In all the talk of “building back better” and making economies “match fit”, “strategically autonomous” and “resilient”, there is an unstated but tragic premise. For decades, most advanced economies did not build their future but languished in an investment drought, the scandal of which is greater for being unacknowledged.

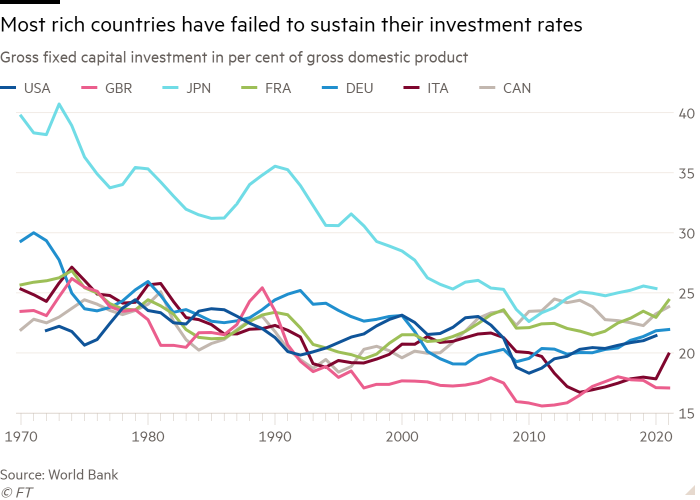

Between 1970 and 1989, the share of gross domestic product devoted to investment by six of the world’s seven biggest economies averaged from 22.6 per cent for the US to 24.8 per cent for Germany. The seventh, Japan, was an outlier with 35 per cent.

Of the G7, only Canada has sustained this level of investment: its 22.5 per cent in this millennium is barely down from 22.8 back then. All the others have only managed to match their 1970-89 investment levels in four instances: the US in the boom years of 2000 and 2005-06, and France in 2021.

Yet these past 20 years have been the era of lower-than-ever financing costs, first because of market exuberance, then thanks to central banks’ ultra-lax monetary policy. And what do we have to show for all that cheap credit? Two lost decades for investment. As economics writer Annie Lowrey concisely puts it, “we blew it”.

France and the US have invested nearly two percentage points of GDP less this century than they did in the 1970s and 1980s; Germany and Italy about 4.5 points less; the UK and Japan 6 and 10 percentage points less respectively. These are enormous numbers. The G7 account for about $45tn in annual GDP. Restoring their investment ratios could fill nearly half the global shortfall to the $4tn the International Energy Agency calls for in annual clean technology investment if we are to meet net zero by 2050.

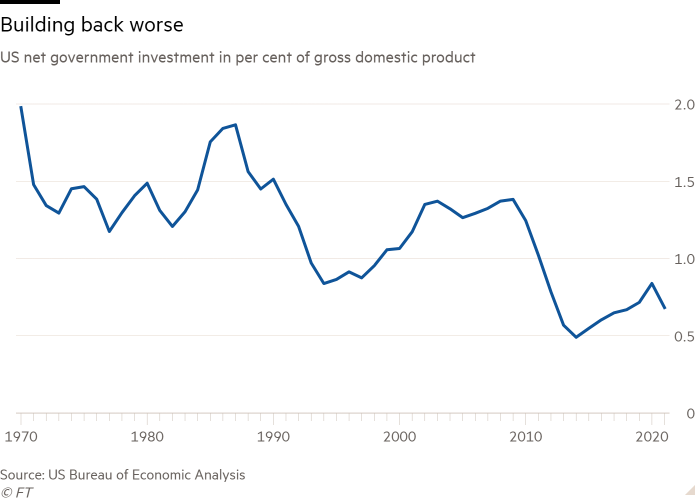

Those are total investment numbers, but a similar story holds for the public sector on its own. In the US, net government investment (after accounting for depreciation of the existing public capital stock) fell by almost two-thirds in the decade to 2014, when it dropped to 0.5 per cent of GDP.

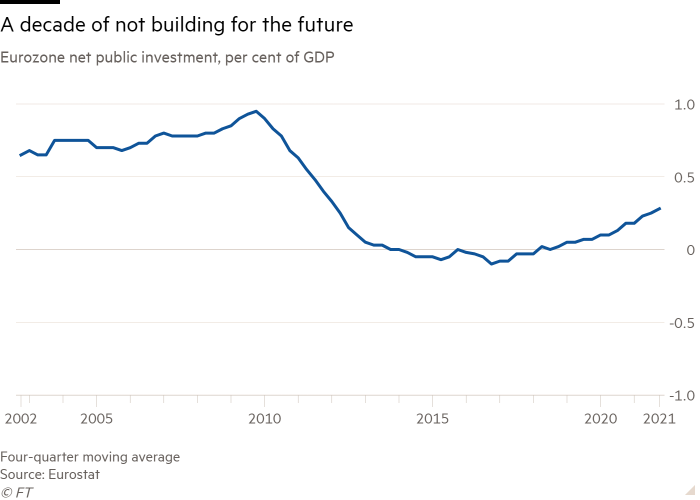

In the eurozone, net public investment went negative in the same year, thanks to extreme fiscal austerity in the eurozone periphery and chronic under-investment in Germany.

Some will be tempted by claims that we need not worry. It is normal to invest less as you get richer — so one argument goes — because adding to an already large capital stock is increasingly useless. The cost of capital goods has fallen, so the same money buys you more real investment, goes another. A third is that the current economy needs intangible, not physical capital, and while this is harder to measure, countries seem to be doing better on that front.

Yet such reassurances, even if factually true, are no use. No one who takes a close look at most western countries’ physical infrastructure can think it fit for purpose — not when that purpose expands to include decarbonising our industries and energy and transport systems.

Why have we lived for so long off past investments and failed to make enough new ones? Financing costs have clearly not been the problem, with interest rates at record lows. (Crisis-hit eurozone countries in the sovereign debt crisis were the exception, but even Spain and Italy have out-invested Britain for decades.)

More likely culprits are a lack of demand and cheap labour. Businesses that don’t expect enough demand to absorb expanded output have no reason to invest. And when they are permitted to treat workers as cheap and disposable, they may choose that over irreversible capital investments. This is why faster wage growth and the so-called “labour shortages” (really competition for workers) are something we should embrace if we are to prod businesses into productive investments.

Something similar may have been true for cheap energy in Europe. The 2010s were a time of unusually low-cost natural gas and hence electricity. This may have undermined the urgency of investing in both greater renewable generation and geopolitically safe natural gas developments. Oil prices, too, were low for much of the decade.

But underneath these economic factors, I think our failure to invest is profoundly political. Raising the investment-to-GDP ratio, whether through boosts to private or public investment, or both, means that a smaller ratio of GDP is left over for consumption. Even if this prepares a better future, it can feel like a measlier existence today. And that is something a generation of politicians across the rich world have been afraid to inflict on their voters.

That is true in good times, when transfer payments, tax cuts and immediate public goods are all politically more attractive than capital investment. (Something equivalent is at work in the private sector: witness companies’ choice to return cash to owners through share buybacks rather than invest in their own growth.) It has also been true in bad times, when investment is the easiest expenditure for belt-tightening governments and companies to cut.

European countries have come to rue how they used the “peace dividend” of 1989 to cut defence spending. The same moment pushed the west as a whole to forget the broader idea of short-term sacrifice for a more prosperous future. But this is not inevitable, as exceptions such as Canada and the Nordics’ sustained investment show. Western voters and governments have both unlearned the virtue of delayed gratification. They have to relearn it, and fast.