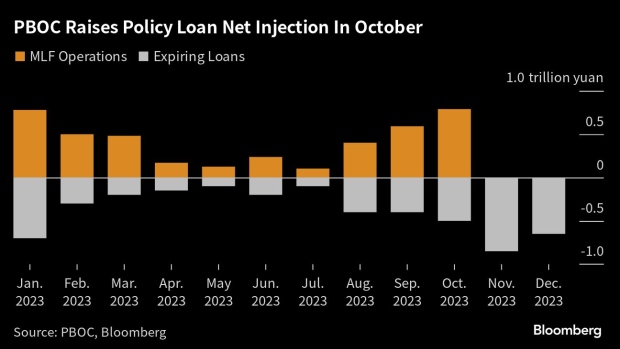

(Bloomberg) — China’s central bank is making the biggest medium-term liquidity injection since 2020, stepping up efforts to support the nation’s economic recovery and debt sales.

The People’s Bank of China added a net 289 billion yuan ($39.6 billion) into the financial system via a one-year policy loan on Monday, the most since Dec. 2020. At the same time, it drained a net 134 billion yuan of short-term liquidity through open-market operations.

The nation is tussling with a stuttering economy, with consumer prices reflecting weak demand while data released last week showed the amount of loans made missed expectations. Beijing as well as local governments are ramping up debt sales to finance stimulus spending, reinforcing the need for more liquidity in the financial system.

“The additional liquidity injection aims to maintain stable interbank liquidity conditions amid rising LGB debt swap bond issuance, as well as stronger liquidity demand during tax payment times,” said Becky Liu, head of China macro strategy at Standard Chartered Bank, referring to local government bonds. “It also reflects stronger liquidity demand by commercial banks.”

The PBOC kept the MLF interest rate unchanged at 2.5%, in line with expectations. Yields from two-year to 10-year sovereign bonds rose by one to three basis points on Monday.

The move comes as Beijing considers a new round of stimulus to help the economy meet the official annual growth target of around 5%. The Ministry of Finance sold 1.2 trillion yuan of central government bonds in September, 60% higher than the average for the same period in the past three years, Bloomberg-compiled data show.

More supply is arriving, including a 1 trillion yuan program to help regional governments refinance hidden debts — a risk that Beijing is keen to reduce. Policymakers are also weighing additional sovereign bond sales of at least 1 trillion yuan for spending on infrastructure, Bloomberg News reported earlier.

Liu said the PBOC may cut the one-year MLF rate before year end, and recommended buying cash bonds on the expectations that “China rates remain a lower-for-longer story on the back of likely continued sub-par growth during the current period of economic transition.”

Uneven Recovery

Official data on Friday showed a surprise flatlining of the consumer inflation rate last month, though other recent indicators such as exports have suggested the slowdown may be moderating. Authorities have rolled out piecemeal measures to buttress the economy but refrained from big stimulus.

China’s monetary policy will make better use of both aggregate and structural tools, central bank chief Pan Gongsheng said in a statement on Saturday, referring to broad moves that affect overall liquidity and targeted ones to aid certain industries. It will seek more sustainable growth while maintaining a “reasonable” expansion pace, he said.

Though markets are still cautious about the precarious economic recovery, financial institutions ranging from Citigroup Inc. to JPMorgan Chase & Co. have upgraded growth targets earlier this month after some improvement in indicators including manufacturing activity.

The cash injection should “offset the demand from government bond supply this week,” said Zhaopeng Xing, senior China strategist at Australia & New Zealand Banking Group Ltd. “The tight liquidity may ease in the second half of October, as the authorities mandated local governments to spend all money raised by bonds before the end of October.”

–With assistance from Wenjin Lv.

(Adds comment in the fourth paragraph)