on Thursday and end with a vote on Oct. 21.

Steeves says growth of the surplus was fed by revenue from the Harmonized Sales Tax and federal money, especially for health-care funding.

Progressive Conservative Premier Blaine Higgs has promised to reduce the HST by two percentage points to 13 per cent if the party is elected to govern next month.

Meanwhile, the province’s net debt, according to the audited consolidated financial statements, has dropped from $12.3 billion in 2022-23 to $11.8 billion in the most recent fiscal year.

Liberal critic René Legacy says having a stronger balance sheet does not eliminate issues in health care, housing and education.

This report by The Canadian Press was first published Sept. 16, 2024.

OTTAWA – Finance Minister Chrystia Freeland says the government is making some changes to mortgage rules to help more Canadians to purchase their first home.

She says the changes will come into force in December and better reflect the housing market.

The price cap for insured mortgages will be boosted for the first time since 2012, moving to $1.5 million from $1 million, to allow more people to qualify for a mortgage with less than a 20 per cent down payment.

The government will also expand its 30-year mortgage amortization to include first-time homebuyers buying any type of home, as well as anybody buying a newly built home.

On Aug. 1 eligibility for the 30-year amortization was changed to include first-time buyers purchasing a newly-built home.

Justice Minister Arif Virani is also releasing drafts for a bill of rights for renters as well as one for homebuyers, both of which the government promised five months ago.

Virani says the government intends to work with provinces to prevent practices like renovictions, where landowners evict tenants and make minimal renovations and then seek higher rents.

The government touts today’s announced measures as the “boldest mortgage reforms in decades,” and it comes after a year of criticism over high housing costs.

The Liberals have been slumping in the polls for months, including among younger adults who say not being able to afford a house is one of their key concerns.

This report by The Canadian Press was first published Sept. 16, 2024.

OTTAWA – Statistics Canada says manufacturing sales rose 1.4 per cent to $71 billion in July, helped by higher sales in the petroleum and coal and chemical product subsectors.

The increase followed a 1.7 per cent decrease in June.

The agency says sales in the petroleum and coal product subsector gained 6.7 per cent to total $8.6 billion in July as most refineries sold more, helped by higher prices and demand.

Chemical product sales rose 5.3 per cent to $5.6 billion in July, boosted by increased sales of pharmaceutical and medicine products.

Sales of wood products fell 4.8 per cent for the month to $2.9 billion, the lowest level since May 2023.

In constant dollar terms, overall manufacturing sales rose 0.9 per cent in July.

This report by The Canadian Press was first published Sept. 16, 2024.