ATLANTA, GA – JANUARY 04: (L-R) Federal Reserve Chair Jerome Powell and former Chairs of the Federal … [+] Reserve Janet Yellen and Ben Bernanke participate in a panel discussion at the American Economic Association conference on January 4, 2019 in Atlanta, Georgia. Following a strong December jobs report, the Dow Jones Industrial Average rose 350 points at the open on Friday morning. In a television interview on Friday morning, National Economic Council Director Larry Kudlow said he believes there is ‘no recession in sight.’ (Photo by Jessica McGowan/Getty Images)

Getty Images

On Thursday, August 27, Fed Chair Jay Powell spoke at the Fed’s annual Jackson Hole symposium. His talk was much anticipated, as it was expected that the old 2% inflation objective would be updated. In fact, the Fed had telegraphed the change; and the Fed has been following the newly announced policy for several months.

The policy change allows the Fed to permit inflation to exceed the Fed’s announced 2% target without preemptively raising the Fed Funds rate or otherwise tightening policy to head off a rise above that 2% target, as the Fed had done beginning in 2015 and ending in 2018. In effect, the new policy is different from the one it replaces in that it changed the 2% target inflation rate from 2% as a hard ceiling to 2% as a long-term average. Since we haven’t seen 2% inflation this century, if inflation rises above 2%, the Fed won’t have to react. And it may be several years before it does react depending on how far and how fast inflation rises above that 2% “long-term” target.

Since current inflation is nowhere near 2%, there is no immediate action implied by the new policy. It does mean that interest rates will continue to be minuscule as far as the eye can see, and for a much longer period than would have been the case under the replaced policy. As indicated above, had this policy been in effect in 2015, that tightening cycle (including the monthly reductions in the Fed’s balance sheet) would likely not have occurred.

The Anomaly: Rates Spiked Up On the Policy Announcement

Despite the fact that Powell just announced that interest rates are going to be lower for longer, interest rates spiked. No doubt, someday down the road, inflation above 2% will occur if the Fed pursues this ultra-easy monetary policy long after the economy has healed. But, at this time, we are far, far from that point.

Economists have often noted that, at least theoretically, inflation appears to be partially a function of “expectations.” There is a high correlation between what consumers “expect” inflation to be, and what it actually turns out to be. Did the mere announcement by Powell that the Fed was willing to tolerate more inflation actually cause the market to add an inflation premium to the yield curve? Apparently so. Yet the reality, at least for many more quarters, is that in the service sector of the economy, where the consumer spends most of her money, prices won’t be rising above February levels – at least not in airline fares, move theater tickets, theme parks, or restaurants. Nor will rents be rising since a significant percentage of Americans have missed their rent or mortgage payments for the past few months (an eviction tsunami is coming!). These sectors have significant influence on the major rice indexes.

In addition, all of the surveys that measure consumer inflation expectations have indicated that consumers “expect” inflation to be flat to lower over the near and medium-term horizon. As mentioned above, this “new” policy wasn’t really “new,” in that the Fed had telegraphed this policy several months ago. The Wall Street Journal described this in its Friday (August 28) edition as follows:

It won’t lead to a significant change in how the Fed is currently conducting policy because it had already incorporated the changes it formally codified Thursday.

The markets already knew this. So, this wasn’t new data or a shock. Yet, rates still spiked.

Another debunked theory as to why rates have spiked is the fact that the CPI and PPI for August showed some upward price movements. That really can’t be why rates spiked, as this was just the bounce off of the price craters of April/May/June when no one would buy anything no matter what the price (except TP!). (Similarly, we don’t consider the spike in the employment data of several million people in June as the start of a tight labor market.) Here are some current data:

The NY Fed Inflation Gauge: 2% in February; currently 1.1%;

Atlanta Fed Wage Tracker: 4.1% in May; 3.6% in July;

Employment Cost Index: +0.5% – the lowest in the past five years;

Nonfarm Business Price Deflator: 1.5% in Q1; -0.2% in Q2 (first time <0 in 70 years).

It’s For the Banks

Another possible reason for the Fed to spike inflation expectations is to steepen the yield curve for the benefit of its constituent banks that need curve steepness to improve their profit margins. Banks borrow short-term but lend long-term, so a positively sloped and steep yield curve gives them higher lending rates while holding down borrowing costs. As discussed briefly in my last blog (“The Economy: On a Sugar High”), the Fed minutes for their July meeting indicated that the Fed would not be pegging the yield curve at this time. That announcement along with Thursday’s policy change clearly indicates that the Fed will tolerate a steeper yield curve.

