That tearing sound you hear is economic forecasts being ripped up and thrown in the trash. Over the past few days, the continuing spread of the dangerous new coronavirus has driven the Bank of Canada and the U.S. Federal Reserve to slash interest rates, prompted airlines to project staggering losses, kneecapped oil prices, and sent stock and bond markets into pandemonium.

Epidemiologists and public-health officers are racing to find answers to one of the biggest global health challenges since the SARS epidemic of 2003. While they do so, businesses are delaying investments, postponing expansion and putting off travel. Global economic growth could fall to 1 per cent this year, down from 2.6 per cent last year, the Institute for International Finance warned this week. If so, it would be the slowest growth since 2009.

Some sectors are already badly wounded. Just two weeks ago, the International Air Transport Association had warned that global airlines were set to lose US$29.3-billion in passenger revenue as a result of COVID-19. This week, it supersized its estimate, saying the potential virus-related losses had ballooned to as much as US$113-billion.

Story continues below advertisement

Stock markets are gyrating in huge nervous swings – rocketing up one day this week, only to plunge the next. The bond market, meanwhile, is pricing in outright fear. The prices of safe government bonds in Canada and the United States hit historic highs this week as investors rushed to find havens at any price.

While the ultimate scope of the virus outbreak remains very much in doubt, the uncertainty around the disease is poisonous in its own right. It freezes decision-making and casts a pall over risk-taking. That is creating a cascading series of risks.

Now the job for monetary and fiscal policy makers worldwide is to insulate the economy and businesses from as much damage as possible until the virus’s spread is either arrested or runs its course. That means ensuring elevated levels of corporate and consumer debt don’t turn into a crisis.

For policy makers, it’s a challenge unlike anything before. The global financial crisis in 2008 prompted historic rate cuts by the Fed and Bank of Canada to provide a lifeline for ailing banks amid a widespread freeze of the credit system. Governments spent hundreds of billions of dollars to bail out systemically important companies.

One problem now, however, is that central banks are nearly out of ammunition.

Ever since the crisis, central bankers have served as the prime caregivers for sickly economies. They have repeatedly chopped interest rates to resuscitate activity.

This week, both the Fed and the Bank of Canada chopped their policy rates by half a percentage point in a single go – something they had not done since the 2008-09 debacle.

Story continues below advertisement

But with their key policy rates now hovering just over 1 per cent, they have little room left to lower rates compared with past recessions, when they typically cut those rates by five percentage points in quick stages to bolster growth.

Analysts are already expecting further rate cuts by central banks. Some are now talking about the possibility of zero interest rates in the U.S.

But to further stimulate economies, governments would have to take fiscal action – boost spending, cut taxes or both. Leaders say they are ready to do that. Finance Minister Bill Morneau told a Toronto business audience on Friday that Ottawa has the “fiscal firepower” to respond to the economic fallout from the viral outbreak. For affected businesses and workers, “we have the tools to respond quickly” he said, although he didn’t outline specific measures.

Many analysts say plunging yields on U.S Treasury bonds and Canadian government bonds are a sign of deeper economic trouble to come.

“Like it or not, the Treasury yield curve and fed funds futures market now assign an uncomfortably high implied probability to a painful contraction of corporate earnings and a pronounced worsening of the corporate default outlook arriving by the end of 2020,” John Lonski, chief economist at Moody’s Capital Markets Research, wrote in a note this week.

Story continues below advertisement

If lenders turn more skittish, even otherwise healthy companies may find it difficult to refinance their debt.

“Our current assumption is that the virus-related disruption is not severe enough to prompt a widespread business debt crisis” on a global level, says Simon MacAdam, global economist at Capital Economics in London. “But if the virus triggers a sharper drop in profits or a bigger rise in borrowing costs than we envisage, then these pockets of vulnerability could blow up.”

He says that Canada stands out as a particularly concerning case. In this country, “high borrowing costs and poor earnings – particularly in the oil and gas industries – mean that operating profits barely cover interest expenses” in some cases.

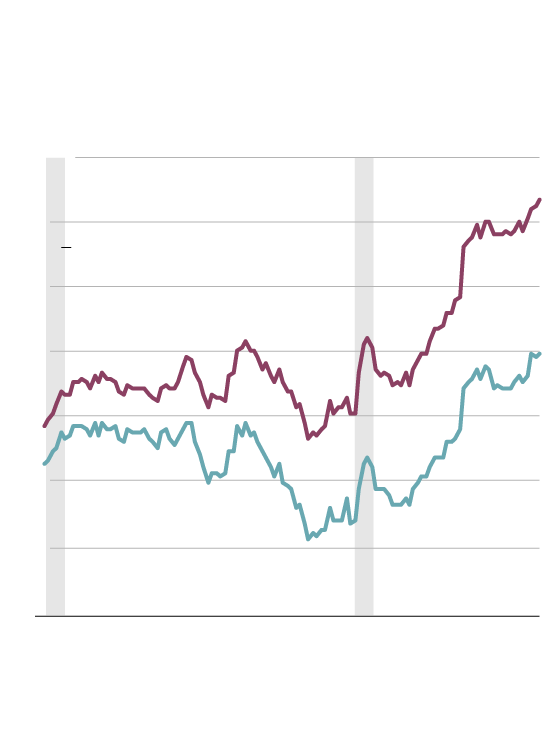

Both Canadian households and the corporate sector have taken on high levels of debt over the past decade.

Excluding the big banks and other financial companies, Canada’s ratio of total debt to annual gross domestic product (GDP) is now 119 per cent. Not only is that a record high, it’s also among the highest in the developed world.

Canadian Non-financial

Corporate Debt in Perspective

Percentage of nominal GDP

Total Debt

JOHN SOPINSKI/THE GLOBE AND MAIL

SOURCE: td economics

Canadian Non-financial

Corporate Debt in Perspective

Percentage of nominal GDP

Total Debt

JOHN SOPINSKI/THE GLOBE AND MAIL, SOURCE: td economics

Canadian Non-financial Corporate Debt in Perspective

Percentage of nominal GDP

Total Debt

JOHN SOPINSKI/THE GLOBE AND MAIL, SOURCE: td economics

By contrast, Canada’s non-financial debt to GDP was about 80 per cent going into the Great Recession of 2008-09, according to the Bank of International Settlements.

Story continues below advertisement

“Corporate balance sheets have never been this vulnerable to a recession before. Not even close,” said David Rosenberg, head of Rosenberg Research and Associates.

To be sure, many growing companies have deliberately added debt knowing that prevailing low interest rates provide an attractive way to finance expansion without undue balance-sheet pressure.

For heavily indebted corporations, however, there are two key risks. The first is that a major hit to earnings would make it more difficult to keep up with debt payments.

Second, vulnerable borrowers could have trouble refinancing their maturing debt obligations if the economic toll from the coronavirus outbreak spreads enough to make lenders tighten their credit standards. And as investors stampede away from corporate bonds into safer government bonds, the yield spread between them widens.

“In the event of an economic downturn, corporate indebtedness could result in widening corporate bond spreads and increased delinquency rates, which would amplify the severity of a downturn,” TD economists James Orlando and Brett Saldarelli wrote in a recent report.

The growth of corporate debt in the years since the global financial crisis has been a worldwide phenomenon.

Story continues below advertisement

Between December, 2008, and December, 2019, the global stock of non-financial corporate bonds doubled, according to a recent OECD report. Credit quality has broadly deteriorated over that time, as lenders have readily supplied riskier borrowers with financing.

