Economic shocks like the coronavirus pandemic of 2020 only arrive once every few generations, and they bring about permanent and far-reaching change.

Measured by output, the world economy is well on the way to recovery from a slump the likes of which barely any of its 7.7 billion people have seen in their lifetimes. Vaccines should accelerate the rebound in 2021. But other legacies of Covid-19 will shape global growth for years to come.

Some are already discernible. The takeover of factory and service jobs by robots will advance, while white-collar workers get to stay home more. There’ll be more inequality between and within countries. Governments will play a larger role in the lives of citizens, spending—and owing—more money. What follows is an overview of some of the transformations under way.

Leviathan

Big government staged a comeback as the social contract between society and the state got rewritten on the fly. It became commonplace for authorities to track where people went and who they met—and to pay their wages when employers couldn’t manage it. In countries where free-market ideas had reigned for decades, safety nets had to be patched up.

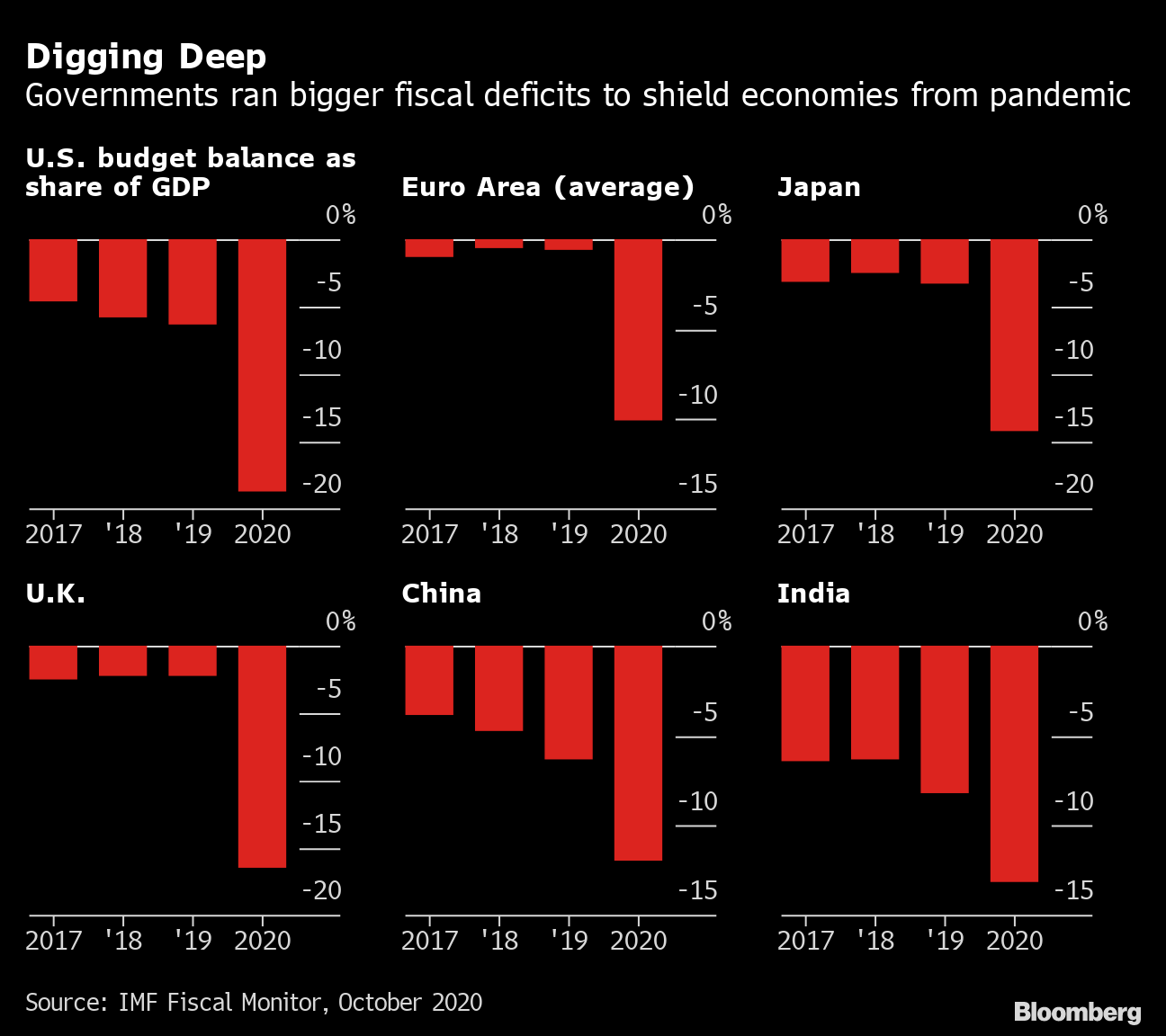

Digging Deep

Governments ran bigger fiscal deficits to shield economies from pandemic

Source: IMF Fiscal Monitor, October 2020

.chart-js display: none;

To pay for these interventions, the world’s governments ran budget deficits that add up to $11 trillion this year, according to McKinsey & Co. There’s already a debate about how long such spending can continue, and when taxpayers will have to start footing the bill. At least in developed economies, ultralow interest rates and unfazed financial markets don’t point to a near-term crisis.

