Negative oil prices, ships dawdling at sea with unwanted cargoes, and traders getting creative about where to stash oil. The next chapter in the oil crisis is now inevitable: great swathes of the petroleum industry are about to start shutting down.

The economic impact of the coronavirus has ripped through the oil industry in dramatic phases. First it destroyed demand as lockdowns shut factories and kept drivers at home. Then storage started filling up and traders resorted to ocean-going tankers to store crude in the hope of better prices ahead.

Now shipping prices are surging to stratospheric levels as the industry runs out of tankers — a sign of just how distorted the market has become.

The specter of production shutdowns — and the impact they will have on jobs, companies, their banks, and local economies — was one of the reasons that spurred world leaders to join forces to cut production in an orderly way. But as the scale of the crisis dwarfed their efforts, failing to stop prices diving below zero last week, shut-downs are now a reality. It’s the worst-case scenario for producers and refiners.

“We are moving into the end-game,” Torbjorn Tornqvist, head of commodity trading giant Gunvor Group Ltd., said in an interview. “Early-to-mid May could be the peak. We are weeks, not months, away from it.”

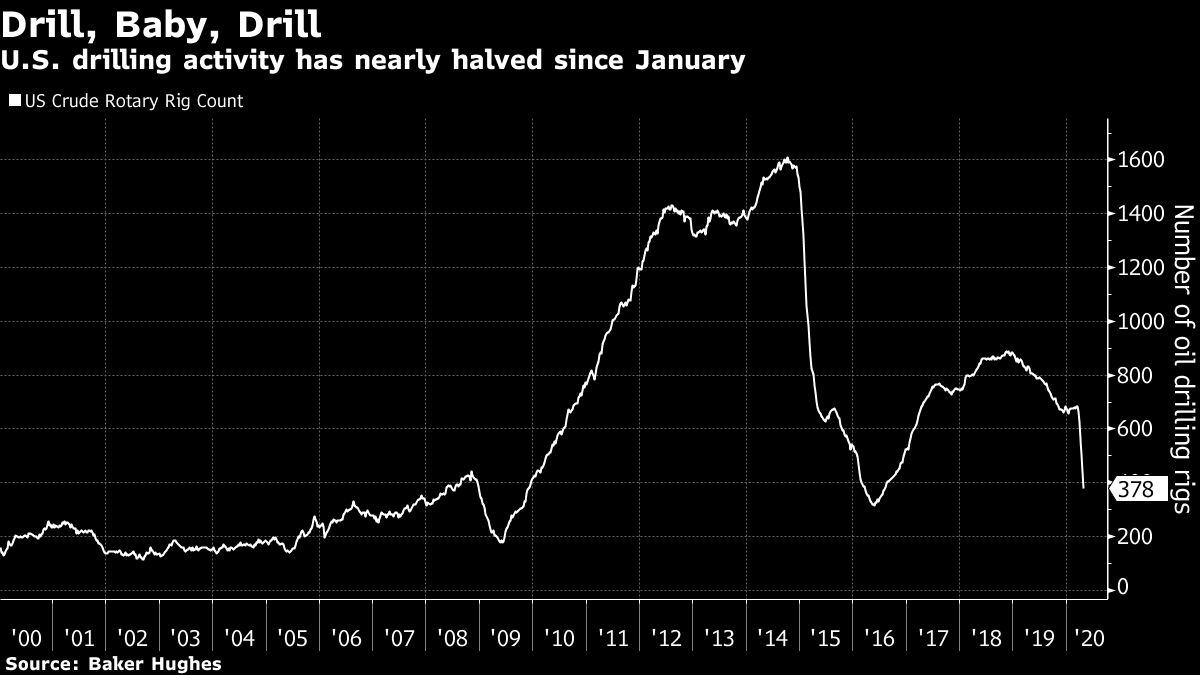

In theory, the first oil output cuts should have come from the OPEC+ alliance, which earlier this month agreed to reduce production from May 1. Yet after the catastrophic price plunge on Monday, when West Texas Intermediate fell to -US$40 a barrel, it’s the U.S. shale patch that is leading.