According to the International Monetary Fund’s latest report on global financial stability, a global economic shock only half as severe as the one in 2009 would put nearly 40 per cent of corporate debt in major economies “at risk.” That means companies carrying US$19-trillion in debt would not have enough profits to cover their interest payments.

rising corporate debt service ratios

amid stable interest rates

Debt Service Ratio

DSR* Avg. (2000-2009)

DSR* Avg. (2010-2019)

*Debt service ratio

JOHN SOPINSKI/THE GLOBE AND MAIL

SOURCE: td economics

rising corporate debt service ratios

amid stable interest rates

Debt Service Ratio

DSR* Avg. (2000-2009)

DSR* Avg. (2010-2019)

*Debt service ratio

JOHN SOPINSKI/THE GLOBE AND MAIL, SOURCE: td economics

rising corporate debt service ratios amid stable interest rates

Debt Service Ratio

DSR* Avg. (2000-2009)

DSR* Avg. (2010-2019)

*Debt service ratio

JOHN SOPINSKI/THE GLOBE AND MAIL, SOURCE: td economics

Financial markets have begun to factor in the rising risk of credit crunch. In the U.S., the yields on speculative-grade bonds, also known as “junk bonds,” have spiked in comparison with 10-year Treasuries. That spread – a crucial gauge of risk sentiment – widened to 11.8 per cent on Thursday, up from 9.6 per cent in mid-February, when the threat of a pandemic started to spill into credit markets.

That’s a pretty big move in a short period of time, Mr. Orlando said. But while investors are clearly growing concerned about the market’s weakest borrowers, current high-yield spreads are far from pricing in a wave of defaults. Back in 2015-16, when a growth scare in China roiled markets, the spread on the lowest grade of U.S. corporate bonds widened to 20 percentage points. And at the depths of the global financial crisis, it climbed to more than 40 points.

Falling energy prices certainly won’t help earnings forecasts for Canadian oil and gas producers. Since January, the price of West Texas Intermediate crude has fallen by about one-third to a three-and-a-half year low of about US$41 a barrel.

An escalating outbreak could scare lenders away from the energy sector’s marginal borrowers. Despite a wave of debt reduction, cost cutting and consolidation in the oil patch over the past five years, there are still companies in the sector just treading water.

Story continues below advertisement

“There are a number of zombie companies out there who have managed to keep the lights on for a lot longer than I would have been expected,” said Robert Mark, a portfolio manager at Raymond James and former energy analyst. “I’m surprised there haven’t been more bankruptcies.”

Investors’ rush to buy government bonds has pushed yields to next to nothing – a mere 0.6 per cent in the case of a 10-year Government of Canada bond, for instance. This supposedly safe debt is now a significant money loser for savers once you factor in the corrosive effect of inflation.

That situation is unlikely to change any time soon, says Drummond Brodeur, chief global strategist at Signature Global Asset Management. He assumes central banks will leave rates as low as possible to encourage growth, stoke inflation and avoid a Japan-like situation in which deflationary expectations become embedded in the economy.

The prospect of what could be years of an ultralow-rate environment confronts households with a nasty choice – invest in bonds that will almost certainly erode their savings or take their chances in a stock market that has been shooting up and down with wild abandon in recent days.

Analysts at J.P. Morgan, Rabobank and NatWest Markets warn the benchmark federal funds rate in the U.S. could hit zero this year. For now, the consensus in the futures market is just slightly more optimistic – it sees the U.S. policy rate dipping below 20 basis points (one fifth of a percentage point) by the end of 2020.

Central banks in Europe and Japan have taken their policy rates into negative territory, but such drastic action appears unlikely in Canada and the U.S. “I’m dubious about negative rates,” says Eric Lascelles, chief economist at RBC Global Asset Management. “There is a big debate about whether they actually work.”

Low or negative rates may actually slow economic growth by forcing households to save even more for retirement to offset the effect of falling yields. Lower mortgage rates would risk propelling Canada’s already frothy housing market into even more extreme territory.

If conventional monetary policy is running out of room to stimulate the economy, attention may have to turn to more innovative measures. In a 2015 speech, Bank of Canada Governor Stephen Poloz outlined several unconventional policy options to deal with crises. One intriguing idea is “funding for credit” – a scheme in which the central bank would provide money to commercial banks for lending to sectors that may be facing short-term credit crunches.

