The Bank of Russia acted quickly to shield the nation’s $1.5 trillion economy from sweeping sanctions that hit key banks, pushed the ruble to a record low and left President Vladimir Putin unable to access much of his war chest of more than $640 billion.

The central bank more than doubled its key interest rate to 20%, the highest in almost two decades, and imposed some controls on the flow of capital. It was part of a barrage of announcements that eventually restored some calm after a rout that pushed some Russian Eurobonds into distressed territory last week.

“The Bank of Russia will be very flexible in using all necessary instruments,” Governor Elvira Nabiullina said in brief televised remarks in Moscow.

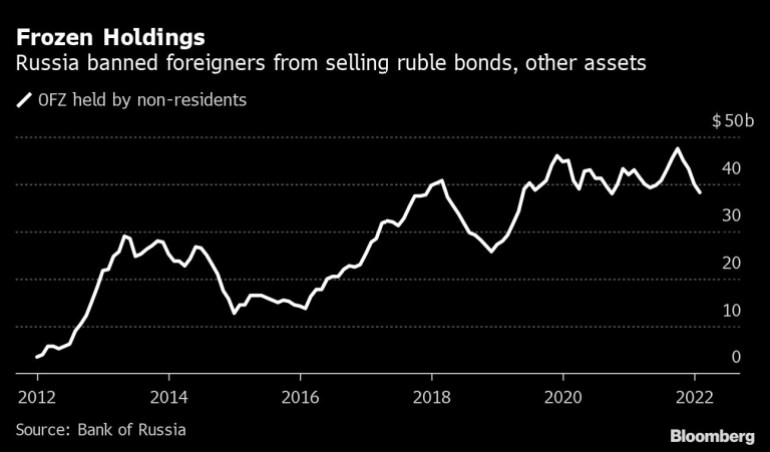

Facing the risk of a bank run, a rapid sell-off in assets and the steepest depreciation in the ruble since 1998, policy makers banned brokers from selling securities held by foreigners starting Monday on the Moscow Exchange. Exporters were ordered to start mandatory hard-currency revenue sales and stock trading was temporarily suspended in Moscow.

“The ruble has ceased to be a freely convertible currency with the sweeping sanctions,” said Friedrich Heinemann, head of the corporate taxation and public finance department at German think thank ZEW. “In terms of currency policy, this throws Russia back to the early 1990s and the time before the country’s comprehensive economic opening.”

Less than a week after Putin ordered his military to invade Ukraine, Russia is at risk of succumbing to the biggest financial crisis of his more than two decades in power. He gathered Nabiullina and other top officials in the Kremlin to discuss plans for a response, calling the U.S. and its allies who joined in the sanctions “the empire of lies.”

The steps taken so far on Monday represent the most forceful measures by Russia after the latest round of sanctions, with the U.S. and the European Union agreeing to block access to much of the $640 billion the country’s central bank has built up as a buffer to protect the economy.

Additional measures taken by global governments to exclude some Russian banks from the SWIFT messaging system could further choke up the country’s banking system. Sanctioned institutions dominate Russia’s financial sector with $1 trillion in assets.

But the U.S. and Europe remain reluctant for now to sanction Russian energy, seeking to insulate the world economy from a greater shock. Germany’s Economy Ministry said on Monday that purchases of Russian gas remain possible using SWIFT even after the latest curbs.

In the absence of even wider trade sanctions that could ensnare Russian energy shipments, the policies implemented so far may be enough to stabilize markets, according to Renaissance Capital. The ruble recouped some losses and was trading nearly 14% weaker at around 96 per dollar as of 4:26 p.m. in Moscow. It was briefly down more than 30% earlier in the day.

“All these measures should limit the depreciation of the ruble,” said Sofya Donets, economist at Renaissance Capital in Moscow. “If the run on FX continues, we would anticipate additional direct restrictions on domestic operations.”

Nabiullina, who took no questions from reporters on Monday, said the central bank didn’t intervene in the currency market on Monday as a result of the limitations on its reserves. It spent $1 billion last Thursday and a smaller amount the following day to shore up the ruble, she said.

“We will make further decisions on monetary policy based on how the actual situation develops while assessing risks primarily in terms of the external conditions,” Nabiullina said.

Decisions to suspend some regulatory requirements amounted to a capital boost for banks by the equivalent of 900 billion rubles ($8.6 billion), she said.

The ruble’s 24% drop so far this year is the worst slump globally, prices compiled by Bloomberg show. At current levels the ruble’s slump is the biggest since 1998, the year the nation’s economy went into a tailspin and the government defaulted on its local debt.

S&P Global Ratings lowered Russia’s credit score below investment grade on Friday, while Moody’s Investors Service — which rates Russia one notch above junk — put the nation on review for a downgrade.

Policy makers are counting that the steep rate hike, alongside the mandatory conversion of export revenues and a halt to outflows from the financial market, will help restore confidence and minimize losses at home even as war continues to rage across the border.

“This is merely a reaction by the central bank to the fact that sanctions have weakened, completely neutralized their defense arsenal that they’ve built up in the past five to 10 years,” said Simon Harvey, head of FX analysis at Monex Europe Ltd. “It’s unprecedented escalation and markets are very poorly positioned for it.”

Russians were already lining up at cash machines around the country as demand for foreign currency soared. The central bank has said it was increasing supplies to ATMs to meet need and issued another statement Sunday vowing to provide banks “uninterrupted” supplies of rubles.

Most of Europe has closed its airspace to Russian carriers, which could make it difficult to physically transport cash into the country.

“I think rubles will be plenty, the question is FX,” said Viktor Szabo, an investor at Aberdeen Asset Management Plc. in London. “With reserves partially blocked, the central bank will have to prioritize, and I guess population will not be on top of the list.”

Oil and gas revenue remains a lifeline as the sale and transport of energy have largely escaped disruptions. At current prices, Russia was running a monthly current-account surplus of about $20 billion.

Still, damage to the economy will be severe from the combination of wild swings in the exchange rate and the soaring cost of money. Bloomberg Economics was already predicting a contraction in the first and second quarter even before the weekend’s sanctions and now sees the risk of an even “deeper downturn.”

Renaissance Capital said it now expects a recession this year, compared to a forecast of 3% growth expected as recently as last week.

The continued flow of oil will likely provide some relief, given the World Bank calculates commodities account for almost 70% of goods exports. About 43% of the country’s crude and condensate output is sold abroad.

If crude prices stay around $90 this year, the country’s budget could get more than $65 billion in extra revenue, adding to the Kremlin’s financial strength, economists said recently. Oil at $100 would boost the windfall closer to $73 billion.

In Russia, memories linger of hyperinflation that peaked at more than 2,500 percent in 1992 and wiped out savings in the wake of the Soviet collapse. Price growth is already running at more than double the central bank’s target, despite a series of rate hikes since last March.

Renaissance Capital estimates the suspension of operations with non-residents alone could prevent $50 billion in possible capital outflows in the coming weeks. The freeze on such transactions may stay in place for long, according to RenCap’s Donets.

“These measures may help calm down the increased market nervousness, but at the same time they undermine the foundation of monetary policy, which is focused on inflation targeting and a flexible exchange rate,” said Natalia Lavrova, chief economist at BCS Financial Group in Moscow. “We do not rule out a possible rate hike going forward or further unexpected and non-market decisions.”

(Updates with governor’s comments starting in third paragraph.)

OTTAWA – Canada’s unemployment rate held steady at 6.5 per cent last month as hiring remained weak across the economy.

Statistics Canada’s labour force survey on Friday said employment rose by a modest 15,000 jobs in October.

Business, building and support services saw the largest gain in employment.

Meanwhile, finance, insurance, real estate, rental and leasing experienced the largest decline.

Many economists see weakness in the job market continuing in the short term, before the Bank of Canada’s interest rate cuts spark a rebound in economic growth next year.

Despite ongoing softness in the labour market, however, strong wage growth has raged on in Canada. Average hourly wages in October grew 4.9 per cent from a year ago, reaching $35.76.

Friday’s report also shed some light on the financial health of households.

According to the agency, 28.8 per cent of Canadians aged 15 or older were living in a household that had difficulty meeting financial needs – like food and housing – in the previous four weeks.

That was down from 33.1 per cent in October 2023 and 35.5 per cent in October 2022, but still above the 20.4 per cent figure recorded in October 2020.

