RBC sees home prices falling 14% before the dust settles

Reviews and recommendations are unbiased and products are independently selected. Postmedia may earn an affiliate commission from purchases made through links on this page.

Article content

Good Morning!

Advertisement 2

Article content

Article content

Seven months and 300 basis points into the Bank of Canada’s hiking cycle and homebuyers remain on the defensive.

Housing data last week revealed that the national composite MLS Home Price Index fell another 1.6 per cent in August from the month before.

“It’s now down 7.4 per cent since February’s peak, within striking distance of the 8% peak-to-trough decline recorded during 2017-2019 downturn,” wrote RBC assistant chief economist Robert Hogue in a note.

And most agree it’s not over yet.

RBC sees the housing market decline continuing with the Bank expected to keep hiking interest rates until the end of the year. After the Bank’s last increase on Sept. 7, RBC economists now forecast the policy rate will rise to 4 per cent, up from the 3.5 per cent they had previously expected.

Advertisement 3

Article content

“Higher interest rates will disqualify more buyers from obtaining a mortgage and shrink the size of a mortgage others can qualify for,” said Hogue.

Ontario and British Columbia, and increasingly Quebec and parts of Atlantic Canada, are suffering the biggest declines, Hogue said, with home sales falling below pre-pandemic levels last month.

Corrections are steepest in the most overheated markets. Over the past six months, the composite MLS Home Price Index has plunged 19 per cent in Cambridge, Ontario, 16 per cent in Kitchener-Waterloo and London, 15 per cent in Brantford and 13 per cent in Guelph. Chilliwack, B.C., is down 14 per cent and the Fraser Valley, nine per cent.

Eastern Canada has fared better, but “downward pressure is intensifying,” said Hogue. Montreal prices are down 3.3 per cent over the past three months, about half the drop in Toronto. But Halifax has fallen 6.3 per cent in the same time period, with a 3.9 per cent drop in August alone. Prices in Saint John, New Brunswick, fell 4.2 per cent last month.

Advertisement 4

Article content

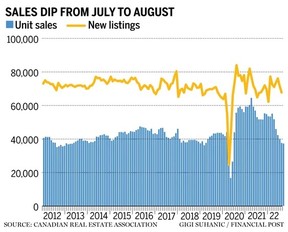

Still August’s national data leaves some room for optimism. Home sales fell one per cent from the month before, and while it’s the sixth monthly drop in a row, it was also the smallest. Compared to a year ago, sales were down 24.7 per cent in August, a smaller decline than the 29 per cent seen in July.

“August saw national sales hold steady month-to-month for the first time since February which, along with a stabilization of demand/supply conditions in many markets, could be an early sign that this year’s sharp adjustment in housing markets across Canada may have mostly run its course,” Canadian Real Estate Association chair Jill Oudil, said in the release of August’s data.

The average national home price, different than the composite home price index, was also up 1.9 per cent in August from July to $663,000 on a seasonally adjusted basis, the first increase after five months of decline.

Advertisement 5

Article content

However, Randall Bartlett, senior director of Canadian economics at Desjardins, says a closer look at the details should curb any budding enthusiasm.

Gains in the average price month over month were concentrated in the Greater Toronto Area, and the composite benchmark prices, which he says better reflects market conditions, are still falling.

“We believe this is more likely to be a dead cat bounce than a bounce back in the Canadian housing market,” he wrote in a note Thursday.

RBC, which predicts home sales will fall 23 per cent this year and another 15 per cent next, doesn’t expect the market to hit bottom until the spring, by which time prices will have fallen 14 per cent from their peak nationwide.

Ontario and B.C. will experience bigger declines of 16 per cent, while markets in Alberta and Saskatchewan prices are expected to lose just four per cent.

Advertisement 6

Article content

_____________________________________________________________

Was this newsletter forwarded to you? Sign up here to get it delivered to your inbox.

_____________________________________________________________

THE QUEEN’S QUILT As the world marks the funeral of Queen Elizabeth II today, here is a story of a woman in Nunavut who over the decades has accumulated what she believes is the largest private collection of Queen Elizabeth-themed souvenirs in the Canadian Arctic. Teacups, saucers, cookie tins, pots, spoons, old newspapers, magazines, books about the royal family, Joy Suluk has it all, totalling some 200 objects. But there is a twist in this tale. One day in 1994, the Queen herself showed up on an official visit to Rankin Inlet, and while touring an artisanal fair, bought a handmade blue-and-white quilt with polar bears and whales on it from a speechless Suluk. That’s the quilt above. Get the whole story from the Financial Post’s Joe O’Connor. Photo from Joy Suluk

Advertisement 7

Article content

___________________________________________________

- The government of Canada will hold a national ceremony in honour of the late Queen Elizabeth II, who passed away on Sept. 8

- Today’s Data: Canadian industrial product and raw materials price indices

_______________________________________________________

All but set in stone’: More economists join chorus predicting a Canadian recession

The Bank of Canada is losing money for the first time ever on rising rates

Quiet quitting is nonsense: Expecting all staff to work above and beyond is a mistake

Structured notes can offer investors some protection when markets are volatile

FP Answers: Pros and cons of fixed vs variable mortgages as borrowing rates rise

Advertisement 8

Article content

Send your small business questions to the Financial Post

_____________________________________________

__________

Everybody is watching housing starts these days for signs of whether construction will follow the housing market into a historic downturn.

Data from the Canada Mortgage and Housing Corporation Friday showed Canadian housing starts fell 2.8 per cent to 267,443 units on a seasonally adjusted annual basis in August. Despite the decline, housing starts are still near record levels and the six-month moving average inched higher to 267,309 units.

“Construction activity continues to hold up remarkably well in the face of an historic downturn in the Canadian home resale market. Still, starts are showing signs of weakening,” wrote Marc Desormeaux, Desjardins principal economist, in a note after the data was released.

Advertisement 9

Article content

Desjardins believes this is just the early innings of a downturn in home construction and it expects the effects of the cooling housing market to increasingly spill over into the building sector, gaining force as the Bank of Canada raises interest rates again in October.

“We are of the mind that this will eventually push the Canadian economy into recession in the first half of 2023,” Desormeaux wrote.

__________________________________________

Rents are soaring in Canadian cities, up 32 per cent in Metro Vancouver and 18 per cent in Toronto.

Our content parent MoneyWise has some tips on how to navigate today’s “unreal” rental market and find an affordable place to live as demand and prices increase.

____________________________________________________

Today’s Posthaste was written by Pamela Heaven (@pamheaven), with additional reporting from The Canadian Press, Thomson Reuters and Bloomberg.

Have a story idea, pitch, embargoed report, or a suggestion for this newsletter? Email us at [email protected], or hit reply to send us a note.

Listen to Down to Business for in-depth discussions and insights into the latest in Canadian business, available wherever you get your podcasts. Check out the latest episode below: