Brace for it: after a long bull run, the Canadian housing market is correcting.

The list goes on. Fifth, in the low-interest period, more buyers opted for variable-rate mortgages, and they have faced instant resets with the sharp rise in interest rates this year. Changes in housing market conditions — especially selling prices — are like a nasty double-whammy for recent homebuyers. The list could be longer, but here’s one more: housing is a key leading indicator of economic activity. Where it goes, the rest of the economy usually follows. Recent homebuyers won’t be the only ones to get jolted; they are just the first to feel it.

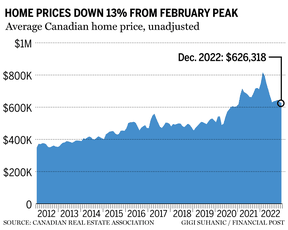

Numbers released on Jan. 16 by the Canadian Real Estate Association (CREA) are sobering. Sales of existing dwellings fell 21 per cent in the second quarter of this year, then 14 per cent in the third and a further five per cent in the fourth to bring the year as a whole down by 38 per cent. True, this comes after an extraordinary surge in 2020-21, but sales levels are currently 16 per cent below the three-year pre-pandemic average. Through another lens, current sales have only been this far below the 10-year average twice since 2007, and the wedge is currently comparable to what we experienced in the 2009 recession.

New homebuilding activity seems to strongly disagree. In contrast to the United States market, housing starts in Canada are on a tear. Temporary factors might be the reason. Last year there was a highly unusual surge of non-permanent residents, a large portion of which were composed of Ukrainian immigrants fleeing war. This is expected to continue boosting building activity into 2023, as over 135,000 arrivals from Ukraine by land and air occurred in 2022, while at latest count, approved applications number over 470,000.

The conflict between the existing and new home markets, typically perfect substitutes, is a puzzle. However, the solution might simply come down to timing. Builders are under intense pressure to run hard while the market is red hot. But it takes time to buy land, zone it, clear it, service it, promote it, and then get on with the building. If you want a house now, it’s likely easier to buy an existing one — suggesting this latter market is a better indication of true, immediate market conditions.

If misery loves company, we’re almost flat out of luck. While interest rates are rising just about everywhere, housing markets aren’t reacting the same as Canada’s. Of the 14 countries covered in an Oxford Economics study late last year, Canada’s housing price correction is the largest, with only Sweden and New Zealand coming anywhere close. Their peak-to-trough forecast has Canada falling 30 per cent, New Zealand down 28 per cent, Sweden declining 20 per cent and Australia and the U.K. each shedding 11 per cent. All the rest are in the single digits, averaging a relatively mild four per cent correction. We are clearly the outlier at the bad end of the distribution.

If housing is still a reliable bellwether of the broader economy — and there’s no good reason to believe it isn’t — then alarming weakness at the leading edge of this prescient market spells trouble ahead. I earnestly hope that those who are confidently predicting a mild correction are right. I fear we are in for something much worse.

Peter Hall is chief executive of Econosphere Inc., and the former chief economist at Export Development Canada.