In the longer run, a big rethink in economics is changing minds about public debt. The new consensus says governments have more room to spend in a low-inflation world, and should use fiscal policy more proactively to drive their economies. Advocates of Modern Monetary Theory say they pioneered those arguments and the mainstream is only now catching up.

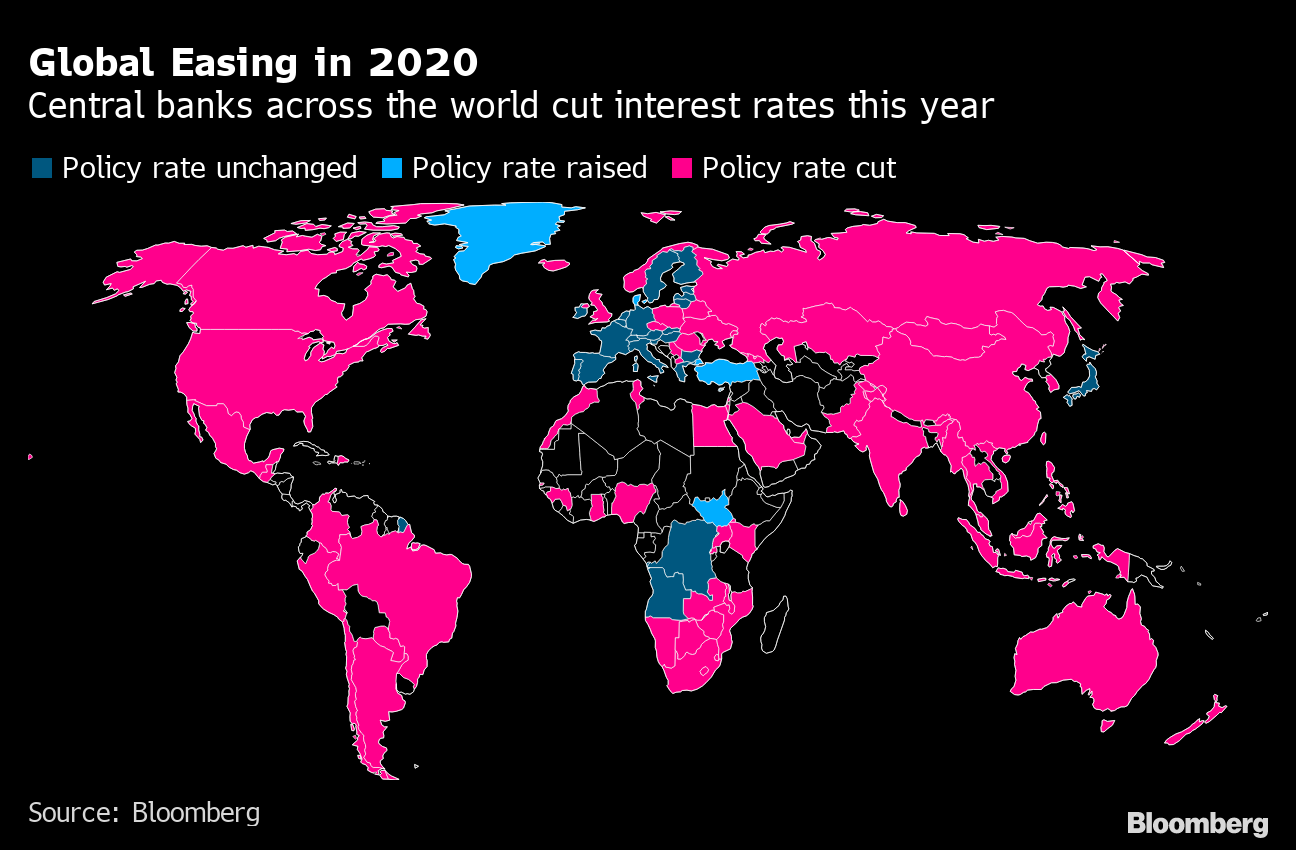

Even Easier Money

Central banks were plunged back into printing money. Interest rates hit new record lows. Central bankers stepped up their quantitative easing, widening it to buy corporate as well as government debt.

All these monetary interventions have created some of the easiest financial conditions in history—and unleashed a frenzy of speculative investment, which has left plenty of analysts worried about moral hazards ahead. But the central-bank policies will be hard to reverse, especially if labor markets remain fractured and companies continue their recent run-up in saving.

