The outlook for real growth in living standards in the coming months, years and decades is bleak

Article content

Yet another alarming inflation number from Statistics Canada — 7.7 per cent from May to May — has underlined that something is seriously wrong with Canada’s economy. Prices are rising fast because spending is rising fast while production is not. The capacity of our economy to produce is flatlining because business investment has been so weak that the stock of productive capital per worker is falling. If we do not turn that around, the outlook for real growth in living standards in the coming months, years and decades is bleak.

Advertisement 2

Article content

The basic problem is chronically low business investment, which has been the highlight — or lowlight — of Statistics Canada’s quarterly GDP reports for several years now. The cumulative effect of low rates of investment shows up in the national balance sheet accounts, which tally not flows but stocks: the assets and liabilities of households, businesses and governments. The balance sheet accounts make fewer headlines than the inflation and GDP reports, which is a shame because they tell us a lot about our economic prospects. Lately, they have been telling us that, thanks to business investment that is not even keeping up with depreciation, Canada’s net stock of capital is stagnating.

Economic growth has three main drivers: growth in the work force, growth in the capital stock, and growth of productivity. Growth in the capital stock and growth in productivity tend to run together. When businesses invest in new buildings, engineering structures, machinery and equipment, and intellectual property such as software, workers get better tools to work with, which enables them to produce more output and earnings per hour of work. The data show that our work force is still growing, though not as quickly as in previous decades. But our stock of non-residential structures, machinery, software and other tools per worker is shrinking.

Advertisement 3

Article content

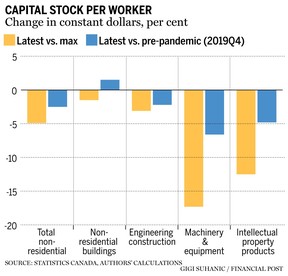

Compared to before the pandemic the real stock of business capital per worker is down three per cent (see nearby figure). The only type of business capital that has grown faster than the work force since the fourth quarter of 2019 is non-residential buildings. Capital per worker in the other major categories is down: engineering construction by two per cent, machinery and equipment by seven per cent, and intellectual property products — the category of investment that people thought COVID would spur, to the extent even of possibly triggering a new period of prosperity — by five per cent.

Extend the comparison further back and the numbers are downright alarming. Canada’s stock of business capital per worker was declining even before the pandemic. Total business capital per worker peaked in the fourth quarter of 2015. Since then, it is down five per cent. Each type of capital is also down per worker from its own peak around that time: non-residential buildings by one per cent, engineering construction per worker by three per cent, intellectual property products by 12 per cent and machinery and equipment by 17 per cent.

Advertisement 4

Article content

These numbers normally rise over time. Such a multi-year decline in the tools available to the average member of Canada’s workforce is very likely unprecedented. The only historical period where consistent data (if it existed) might show something similar is the depression of the 1930s. From the perspective of Canadian workers, our economy is decapitalizing.

-

Jack Mintz: Why all the job vacancies?

-

Opinion: Vladimir Putin’s $10-trillion war

-

Opinion: Debt-to-GDP is an anchor not a guide

One more release from Statistics Canada that should have made headlines but mainly didn’t was June’s report that labour productivity fell 0.5 per cent in the first quarter of this year — its seventh consecutive decline. No wonder growth in production is lagging growth in spending.

Advertisement 5

Article content

The 2022 federal budget did note the dire implications of low business investment, citing projections that growth in living standards in Canada would rank dead last among OECD countries over the next 40 years. If anything, however, federal initiatives since then — higher taxes on politically vulnerable businesses and products, lower limits on deductibility of interest on business loans and confidence-sapping proposals for new regulation related to greenhouse gases, plastics and competition policy — will further discourage investment. Higher investment and robust economic growth seem to be low priorities in Ottawa these days.

We need changes in both tone and policy. Without them, the ominous decapitalization of Canada’s economy seems set to continue. Canadian workers need more capital — better tools — to raise their productivity and earnings. Otherwise, both the current expansion and our long-term living standards are in trouble.

Mawakina Bafale is a research assistant at the C. D. Howe Institute, where William Robson is CEO.