This has other benefits, too. It supports the value of the dollar in the foreign exchange world, as higher longer-term Treasury yields attract foreigners to demand dollars to be used to purchase those Treasuries. The value of the dollar vis-a-vis other currencies has been falling since the pandemic began due to Fed money printing, and it continued its downward spiral even after this Fed announcement. But it isn’t surprising that the Fed would like to stem that trend. The price of gold is quite sensitive to the dollar’s exchange rate. It rose rapidly from early June to early August, took a breather, and now seems to have formed a base from which it may move higher.

Policy Assessment

The economists and policy makers at the Fed are top notch. As indicated above, there may be unannounced motivations for such a policy announcement. Likely, they don’t want to be caught having to raise interest rates if inflation returns while there are still significant levels of unemployment. The 2% inflation target was adopted in 2012 when the expectation was that interest rates would return to the levels experienced in the 1990s and before the Great Recession. Today, there is no such expectation. Demographics have changed such that economic growth in the developed economies is much harder to achieve. Furthermore, technology has vastly lowered production costs.

So, why is 2% still the target? Looking at the PCE deflator (Personal Consumption Expenditure Chain Price Index), the index the Fed uses to measure inflation, the Fed hasn’t achieved that inflation level since adopting the target. It has averaged about 1.5%. In fact, we haven’t had sustained 2% PCE inflation this century! What is so magic about 2%? Why not 1.5%, 1% or even 0%? Remember, the written Fed mandate is “price stability!” (Sometime back in the 80s or 90s, when asked at a Congressional hearing what the rate of inflation should be for price stability, then Chair, Alan Greenspan, answered 0%!!).

Nevertheless, Powell has laid out the path that the Fed is going to pursue, artificially low interest rates until inflation rises above 2% for a significant period of time. During this time, there will be no real price discovery in the fixed income markets, as the Fed will either intervene directly, or simply print more money to keep rates artificially low. The best hedge for investors is gold. The dollar’s value is already in the tank and is likely to erode further. If 2% isn’t the right magic inflation number and is unachievable in a world of high unemployment, the pursuit of it may cause the world to look for an alternative reserve currency.

Employment-the Seasonal Adjustment Issue

Meanwhile, the economy continues under the constraints imposed by government(s) over the pandemic issues. Employment, of course, is the primary measure of the economy’s health in today’s world. For the past few months, this blog has been following the trends in the unemployment data, both the state unemployment programs, and the new PUA program (Pandemic Unemployment Assistance) mandated by the CARES Act for the self-employed and independent contractors that don’t qualify for the state programs. The data I have been using are not-seasonally adjusted (NSA) because seasonal factors don’t make sense (i.e., the economy doesn’t seasonally shut down every March!).

Well, lo and behold, the Department of Labor (DOL) has finally recognized the seasonal adjustment (SA) issue! Beginning with the data presented on Thursday, September 3, the DOL will use much toned-down seasonal factors (i.e., using an “additive” instead of a “multiplicative” methodology. From their August 27th release:

…in the presence of a large level shift in a time series, multiplicative seasonal adjustment factors can result in systematic over- or under- adjustment…”

To explain using an example: if the normal data point is about 100,000 and the seasonal factor would add +5,000, a factor of 1.05, then, using the additive method, one would add 5,000 to 100,000 to get the SA number of 105,000. Under normal circumstances, using the multiplicative technique, 100,000*1.05 is also 105,000. But if the base suddenly jumps to 1,000,000, the additive technique puts the number at 1,005,000, while the multiplicative technique distorts the data to 1,050,000, i.e., there is a 45,000 difference in the two techniques in this example.

While this new technique will begin next week, it doesn’t appear that the SA data beginning in March will be revised. The DOL note indicates that data revisions will occur at the beginning of the calendar year. This means that there will be no consistency in the methodology used in the SA data, so best to stick with the NSA data, as I do here.