Global Easing in 2020

Central banks across the world cut interest rates this year

Source: Bloomberg

.chart-js display: none;

And history shows that pandemics depress interest rates for a long time, according to a paper published this year. It found that a quarter-century after the disease struck, rates were typically some 1.5 percentage points lower than they otherwise would have been.

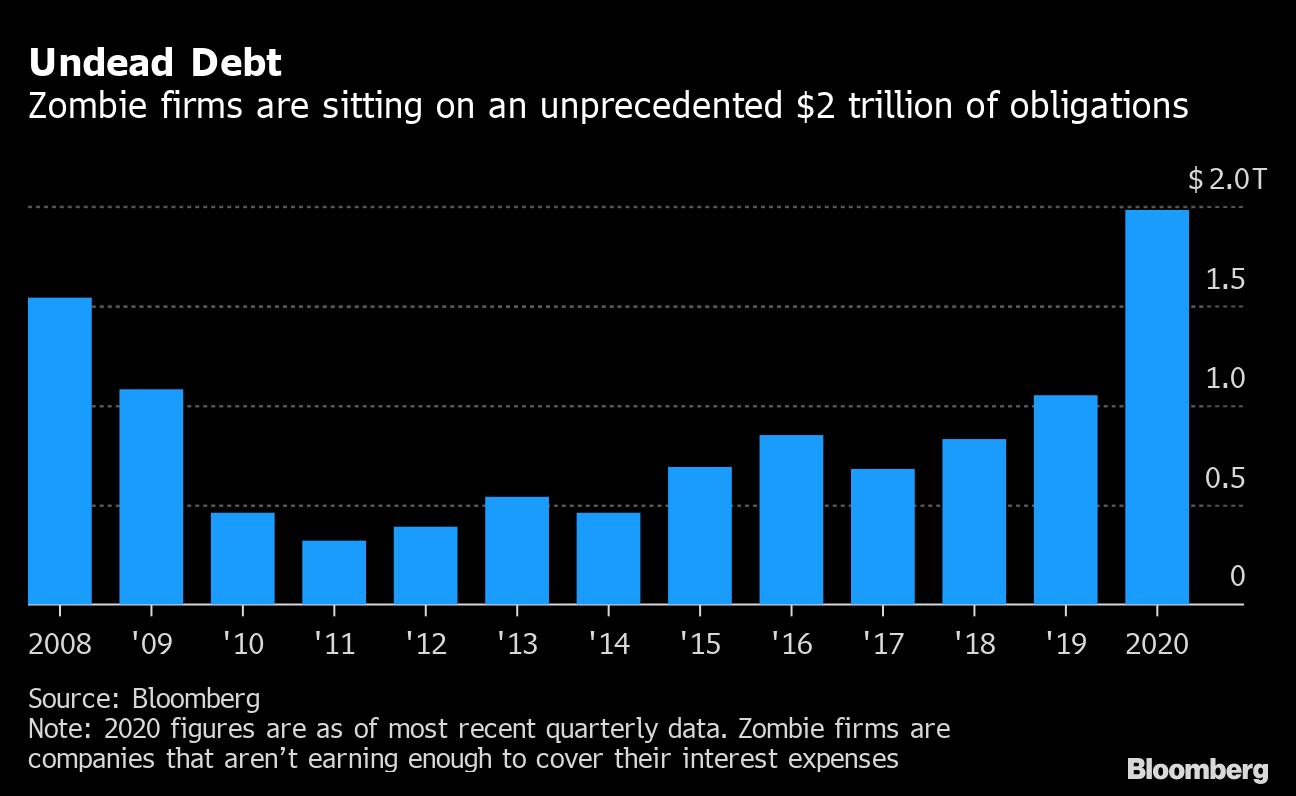

Debts and Zombies

Governments offered credit as a lifeline during the pandemic—and business grabbed it. One result was a surge in corporate debt levels across the developed world. The Bank for International Settlements calculates that nonfinancial companies borrowed a net $3.36 trillion in the first half of 2020.

With revenues plunging in many industries because of lockdowns or consumer caution, and losses eating into business balance sheets, the conditions are in place for a “major corporate solvency crisis,” according to one new report.

Undead Debt

Zombie firms are sitting on an unprecedented $2 trillion of obligations

Source: Bloomberg

Note: 2020 figures are as of most recent quarterly data. Zombie firms are companies that aren’t earning enough to cover their interest expenses

.chart-js display: none;

Some also see danger in offering too much support for companies, with too little discrimination over who gets it. They say that’s a recipe for creating “zombie firms” that can’t survive in a free market and are only kept alive by state aid—making the whole economy less productive.

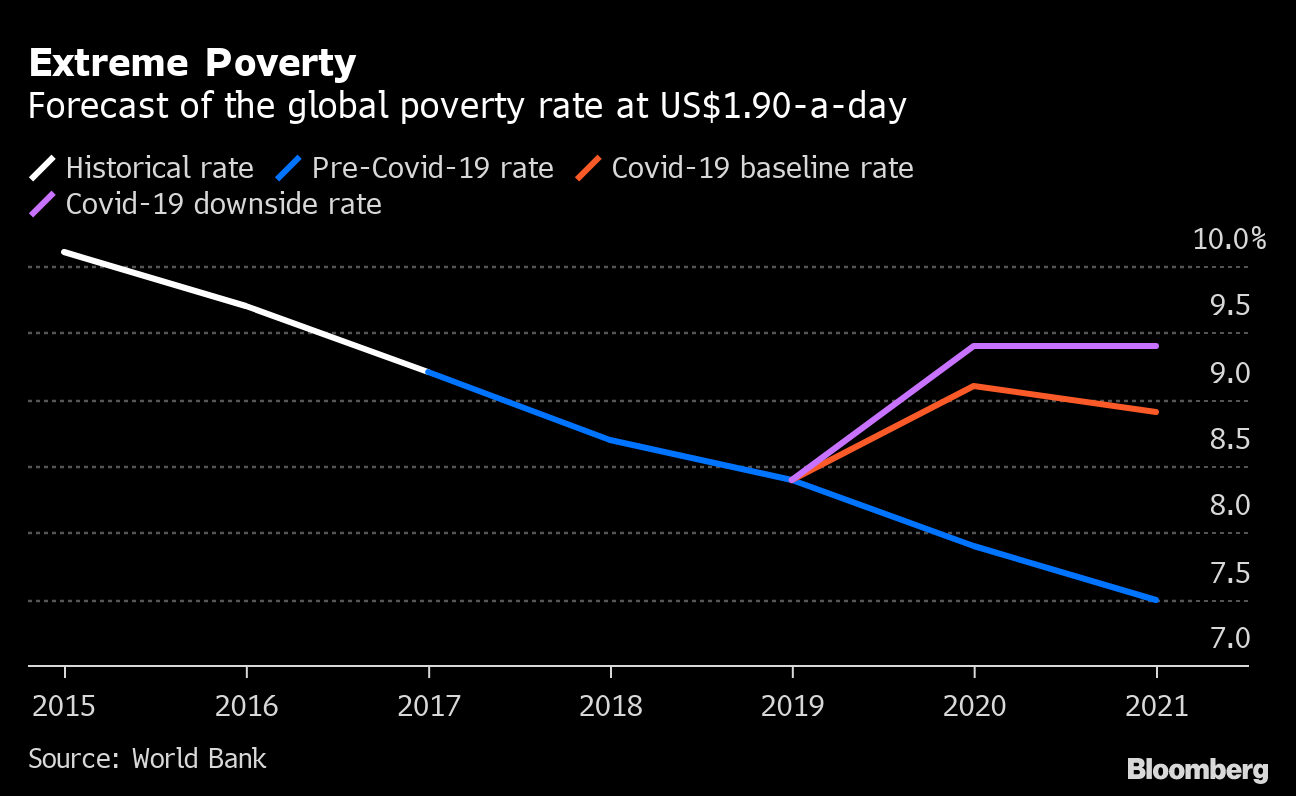

Great Divides

The stimulus debate can feel like a first-world luxury. Poor countries lack the resources to protect jobs and businesses—or invest in vaccines—the way wealthier peers have done, and they’ll need to tighten belts sooner or risk currency crises and capital flight.

Forecast of the global poverty rate at US$1.90-a-day

Source: World Bank

.chart-js display: none;

Creditor governments in the G-20 have taken some steps to ease the plight of the poorest borrowers, but they’ve been slammed by aid groups for offering only limited debt relief and failing to rope private investors into the plan.