“The idea is to make sure that economically important sectors continue to have access to funding even when the supply of credit is impaired,” Mr. Poloz said in his 2015 speech. “In this case, the central bank would provide collateralized funding at a subsidized rate as long as banks met specified lending objectives.”

An even simpler idea would be for governments to step in and unleash a new wave of fiscal stimulus to cushion any virus-related downturn. Policy makers could also craft specific measures aimed at particularly hard hit sectors or industries. Italy, for instance, has already moved to introduce tax credits for any company that reports a 25 per cent or larger drop in revenue.

The challenge for leaders is that it is still too early to assess how deep or long the economic hit from the virus may turn out to be. “Will the rest of the world [outside China] receive a heavy, moderate or light blow from this?” Mr. Lascelles asks. “The honest answer is no one knows.”

Some observers are guardedly optimistic. “A global recession is a clear and rising risk,” says Thomas Torgerson, managing director for sovereign ratings at market watchers DBRS Morningstar in New York. “However, it is still not our baseline case.”

The hope is that the virus outbreak begins to lose force as weather warms and public-health measures come into effect, Mr. Torgerson says. In that case, any virus-related downturns in spending may be largely made up in subsequent months as lower rates and other stimulus measures help the economy.

For now, most forecasters insist the chance of a dire outcome is extremely low. The history of such viral outbreaks suggest they rarely last longer than 12 months.

“It would be surprising if in a year or two we are still seeing significant effects,” Mr. Lascelles says.

China, the origin of the new virus, provides some reason for optimism. Its hard-line approach to quarantine and mobility restrictions appears to have tamed its virus outbreak, which infected more than 80,000 people since the start of the year. It is now reporting fewer than 200 new cases a day, according to the World Health Organization.

To be sure, the country has paid a painful price. Purchasing managers indexes show Chinese business activity plummeted in February. Several indicators suggest the country’s economy is inching back to normalcy, but “the pace of improvement remains slow and economic activity is still well below normal levels,” notes Julian Evans-Pritchard, senior China economist at Capital Economics.

Remarkably, though, the CSI 300 index of Chinese stocks remains the world’s best-performing stock market so far this year. That may say something about the wave of policy measures that Beijing has unleashed to support its economy and market. It may also speak to the resilience in markets. As devastating as the human toll of the virus outbreak may be, economic activity can bounce back if the right conditions are in place.

Mr. Lascelles at RBC says that North America has enjoyed a long economic recovery since the financial crisis. In that time, the expansion has survived the euro zone crisis, Brexit and plunging oil prices. He thinks it may survive this challenge, too. “I wouldn’t count out the economy’s ability to keep on growing.”

Your time is valuable. Have the Top Business Headlines newsletter conveniently delivered to your inbox in the morning or evening. Sign up today.

TOKYO (AP) — Japanese technology group SoftBank swung back to profitability in the July-September quarter, boosted by positive results in its Vision Fund investments.

Tokyo-based SoftBank Group Corp. reported Tuesday a fiscal second quarter profit of nearly 1.18 trillion yen ($7.7 billion), compared with a 931 billion yen loss in the year-earlier period.

Quarterly sales edged up about 6% to nearly 1.77 trillion yen ($11.5 billion).

SoftBank credited income from royalties and licensing related to its holdings in Arm, a computer chip-designing company, whose business spans smartphones, data centers, networking equipment, automotive, consumer electronic devices, and AI applications.

The results were also helped by the absence of losses related to SoftBank’s investment in office-space sharing venture WeWork, which hit the previous fiscal year.

WeWork, which filed for Chapter 11 bankruptcy protection in 2023, emerged from Chapter 11 in June.

SoftBank has benefitted in recent months from rising share prices in some investment, such as U.S.-based e-commerce company Coupang, Chinese mobility provider DiDi Global and Bytedance, the Chinese developer of TikTok.

SoftBank’s financial results tend to swing wildly, partly because of its sprawling investment portfolio that includes search engine Yahoo, Chinese retailer Alibaba, and artificial intelligence company Nvidia.