The Employment Trend

The week ended August 22 saw a -68k drop in the state Initial Claims (IC) data. This offset the disappointing IC rise of +51k the prior week. Continuing Claims (CC), those on unemployment for two consecutive weeks, showed another significant drop of nearly -273k, after falling more than -1.0 million the prior week. Looking at the table and graph, except for a three-month period in early and mid-July, the rate of decline in the ranks of “those who work for an employer” continued its downtrend. From this data, it appears that large and medium-sized companies (factories, and large white collar businesses) have begun to recall or rehire employees.

Unemployment Picture

Universal Value Advisors

The news is not as good in entrepreneur land. The PUA IC data are going the other way. PUA Initial Claims (IC) rose +83k the week ended August 22, after having risen +35k the prior week (August 15). I am guessing that the business re-opening pauses or reversals in some states is, at least partially responsible, as it is small businesses (bars, restaurants, salons …) that suffer most with these closures and social distancing rules. It is these constituents who would most likely use the PUA programs. The spike here may also be due to catch-up, as PUA is a new program (awareness on the part of the public, and capacity on the part of the administrative agency). Data for PUA Continuing Claims (CC) for the week ended August 8 (latest data) did fall -252k.

Combined State & PUA Claims

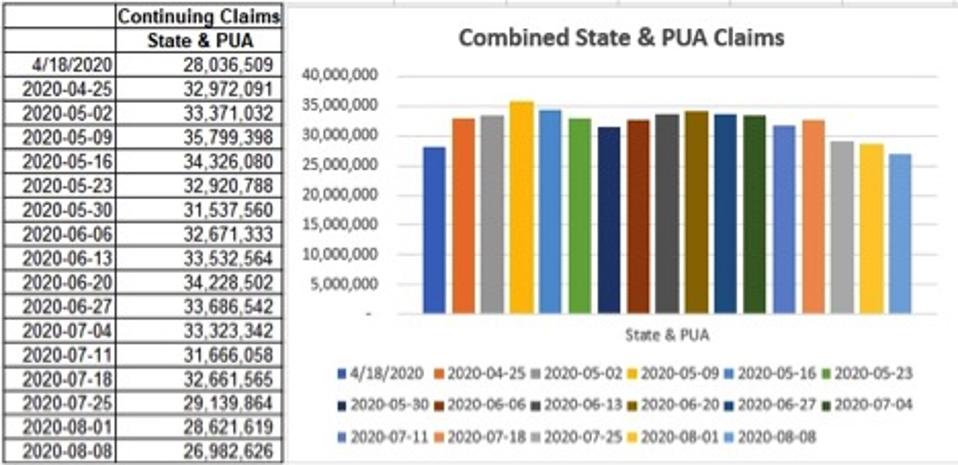

Universal Value Advisors

As shown in the table and graph, the combined programs showed a fall of about -1.6 million (from 28.6 million to 27.0 million). Good progress, but still a long, long way to go!

Conclusions

The worst part of the Recession hasn’t hit yet due to the various and sundry money gifts from Uncle Sam. The virus appears to be heartier than anyone’s (except maybe Dr. Fauci) forecast. Most of Europe is now experiencing upticks in case counts as are some states in the U.S. This may mean a return to “normal” business is still significantly “down the road.” The concept of a “V”-shaped recovery should, by now, be completely debunked.

The Fed’s new policy ensures minuscule interest rates for years. While this, on the surface, appears good for business, it just may not be. For the past 18 months or more, historically low interest rates have created a mountain of debt in corporate America, debt that has kept zombie companies alive. Such debt will be an issue going forward. We already know that corporate America was caught short of liquidity when the pandemic hit, and that caused a surge in bank borrowing and new debt issues. In addition, at the urging of their CFOs, to build up liquidity going forward, the boards of America’s corporations have begun to reduce their future CapEx. That means even slower growth and fewer new future hires.

The Fed’s program of minuscule rates also impacts retirees and those baby-boomers nearing retirement. Their retirement savings, normally invested in safe-haven assets, now must seek more risky assets to throw off enough earnings for the retirees’ expected lifespans.

When uncertainty occurs, as it does every few years, the Fed is now obliged to save the zombie corporations and print more money to support equities. Thus, it isn’t any wonder why the equity market keeps rising despite the historic new heights in risk ratios, like Price/Earnings, and junk bond yield spreads to Treasuries are at historic lows. Under these conditions, how long will it be before the world seeks a different reserve currency?

Maybe, just maybe, the new Fed policy and similar policies for the last 15 years have been ill-designed.