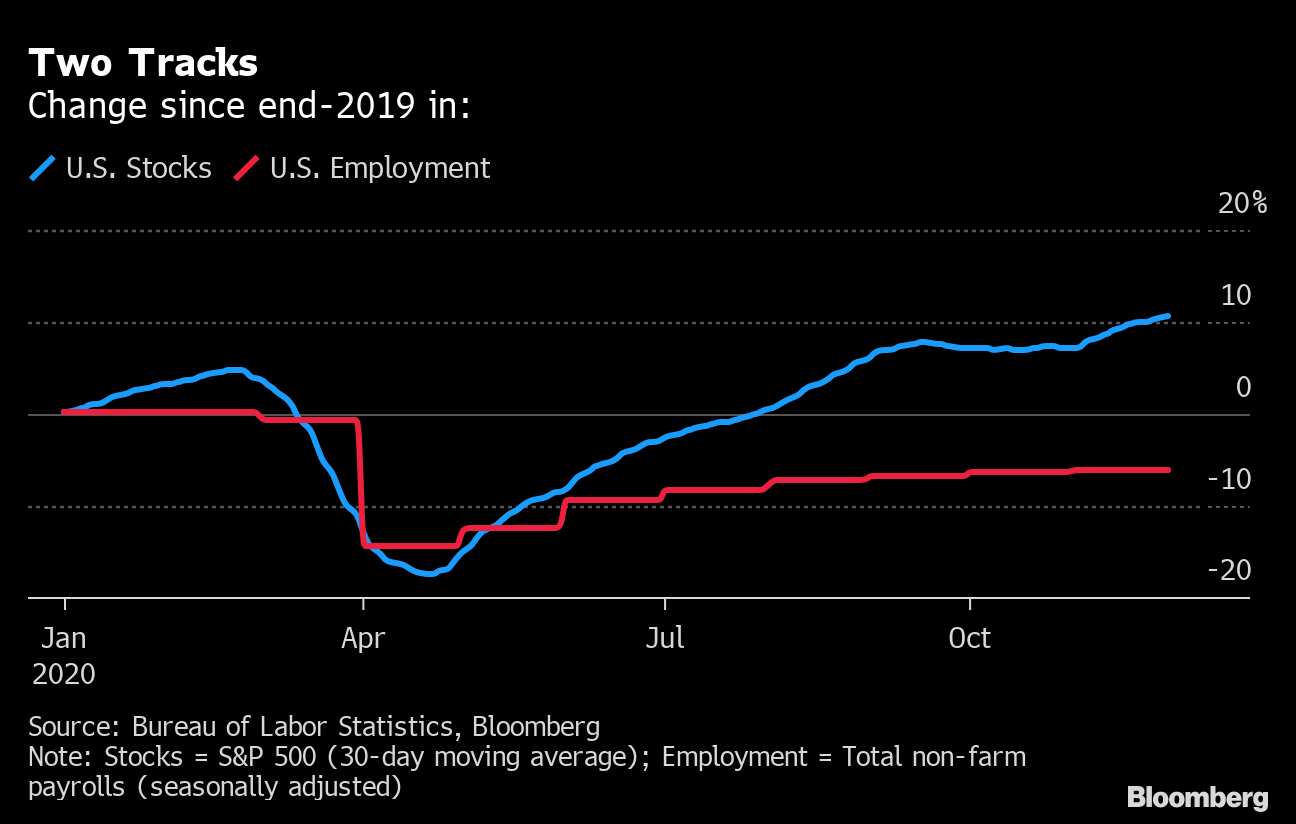

K-Shaped

Low-paying work in services, where there’s more face-to-face contact with customers, tended to disappear first as economies locked down. And financial markets, where assets are mostly owned by the rich, came roaring back much faster than job markets.

The upshot has been labeled a “K-shaped recovery.” The virus has widened income or wealth gaps across faultlines of class, race and gender.

Women have been hit disproportionately hard—partly because they’re more likely to work in the industries that struggled, but also because they had to shoulder much of the extra childcare burden as schools closed. In Canada, women’s participation in the labor force fell to the lowest since the mid-1980s.

Rise of the Robots

Covid-19 triggered new concerns about physical contact in industries where social distancing is tough—like retail, hospitality or warehousing. One fix is to replace the humans with robots.

Who’s Automating?

Asian powerhouses lead among world’s top 10 manufacturers

Source: United Nations Statistics Division, International Federation of Robotics

.chart-js display: none;

Research suggests that automation often gains ground during a recession. In the pandemic, companies accelerated work on machines that can check guests into hotels, cut salads at restaurants, or collect fees at toll booths. And shopping moved further online.

These innovations will make economies more productive. But they also mean that when it’s safe to go back to work, some jobs just won’t be there. And the longer people stay unemployed, the more their skills can atrophy—something economists call “hysteresis.”

You’re on Mute

Higher up the income ladder, remote offices suddenly became the norm. One study found that two-thirds of U.S. GDP in May was generated by people working at home. Many companies told employees to stay away from the office well into 2021, and some signaled they’ll make flexible work permanent.

Work-from-home has mostly passed the technology test, giving employers and staff new options. That’s a worry for businesses catering to the old infrastructure of office life, from commercial real estate to food and transportation. It’s a boon for those building a new one: shares in videoconferencing platform Zoom jumped more than six-fold this year.

Not Working

Google mobility data show workplace activity is still below pre-crisis levels

Source: Google, Bloomberg calculations

.chart-js display: none;

The option of remote work, along with fear of the virus, also triggered a stampede of urbanites toward the suburbs or countryside—and in some countries, a surge in rural property prices.

Not Going Anywhere?

Some kinds of travel came to a near halt. Global tourism fell 72% in the year through October, according to the United Nations. McKinsey reckons a quarter of business trips could disappear forever as meetings move online.

