Legendary fund manager Li Lu (who Charlie Munger backed) once said, ‘The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital. When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that Innovatec S.p.A. (BIT:INC) does use debt in its business. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can’t easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can’t fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

View our latest analysis for Innovatec

What Is Innovatec’s Net Debt?

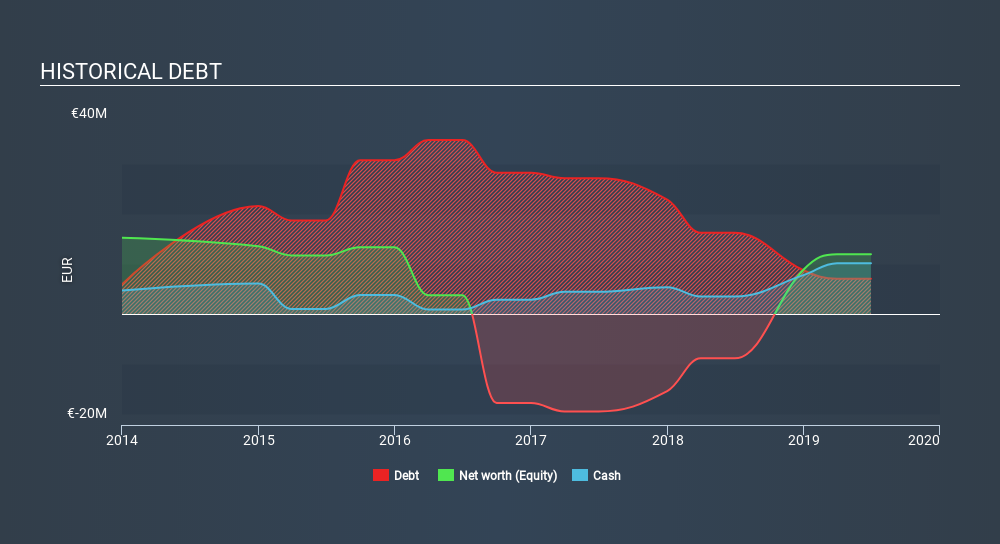

As you can see below, Innovatec had €7.07m of debt at June 2019, down from €16.2m a year prior. However, it does have €10.2m in cash offsetting this, leading to net cash of €3.11m.

How Healthy Is Innovatec’s Balance Sheet?

According to the last reported balance sheet, Innovatec had liabilities of €21.6m due within 12 months, and liabilities of €15.1m due beyond 12 months. On the other hand, it had cash of €10.2m and €19.2m worth of receivables due within a year. So it has liabilities totalling €7.27m more than its cash and near-term receivables, combined.

Since publicly traded Innovatec shares are worth a total of €47.2m, it seems unlikely that this level of liabilities would be a major threat. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward. While it does have liabilities worth noting, Innovatec also has more cash than debt, so we’re pretty confident it can manage its debt safely.

Although Innovatec made a loss at the EBIT level, last year, it was also good to see that it generated €14m in EBIT over the last twelve months. The balance sheet is clearly the area to focus on when you are analysing debt. But it is Innovatec’s earnings that will influence how the balance sheet holds up in the future. So when considering debt, it’s definitely worth looking at the earnings trend. Click here for an interactive snapshot.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. Innovatec may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. Over the last year, Innovatec actually produced more free cash flow than EBIT. That sort of strong cash generation warms our hearts like a puppy in a bumblebee suit.

Summing up

Although Innovatec’s balance sheet isn’t particularly strong, due to the total liabilities, it is clearly positive to see that it has net cash of €3.11m. The cherry on top was that in converted 116% of that EBIT to free cash flow, bringing in €16m. So we don’t have any problem with Innovatec’s use of debt. There’s no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet – far from it. For instance, we’ve identified 4 warning signs for Innovatec that you should be aware of.

If, after all that, you’re more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

If you spot an error that warrants correction, please contact the editor at [email protected]. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

The easiest way to discover new investment ideas

Save hours of research when discovering your next investment with Simply Wall St. Looking for companies potentially undervalued based on their future cash flows? Or maybe you’re looking for sustainable dividend payers or high growth potential stocks. Customise your search to easily find new investment opportunities that match your investment goals. And the best thing about it? It’s FREE. Click here to learn more.