Job seekers owe it to themselves to understand and accept; fundamentally, hiring is a process of elimination. Regardless of how many applications an employer receives, the ratio revolves around several applicants versus one job opening, necessitating elimination.

Essentially, job gatekeepers—recruiters, HR and hiring managers—are paid to find reasons and faults to reject candidates (read: not move forward) to find the candidate most suitable for the job and the company.

Nowadays, employers are inundated with applications, which forces them to double down on reasons to eliminate. It’s no surprise that many job seekers believe that “isms” contribute to their failure to get interviews, let alone get hired. Employers have a large pool of highly qualified candidates to select from. Job seekers attempt to absolve themselves of the consequences of actions and inactions by blaming employers, the government or the economy rather than trying to increase their chances of getting hired by not giving employers reasons to eliminate them because of:

Typos, grammatical errors, poor writing skills.

“Communication, the human connection, is the key to personal and career success.” ― Paul J. Meyer.

The most vital skill you can offer an employer is above-average communication skills. Your resume, LinkedIn profile, cover letters, and social media posts should be well-written and error-free.

Failure to communicate the results you achieved for your previous employers.

If you can’t quantify (e.g. $2.5 million in sales, $300,000 in savings, lowered average delivery time by 6 hours, answered 45-75 calls daily with an average handle time of 3 and a half minutes), then it’s your opinion. Employers care more about your results than your opinion.

An incomplete LinkedIn profile.

Before scheduling an interview, the employer will review your LinkedIn profile to determine if you’re interview-worthy. I eliminate any candidate who doesn’t have a complete LinkedIn profile, including a profile picture, banner, start and end dates, or just a surname initial; anything that suggests the candidate is hiding something.

Having a digital footprint that’s a turnoff.

If an employer is considering your candidacy, you’ll be Google. If you’re not getting interviews before you assert the unfounded, overused excuse, “The hiring system is broken!” look at your digital footprint. Employers are reading your comments, viewing your pictures, etc. Ask yourself, is your digital behaviour acceptable to employers, or can it be a distraction from their brand image and reputation? On the other hand, not having a robust digital footprint is also a red flag, particularly among Gen Y and Gen Z hiring managers. Not participating on LinkedIn, social media platforms, or having a blog or website can hurt your job search.

Not appearing confident when interviewing.

Confidence = fewer annoying questions and a can-do attitude.

It’s important for employers to feel that their new hire is confident in their abilities. Managing an employee who lacks initiative, is unwilling to try new things, or needs constant reassurance is frustrating.

Job searching is a competition; you’re always up against someone younger, hungrier and more skilled than you.

Besides being a process of elimination, hiring is also about mitigating risk. Therefore, being seen as “a risk” is the most common reason candidates are eliminated, with the list of “too risky” being lengthy, from age (will be hard to manage, won’t be around long) to lengthy employment gaps (raises concerns about your abilities and ambition) to inappropriate social media postings (lack of judgement).

Envision you’re a hiring manager hiring for an inside sales manager role. In the absence of “all things being equal,” who’s the least risky candidate, the one who:

offers empirical evidence of their sales results for previous employers, or the candidate who “talks a good talk”?

is energetic, or the candidate who’s subdued?

asks pointed questions indicating they’re concerned about what they can offer the employer or the candidate who seems only concerned about what the employer can offer them.

posts on social media platforms, political opinions, or the candidate who doesn’t share their political views?

on LinkedIn and other platforms in criticizes how employers hire or the candidate who offers constructive suggestions?

has lengthy employment gaps, short job tenure, or a steadily employed candidate?

lives 10 minutes from the office or 45 minutes away?

has a resume/LinkedIn profile that shows a relevant linear career or the candidate with a non-linear career?

dressed professionally for the interview, or the candidate who dressed “casually”?

An experienced hiring manager (read: has made hiring mistakes) will lean towards candidates they feel pose the least risk. Hence, presenting yourself as a low-risk candidate is crucial to job search success. Worth noting, the employer determines their level of risk tolerance, not the job seeker, who doesn’t own the business—no skin in the game—and has no insight into the challenges they’ve experienced due to bad hires and are trying to avoid similar mistakes.

“Taking a chance” on a candidate isn’t in an employer’s best interest. What’s in an employer’s best interest is to hire candidates who can hit the ground running, fit in culturally, and are easy to manage. You can reduce the odds (no guarantee) of being eliminated by demonstrating you’re such a candidate.