No Travel

International tourist arrivals were down 72% through October

Source: World Tourism Organization

.chart-js display: none;

With vacations upended and mass events like festivals and concerts called off, the trend among consumers to favor “experiences” over goods has been disrupted. And when activities do resume, they may not be the same. “We still don’t know how concerts are going to be, really,” says Rami Haykal, co-owner of the Elsewhere venue in Brooklyn. “People will be more mindful, I think, of personal space, and avoiding places that are overly packed.”

Travelers may have to carry mandatory health certificates and pass through new kinds of security. Hong Kong based China Tech Global has developed a mobile disinfection booth that it’s trying to sell to airports. Chief Executive Sammy Tsui says it can clear pathogens from the body and clothes in 40 seconds or less. “You feel some cool air on your body, and some mist,” he says. “But you don’t feel wet.”

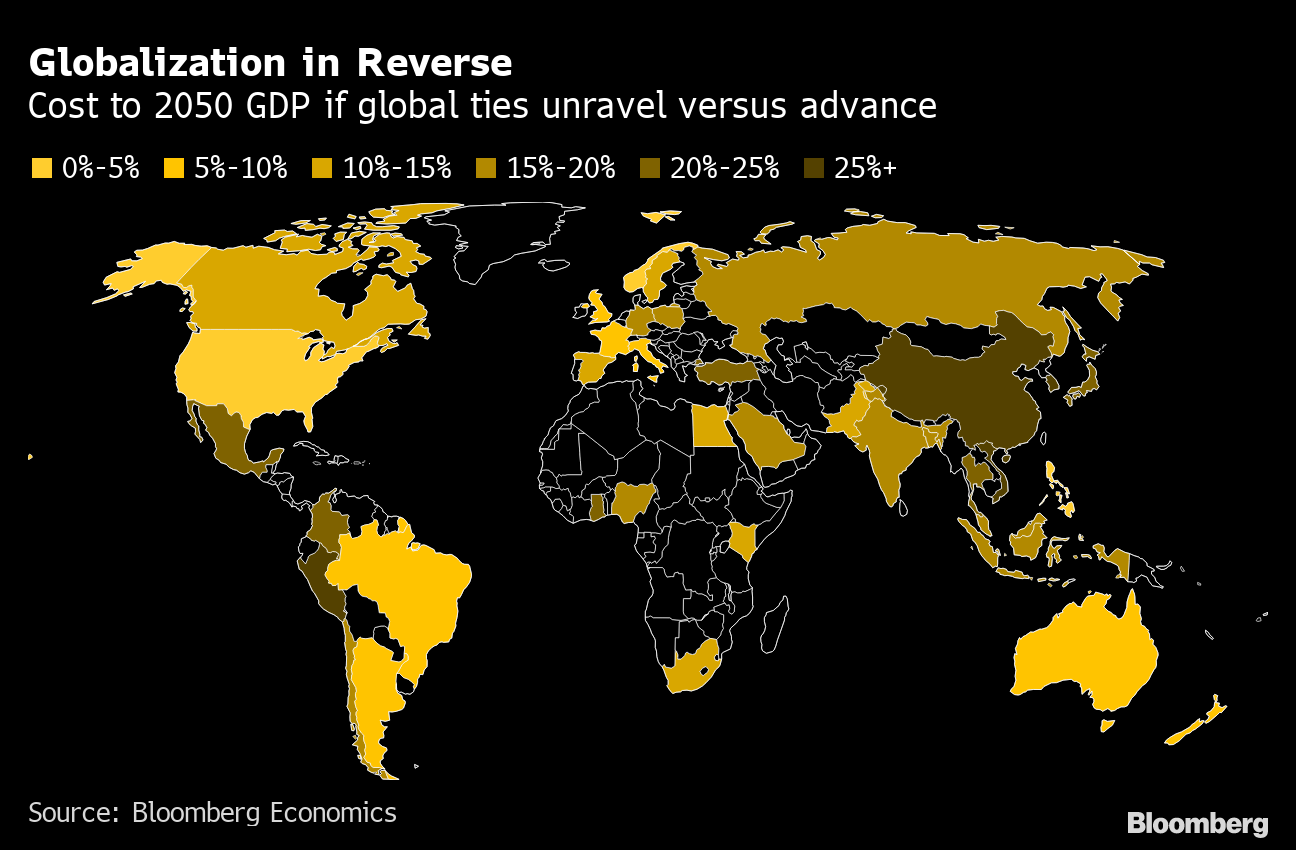

A Different Globalization

When Chinese factories shut down early in the pandemic, it sent shock waves through supply chains everywhere—and made businesses and governments reconsider their reliance on the world’s manufacturing powerhouse.