SoftBank makes investments in a variety of companies that it groups together in a series of Vision Funds.

The company’s founder, Masayoshi Son, is a pioneer in technology investment in Japan. SoftBank Group does not give earnings forecasts.

Shopify Inc. executives brushed off concerns that incoming U.S. President Donald Trump will be a major detriment to many of the company’s merchants.

“There’s nothing in what we’ve heard from Trump, nor would there have been anything from (Democratic candidate) Kamala (Harris), which we think impacts the overall state of new business formation and entrepreneurship,” Shopify’s chief financial officer Jeff Hoffmeister told analysts on a call Tuesday.

“We still feel really good about all the merchants out there, all the entrepreneurs that want to start new businesses and that’s obviously not going to change with the administration.”

Hoffmeister’s comments come a week after Trump, a Republican businessman, trounced Harris in an election that will soon return him to the Oval Office.

On the campaign trail, he threatened to impose tariffs of 60 per cent on imports from China and roughly 10 per cent to 20 per cent on goods from all other countries.

If the president-elect makes good on the promise, many worry the cost of operating will soar for companies, including customers of Shopify, which sells e-commerce software to small businesses but also brands as big as Kylie Cosmetics and Victoria’s Secret.

These merchants may feel they have no choice but to pass on the increases to customers, perhaps sparking more inflation.

If Trump’s tariffs do come to fruition, Shopify’s president Harley Finkelstein pointed out China is “not a huge area” for Shopify.

However, “we can’t anticipate what every presidential administration is going to do,” he cautioned.

He likened the uncertainty facing the business community to the COVID-19 pandemic where Shopify had to help companies migrate online.

“Our job is no matter what comes the way of our merchants, we provide them with tools and service and support for them to navigate it really well,” he said.

Finkelstein was questioned about the forthcoming U.S. leadership change on a call meant to delve into Shopify’s latest earnings, which sent shares soaring 27 per cent to $158.63 shortly after Tuesday’s market open.

The Ottawa-based company, which keeps its books in U.S. dollars, reported US$828 million in net income for its third quarter, up from US$718 million in the same quarter last year, as its revenue rose 26 per cent.

Revenue for the period ended Sept. 30 totalled US$2.16 billion, up from US$1.71 billion a year earlier.

Subscription solutions revenue reached US$610 million, up from US$486 million in the same quarter last year.

Merchant solutions revenue amounted to US$1.55 billion, up from US$1.23 billion.

Shopify’s net income excluding the impact of equity investments totalled US$344 million for the quarter, up from US$173 million in the same quarter last year.

Daniel Chan, a TD Cowen analyst, said the results show Shopify has a leadership position in the e-commerce world and “a continued ability to gain market share.”

In its outlook for its fourth quarter of 2024, the company said it expects revenue to grow at a mid-to-high-twenties percentage rate on a year-over-year basis.

“Q4 guidance suggests Shopify will finish the year strong, with better-than-expected revenue growth and operating margin,” Chan pointed out in a note to investors.

This report by The Canadian Press was first published Nov. 12, 2024.

TORONTO – RioCan Real Estate Investment Trust says it has cut almost 10 per cent of its staff as it deals with a slowdown in the condo market and overall pushes for greater efficiency.

The company says the cuts, which amount to around 60 employees based on its last annual filing, will mean about $9 million in restructuring charges and should translate to about $8 million in annualized cash savings.

The job cuts come as RioCan and others scale back condo development plans as the market softens, but chief executive Jonathan Gitlin says the reductions were from a companywide efficiency effort.

RioCan says it doesn’t plan to start any new construction of mixed-use properties this year and well into 2025 as it adjusts to the shifting market demand.

The company reported a net income of $96.9 million in the third quarter, up from a loss of $73.5 million last year, as it saw a $159 million boost from a favourable change in the fair value of investment properties.

RioCan reported what it says is a record-breaking 97.8 per cent occupancy rate in the quarter including retail committed occupancy of 98.6 per cent.

This report by The Canadian Press was first published Nov. 12, 2024.