Nick Kossovan, a well-seasoned veteran of the corporate landscape, offers “unsweetened” job search advice. You can send Nick your questions to artoffindingwork@gmail.com.

Human Resources Officers must be very busy these days what with the general turnover of employees in our retail and business sectors. It is hard enough to find skilled people let alone potential employees willing to be trained. Then after the training, a few weeks go by then they come to you and ask for a raise. You refuse as there simply is no excess money in the budget and away they fly to wherever they come from, trained but not willing to put in the time to achieve that wanted raise.

I have had potentials come in and we give them a test to see if they do indeed know how to weld, polish or work with wood. 2-10 we hire, and one of those is gone in a week or two. Ask that they want overtime, and their laughter leaving the building is loud and unsettling. Housing starts are doing well but way behind because those trades needed to finish a project simply don’t come to the site, with delay after delay. Some people’s attitudes are just too funny. A recent graduate from a Ivy League university came in for an interview. The position was mid-management potential, but when we told them a three month period was needed and then they would make the big bucks they disappeared as fast as they arrived.

Government agencies are really no help, sending us people unsuited or unwilling to carry out the jobs we offer. Handing money over to staffing firms whose referrals are weak and ineffectual. Perhaps with the Fall and Winter upon us, these folks will have to find work and stop playing on the golf course or cottaging away. Tried to hire new arrivals in Canada but it is truly difficult to find someone who has a real identity card and is approved to live and work here. Who do we hire? Several years ago my father’s firm was rocking and rolling with all sorts of work. It was a summer day when the immigration officers arrived and 30+ employees hit the bricks almost immediately. The investigation that followed had threats of fines thrown at us by the officials. Good thing we kept excellent records, photos and digital copies. We had to prove the illegal documents given to us were as good as the real McCoy.

Restauranteurs, builders, manufacturers, finishers, trades-based firms, and warehousing are all suspect in hiring illegals, yet that becomes secondary as Toronto increases its minimum wage again bringing our payroll up another $120,000. Survival in Canada’s financial and business sectors is questionable for many. Good luck Chuck!. at least your carbon tax refund check should be arriving soon.

NORMAN WELLS, N.W.T. – Imperial Oil says it will temporarily reduce its fuel prices in a Northwest Territories community that has seen costs skyrocket due to low water on the Mackenzie River forcing the cancellation of the summer barge resupply season.

Imperial says in a Facebook post it will cut the air transportation portion that’s included in its wholesale price in Norman Wells for diesel fuel, or heating oil, from $3.38 per litre to $1.69 per litre, starting Tuesday.

The air transportation increase, it further states, will be implemented over a longer period.

It says Imperial is closely monitoring how much fuel needs to be airlifted to the Norman Wells area to prevent runouts until the winter road season begins and supplies can be replenished.

Gasoline and heating fuel prices approached $5 a litre at the start of this month.

Norman Wells’ town council declared a local emergency on humanitarian grounds last week as some of its 700 residents said they were facing monthly fuel bills coming to more than $5,000.

“The wholesale price increase that Imperial has applied is strictly to cover the air transportation costs. There is no Imperial profit margin included on the wholesale price. Imperial does not set prices at the retail level,” Imperial’s statement on Monday said.

The statement further said Imperial is working closely with the Northwest Territories government on ways to help residents in the near term.

“Imperial Oil’s decision to lower the price of home heating fuel offers immediate relief to residents facing financial pressures. This step reflects a swift response by Imperial Oil to discussions with the GNWT and will help ease short-term financial burdens on residents,” Caroline Wawzonek, Deputy Premier and Minister of Finance and Infrastructure, said in a news release Monday.

Wawzonek also noted the Territories government has supported the community with implementation of a fund supporting businesses and communities impacted by barge cancellations. She said there have also been increases to the Senior Home Heating Subsidy in Norman Wells, and continued support for heating costs for eligible Income Assistance recipients.

Additionally, she said the government has donated $150,000 to the Norman Wells food bank.

In its declaration of a state of emergency, the town said the mayor and council recognized the recent hike in fuel prices has strained household budgets, raised transportation costs, and affected local businesses.

It added that for the next three months, water and sewer service fees will be waived for all residents and businesses.

This report by The Canadian Press was first published Oct. 21, 2024.