Sweden’s NA-KD.com, for example, is part of a flourishing “fast fashion” retail industry that moves with social media trends rather than the traditional seasons. After deliveries got jammed this year, the company shifted some production from China to Turkey, says Julia Assarsson, head of inbound and customs.

Globalization in Reverse

Cost to 2050 GDP if global ties unravel versus advance

Source: Bloomberg Economics

.chart-js display: none;

That’s an example of globalization adjusting without retreating. In other areas, the pandemic may encourage politicians who argue that it’s risky to rely on imports of goods vital to national security—as ventilators and masks turned out to be this year.

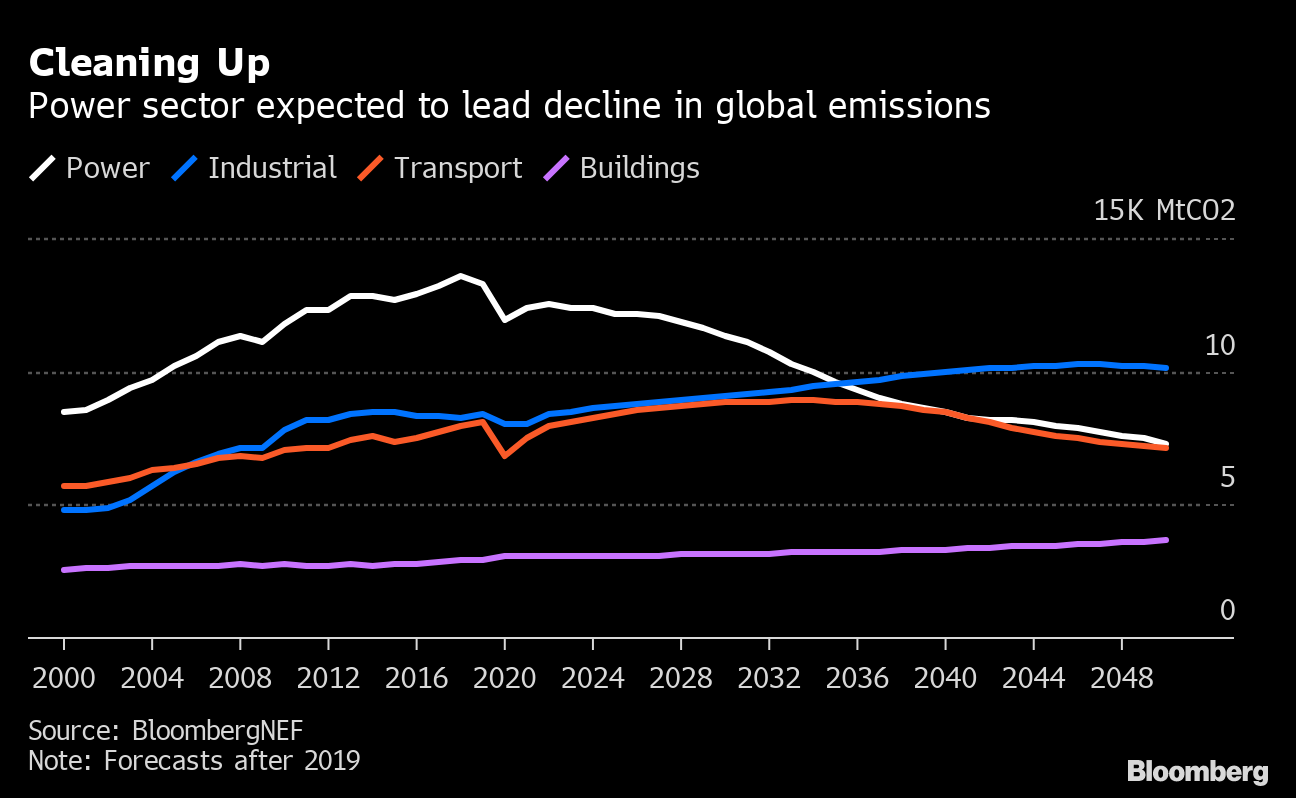

Going Green

Before the pandemic, it was mainly environmentalists musing over theories of peak oil—the idea that the rise of electric vehicles could permanently dent the world’s demand for one of the most polluting fossil fuels.

But when 2020 saw planes grounded and people staying home, even oil majors like BP felt a real threat from the world getting serious about climate.

Cleaning Up

Power sector expected to lead decline in global emissions

Source: BloombergNEF

Note: Forecasts after 2019

.chart-js display: none;

Governments from California to the U.K. announced plans to ban the sale of new gasoline and diesel cars by 2035. And Joe Biden was elected with a promise the U.S. will rejoin the Paris Agreement.

— With assistance by Olivia Rockeman, Brendan Murray, Matthew Boesler, Patrick Gillespie, Shelly Hagan, Mario Sergio Lima, and Jess Shankleman

The Canadian Institute for Health Information says health-care spending in Canada is projected to reach a new high in 2024.

