Brace for it: after a long bull run, the Canadian housing market is correcting.

Economy

Housing’s hard stop spells trouble ahead for the economy

The list goes on. Fifth, in the low-interest period, more buyers opted for variable-rate mortgages, and they have faced instant resets with the sharp rise in interest rates this year. Changes in housing market conditions — especially selling prices — are like a nasty double-whammy for recent homebuyers. The list could be longer, but here’s one more: housing is a key leading indicator of economic activity. Where it goes, the rest of the economy usually follows. Recent homebuyers won’t be the only ones to get jolted; they are just the first to feel it.

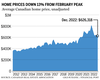

Numbers released on Jan. 16 by the Canadian Real Estate Association (CREA) are sobering. Sales of existing dwellings fell 21 per cent in the second quarter of this year, then 14 per cent in the third and a further five per cent in the fourth to bring the year as a whole down by 38 per cent. True, this comes after an extraordinary surge in 2020-21, but sales levels are currently 16 per cent below the three-year pre-pandemic average. Through another lens, current sales have only been this far below the 10-year average twice since 2007, and the wedge is currently comparable to what we experienced in the 2009 recession.

New homebuilding activity seems to strongly disagree. In contrast to the United States market, housing starts in Canada are on a tear. Temporary factors might be the reason. Last year there was a highly unusual surge of non-permanent residents, a large portion of which were composed of Ukrainian immigrants fleeing war. This is expected to continue boosting building activity into 2023, as over 135,000 arrivals from Ukraine by land and air occurred in 2022, while at latest count, approved applications number over 470,000.

The conflict between the existing and new home markets, typically perfect substitutes, is a puzzle. However, the solution might simply come down to timing. Builders are under intense pressure to run hard while the market is red hot. But it takes time to buy land, zone it, clear it, service it, promote it, and then get on with the building. If you want a house now, it’s likely easier to buy an existing one — suggesting this latter market is a better indication of true, immediate market conditions.

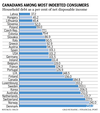

If misery loves company, we’re almost flat out of luck. While interest rates are rising just about everywhere, housing markets aren’t reacting the same as Canada’s. Of the 14 countries covered in an Oxford Economics study late last year, Canada’s housing price correction is the largest, with only Sweden and New Zealand coming anywhere close. Their peak-to-trough forecast has Canada falling 30 per cent, New Zealand down 28 per cent, Sweden declining 20 per cent and Australia and the U.K. each shedding 11 per cent. All the rest are in the single digits, averaging a relatively mild four per cent correction. We are clearly the outlier at the bad end of the distribution.

If housing is still a reliable bellwether of the broader economy — and there’s no good reason to believe it isn’t — then alarming weakness at the leading edge of this prescient market spells trouble ahead. I earnestly hope that those who are confidently predicting a mild correction are right. I fear we are in for something much worse.

Peter Hall is chief executive of Econosphere Inc., and the former chief economist at Export Development Canada.

Continue Reading

OTTAWA – Canada’s unemployment rate held steady at 6.5 per cent last month as hiring remained weak across the economy.

Statistics Canada’s labour force survey on Friday said employment rose by a modest 15,000 jobs in October.

Business, building and support services saw the largest gain in employment.

Meanwhile, finance, insurance, real estate, rental and leasing experienced the largest decline.

Many economists see weakness in the job market continuing in the short term, before the Bank of Canada’s interest rate cuts spark a rebound in economic growth next year.

Despite ongoing softness in the labour market, however, strong wage growth has raged on in Canada. Average hourly wages in October grew 4.9 per cent from a year ago, reaching $35.76.

Friday’s report also shed some light on the financial health of households.

According to the agency, 28.8 per cent of Canadians aged 15 or older were living in a household that had difficulty meeting financial needs – like food and housing – in the previous four weeks.

That was down from 33.1 per cent in October 2023 and 35.5 per cent in October 2022, but still above the 20.4 per cent figure recorded in October 2020.

People living in a rented home were more likely to report difficulty meeting financial needs, with nearly four in 10 reporting that was the case.

That compares with just under a quarter of those living in an owned home by a household member.

Immigrants were also more likely to report facing financial strain last month, with about four out of 10 immigrants who landed in the last year doing so.

That compares with about three in 10 more established immigrants and one in four of people born in Canada.

This report by The Canadian Press was first published Nov. 8, 2024.

The Canadian Press. All rights reserved.

The Canadian Institute for Health Information says health-care spending in Canada is projected to reach a new high in 2024.

The annual report released Thursday says total health spending is expected to hit $372 billion, or $9,054 per Canadian.

CIHI’s national analysis predicts expenditures will rise by 5.7 per cent in 2024, compared to 4.5 per cent in 2023 and 1.7 per cent in 2022.

This year’s health spending is estimated to represent 12.4 per cent of Canada’s gross domestic product. Excluding two years of the pandemic, it would be the highest ratio in the country’s history.

