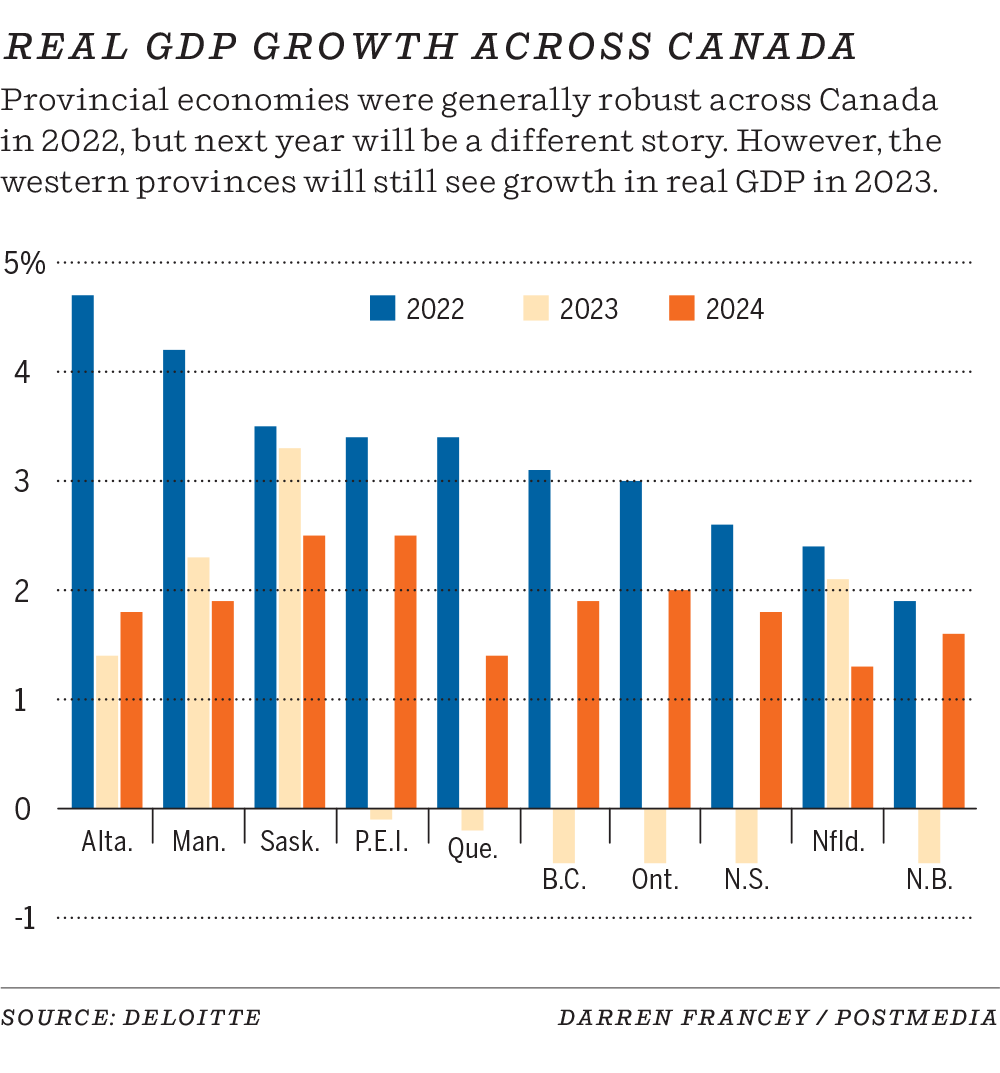

According to Deloitte’s latest economic outlook, Alberta will avoid a recession over the next year, a claim Canada will not be able to make as a whole

“Higher costs for everything have been squeezing household budgets,” said St-Arnaud. “There’s a big decline in purchasing power and consumers will have to do some choices in terms of where and how do they spend. There’s some discretionary spending that won’t happen. Big spending on cars, furniture, appliances, might have to be delayed. Part of the slowdown of the economy is that you’ll see weaker consumer spending as we get into the end of the year.”

But data suggests that higher interest rates are starting to have an effect on cooling inflation, though St-Arnaud said the hikes likely are not done — he agrees with the prognostication of a 50-basis-point bump next month and says there could be an additional 25-point increase before the end of this year.

“We saw some moderation in recent months, but that was mainly due to an easing in gasoline prices,” said St-Arnaud. “(The Bank of Canada) still needs to continue to increase interest rates, but we’re getting to that peak in terms of how much they’ll increase.”

Alberta remains one of the most affordable provinces in the country, which is credited with continued net positive interprovincial migration. In the second quarter of 2022, the total was 9,857 for a fourth-consecutive quarter of positive results. In that time, 23,132 Canadians relocated to Alberta; 15,208 in 2022.

“It’s so important to have people coming in,” she said. “All of these industries, whether they’re the traditional ones or the more growing and emerging ones, are going to need the skilled workers. These positive migration numbers are a great indication that our goal to get these skilled positions filled is going to come to fruition.”

The last time there were four consecutive quarters of net-positive interprovincial migration to Alberta was the third quarter of 2014 to the second quarter of 2015 — also the last time there were four-digit positive gains.

Fir pointed to affordable housing, lower taxes and diversified job opportunities as the draws. Many people are coming to Alberta from Ontario and B.C., where the province has rolled out its Alberta is Calling campaign.

This has been exemplified by recent announcements such as De Havilland announcing plans for a massive manufacturing plant in Wheatland County and Infosys doubling the number of positions for its new office in downtown Calgary to 1,000. There has been further investment in hydrogen production, lithium extraction and agri-sciences.

One positive of the impending slowdown is Deloitte is not expecting employment to bottom out, as it often does in a recession. MacDonald said the current tight labour market will help mitigate some of these pains.

“If you’re looking at laying off staff, you have to ask yourself, ‘how easy is it going to be to get these staff back when demand starts to pick back up?’ ” she said. “We think employers are going to hold on to their employees a lot longer than they normally would during a period of slowdown, just because it’s been so difficult to find the right skills for the jobs that are out there.”

Written by

Twitter: @JoshAldrich03