The annual report released Thursday says total health spending is expected to hit $372 billion, or $9,054 per Canadian.

CIHI’s national analysis predicts expenditures will rise by 5.7 per cent in 2024, compared to 4.5 per cent in 2023 and 1.7 per cent in 2022.

This year’s health spending is estimated to represent 12.4 per cent of Canada’s gross domestic product. Excluding two years of the pandemic, it would be the highest ratio in the country’s history.

While it’s not unusual for health expenditures to outpace economic growth, the report says this could be the case for the next several years due to Canada’s growing population and its aging demographic.

Canada’s per capita spending on health care in 2022 was among the highest in the world, but still less than countries such as the United States and Sweden.

The report notes that the Canadian dental and pharmacare plans could push health-care spending even further as more people who previously couldn’t afford these services start using them.

This report by The Canadian Press was first published Nov. 7, 2024.

Canadian Press health coverage receives support through a partnership with the Canadian Medical Association. CP is solely responsible for this content.

As Canadians wake up to news that Donald Trump will return to the White House, the president-elect’s protectionist stance is casting a spotlight on what effect his second term will have on Canada-U.S. economic ties.

Some Canadian business leaders have expressed worry over Trump’s promise to introduce a universal 10 per cent tariff on all American imports.

A Canadian Chamber of Commerce report released last month suggested those tariffs would shrink the Canadian economy, resulting in around $30 billion per year in economic costs.

More than 77 per cent of Canadian exports go to the U.S.

Canada’s manufacturing sector faces the biggest risk should Trump push forward on imposing broad tariffs, said Canadian Manufacturers and Exporters president and CEO Dennis Darby. He said the sector is the “most trade-exposed” within Canada.

“It’s in the U.S.’s best interest, it’s in our best interest, but most importantly for consumers across North America, that we’re able to trade goods, materials, ingredients, as we have under the trade agreements,” Darby said in an interview.

“It’s a more complex or complicated outcome than it would have been with the Democrats, but we’ve had to deal with this before and we’re going to do our best to deal with it again.”

American economists have also warned Trump’s plan could cause inflation and possibly a recession, which could have ripple effects in Canada.

It’s consumers who will ultimately feel the burden of any inflationary effect caused by broad tariffs, said Darby.

“A tariff tends to raise costs, and it ultimately raises prices, so that’s something that we have to be prepared for,” he said.

“It could tilt production mandates. A tariff makes goods more expensive, but on the same token, it also will make inputs for the U.S. more expensive.”

A report last month by TD economist Marc Ercolao said research shows a full-scale implementation of Trump’s tariff plan could lead to a near-five per cent reduction in Canadian export volumes to the U.S. by early-2027, relative to current baseline forecasts.

Retaliation by Canada would also increase costs for domestic producers, and push import volumes lower in the process.

“Slowing import activity mitigates some of the negative net trade impact on total GDP enough to avoid a technical recession, but still produces a period of extended stagnation through 2025 and 2026,” Ercolao said.

Since the Canada-United States-Mexico Agreement came into effect in 2020, trade between Canada and the U.S. has surged by 46 per cent, according to the Toronto Region Board of Trade.

With that deal is up for review in 2026, Canadian Chamber of Commerce president and CEO Candace Laing said the Canadian government “must collaborate effectively with the Trump administration to preserve and strengthen our bilateral economic partnership.”

“With an impressive $3.6 billion in daily trade, Canada and the United States are each other’s closest international partners. The secure and efficient flow of goods and people across our border … remains essential for the economies of both countries,” she said in a statement.

“By resisting tariffs and trade barriers that will only raise prices and hurt consumers in both countries, Canada and the United States can strengthen resilient cross-border supply chains that enhance our shared economic security.”

This report by The Canadian Press was first published Nov. 6, 2024.

OTTAWA – Statistics Canada says the country’s merchandise trade deficit narrowed to $1.3 billion in September as imports fell more than exports.

The result compared with a revised deficit of $1.5 billion for August. The initial estimate for August released last month had shown a deficit of $1.1 billion.

Statistics Canada says the results for September came as total exports edged down 0.1 per cent to $63.9 billion.

Exports of metal and non-metallic mineral products fell 5.4 per cent as exports of unwrought gold, silver, and platinum group metals, and their alloys, decreased 15.4 per cent. Exports of energy products dropped 2.6 per cent as lower prices weighed on crude oil exports.

Meanwhile, imports for September fell 0.4 per cent to $65.1 billion as imports of metal and non-metallic mineral products dropped 12.7 per cent.

In volume terms, total exports rose 1.4 per cent in September while total imports were essentially unchanged in September.

This report by The Canadian Press was first published Nov. 5, 2024.