People living in a rented home were more likely to report difficulty meeting financial needs, with nearly four in 10 reporting that was the case.

That compares with just under a quarter of those living in an owned home by a household member.

Immigrants were also more likely to report facing financial strain last month, with about four out of 10 immigrants who landed in the last year doing so.

That compares with about three in 10 more established immigrants and one in four of people born in Canada.

This report by The Canadian Press was first published Nov. 8, 2024.

The Canadian Institute for Health Information says health-care spending in Canada is projected to reach a new high in 2024.

The annual report released Thursday says total health spending is expected to hit $372 billion, or $9,054 per Canadian.

CIHI’s national analysis predicts expenditures will rise by 5.7 per cent in 2024, compared to 4.5 per cent in 2023 and 1.7 per cent in 2022.

This year’s health spending is estimated to represent 12.4 per cent of Canada’s gross domestic product. Excluding two years of the pandemic, it would be the highest ratio in the country’s history.

While it’s not unusual for health expenditures to outpace economic growth, the report says this could be the case for the next several years due to Canada’s growing population and its aging demographic.

Canada’s per capita spending on health care in 2022 was among the highest in the world, but still less than countries such as the United States and Sweden.

The report notes that the Canadian dental and pharmacare plans could push health-care spending even further as more people who previously couldn’t afford these services start using them.

This report by The Canadian Press was first published Nov. 7, 2024.

Canadian Press health coverage receives support through a partnership with the Canadian Medical Association. CP is solely responsible for this content.

As Canadians wake up to news that Donald Trump will return to the White House, the president-elect’s protectionist stance is casting a spotlight on what effect his second term will have on Canada-U.S. economic ties.

Some Canadian business leaders have expressed worry over Trump’s promise to introduce a universal 10 per cent tariff on all American imports.

A Canadian Chamber of Commerce report released last month suggested those tariffs would shrink the Canadian economy, resulting in around $30 billion per year in economic costs.

More than 77 per cent of Canadian exports go to the U.S.

Canada’s manufacturing sector faces the biggest risk should Trump push forward on imposing broad tariffs, said Canadian Manufacturers and Exporters president and CEO Dennis Darby. He said the sector is the “most trade-exposed” within Canada.

“It’s in the U.S.’s best interest, it’s in our best interest, but most importantly for consumers across North America, that we’re able to trade goods, materials, ingredients, as we have under the trade agreements,” Darby said in an interview.

“It’s a more complex or complicated outcome than it would have been with the Democrats, but we’ve had to deal with this before and we’re going to do our best to deal with it again.”

American economists have also warned Trump’s plan could cause inflation and possibly a recession, which could have ripple effects in Canada.

It’s consumers who will ultimately feel the burden of any inflationary effect caused by broad tariffs, said Darby.

“A tariff tends to raise costs, and it ultimately raises prices, so that’s something that we have to be prepared for,” he said.

“It could tilt production mandates. A tariff makes goods more expensive, but on the same token, it also will make inputs for the U.S. more expensive.”

A report last month by TD economist Marc Ercolao said research shows a full-scale implementation of Trump’s tariff plan could lead to a near-five per cent reduction in Canadian export volumes to the U.S. by early-2027, relative to current baseline forecasts.

Retaliation by Canada would also increase costs for domestic producers, and push import volumes lower in the process.

“Slowing import activity mitigates some of the negative net trade impact on total GDP enough to avoid a technical recession, but still produces a period of extended stagnation through 2025 and 2026,” Ercolao said.

Since the Canada-United States-Mexico Agreement came into effect in 2020, trade between Canada and the U.S. has surged by 46 per cent, according to the Toronto Region Board of Trade.

With that deal is up for review in 2026, Canadian Chamber of Commerce president and CEO Candace Laing said the Canadian government “must collaborate effectively with the Trump administration to preserve and strengthen our bilateral economic partnership.”

“With an impressive $3.6 billion in daily trade, Canada and the United States are each other’s closest international partners. The secure and efficient flow of goods and people across our border … remains essential for the economies of both countries,” she said in a statement.

“By resisting tariffs and trade barriers that will only raise prices and hurt consumers in both countries, Canada and the United States can strengthen resilient cross-border supply chains that enhance our shared economic security.”

This report by The Canadian Press was first published Nov. 6, 2024.