While it’s not unusual for health expenditures to outpace economic growth, the report says this could be the case for the next several years due to Canada’s growing population and its aging demographic.

Canada’s per capita spending on health care in 2022 was among the highest in the world, but still less than countries such as the United States and Sweden.

The report notes that the Canadian dental and pharmacare plans could push health-care spending even further as more people who previously couldn’t afford these services start using them.

This report by The Canadian Press was first published Nov. 7, 2024.

Canadian Press health coverage receives support through a partnership with the Canadian Medical Association. CP is solely responsible for this content.

The Canadian Press. All rights reserved.

As Canadians wake up to news that Donald Trump will return to the White House, the president-elect’s protectionist stance is casting a spotlight on what effect his second term will have on Canada-U.S. economic ties.

Some Canadian business leaders have expressed worry over Trump’s promise to introduce a universal 10 per cent tariff on all American imports.

A Canadian Chamber of Commerce report released last month suggested those tariffs would shrink the Canadian economy, resulting in around $30 billion per year in economic costs.

More than 77 per cent of Canadian exports go to the U.S.

Canada’s manufacturing sector faces the biggest risk should Trump push forward on imposing broad tariffs, said Canadian Manufacturers and Exporters president and CEO Dennis Darby. He said the sector is the “most trade-exposed” within Canada.

“It’s in the U.S.’s best interest, it’s in our best interest, but most importantly for consumers across North America, that we’re able to trade goods, materials, ingredients, as we have under the trade agreements,” Darby said in an interview.

“It’s a more complex or complicated outcome than it would have been with the Democrats, but we’ve had to deal with this before and we’re going to do our best to deal with it again.”

American economists have also warned Trump’s plan could cause inflation and possibly a recession, which could have ripple effects in Canada.

It’s consumers who will ultimately feel the burden of any inflationary effect caused by broad tariffs, said Darby.

“A tariff tends to raise costs, and it ultimately raises prices, so that’s something that we have to be prepared for,” he said.

“It could tilt production mandates. A tariff makes goods more expensive, but on the same token, it also will make inputs for the U.S. more expensive.”

A report last month by TD economist Marc Ercolao said research shows a full-scale implementation of Trump’s tariff plan could lead to a near-five per cent reduction in Canadian export volumes to the U.S. by early-2027, relative to current baseline forecasts.

Retaliation by Canada would also increase costs for domestic producers, and push import volumes lower in the process.

“Slowing import activity mitigates some of the negative net trade impact on total GDP enough to avoid a technical recession, but still produces a period of extended stagnation through 2025 and 2026,” Ercolao said.

Since the Canada-United States-Mexico Agreement came into effect in 2020, trade between Canada and the U.S. has surged by 46 per cent, according to the Toronto Region Board of Trade.

With that deal is up for review in 2026, Canadian Chamber of Commerce president and CEO Candace Laing said the Canadian government “must collaborate effectively with the Trump administration to preserve and strengthen our bilateral economic partnership.”

“With an impressive $3.6 billion in daily trade, Canada and the United States are each other’s closest international partners. The secure and efficient flow of goods and people across our border … remains essential for the economies of both countries,” she said in a statement.

“By resisting tariffs and trade barriers that will only raise prices and hurt consumers in both countries, Canada and the United States can strengthen resilient cross-border supply chains that enhance our shared economic security.”

This report by The Canadian Press was first published Nov. 6, 2024.

The Canadian Press. All rights reserved.

News4 hours ago

Train derailment and spill near Montreal leads to confinement order

News4 hours ago

Nova Scotia election: Liberals promise to improve cellphone services and highways

News5 hours ago

Hospitality workers to rally for higher wages as hotel costs soar during Swift tour

Investment5 years ago

dynaCERT Inc. Invites You to Join Us at the Vancouver Resource Investment Conference | INN – Investing News Network

Sports5 years ago

AP source: Bears acquiring quarterback Nick Foles from Jaguars – Sportsnet.ca

Media1 year ago

12 Bizarre Things People Did Just To Make Social Media Content

-

News5 hours ago

News5 hours agoEnergy experts think Donald Trump will make tariff exemptions for Canadian oil

-

News23 hours ago

News23 hours agoBad traffic, changed plans: Toronto braces for uncertainty of its Taylor Swift Era

-

News5 hours ago

News5 hours agoRent inflation to slow in the next few years, Desjardins predicts

-

News5 hours ago

News5 hours agoTrudeau off to APEC in Peru, G20 summit in Brazil as peer nations brace for Trump

-

News5 hours ago

News5 hours agoWatchdog says Tims card brouhaha shows N.S. electoral officer needs fining power

-

News5 hours ago

News5 hours agoHospitality workers to rally for higher wages as hotel costs soar during Swift tour

-

News4 hours ago

News4 hours agoNova Scotia election: Liberals promise to improve cellphone services and highways

-

News4 hours ago

News4 hours agoTrain derailment and spill near Montreal leads to confinement order