The best indicator of how the U.S. industry is reacting is the rapid drop in the number of oil rigs in operation, which last week fell to a four-year low. Before the coronavirus crisis hit, oil companies ran about 650 rigs in the U.S. By Friday, more than 40 per cent of them had stopped working, with only 378 left.

“Monday really focused people’s minds that production needs to slow down,” Ben Luckock, co-head of oil trading at commodity merchant Trafigura Group, said. “It’s the smack in the face the market needed to realize this is serious.”

Trafigura, one of the largest exporters of U.S. crude from the U.S. Gulf of Mexico, believes that output in Texas, New Mexico, North Dakota and other states will now fall much faster than expected as companies react to negative prices, which have persisted for several days last week in the physical market.

Until prices collapsed on Monday, the consensus was that output would drop by about 1.5m barrels a day by December. Now market watchers now see that loss by late June. “The severity of the price pressure is likely to act as a catalyst for the immediate turndown in activity and shut-ins,” said Roger Diwan, oil analyst at consultant IHS Markit Ltd.

The price shock has been particularly intense in the physical market: producers of crude streams such as South Texas Sour and Eastern Kansas Common had to pay more than US$50 a barrel to offload their output last week. ConocoPhillips and shale producer Continental Resources Inc. have all announced plans to shut in output. Regulators in Oklahoma voted to allow oil drillers to shut wells without losing leases; New Mexico made a similar decision.

North Dakota, which for years was synonymous with the U.S. shale revolution, is witnessing a rapid retrenchment. Oil producers have already closed more than 6,000 wells, curtailing about 405,000 barrels a day in production, or about 30 per cent of the state’s total.

The output cuts won’t be limited to the U.S. From Chad, a poor and landlocked country in Africa, to Vietnam and Brazil, producers are now either reducing output or making plans to do so.

“I wouldn’t want to get sensational about it but yes, clearly there must be a risk of shut-ins,” Mitch Flegg, the head of North Sea oil company Serica Energy, said in an interview. “In certain parts of the world it is a real and present risk.”

In emergency board meetings last week, oil companies small and large discussed an outlook that’s the most somber any oil executive has ever witnessed. For the small firms, the next few weeks will be all about staying afloat. But even for the bigger ones, like Exxon Mobil Corp. and BP Plc, it’s a challenge. Big Oil will offer an insight into the crisis when companies report earnings this week.

Saudi Arabia, Russia and the rest of the OPEC+ alliance will join the output cuts on Friday, slashing their output by more than 20 per cent, or 9.7 million barrels a day. Saudi Aramco, the state-owned company, is already trimming to reach the target. And Russian oil companies have announced exports of their flagship Urals crude would drop in May to a 10-year low.

Even so, it may not be enough. Every week, 50 million barrels of crude are going into storage, enough to fuel Germany, France, Italy, Spain, and the U.K. combined. At that rate, the world will run out of storage by June. What’s not stored onshore, is stashed in tankers. The U.S. Coast Guard on Friday said there were so many tankers at anchor off California that it was keeping an eye on the situation.

Before the crisis hit, the world was consuming about 100 million barrels a day. Demand now, however, is somewhere between 65 and 70 million barrels. So, in a worst-case scenario, about a third of global output needs to be shut.

The reality is likely to be less severe as storage would continue to bridge the gap between supply and demand. Plus, oil traders say consumption has probably hit a bottom, and will start a very gentle recovery.

Refiners Shut

But before that takes hold, the great shutdown will spread through oil refining too.

Over the past week, Marathon Petroleum Corp., one of the biggest U.S. refiners, announced it would stop production at a plant near San Francisco. Royal Dutch Shell Plc has idled several units in three U.S. refineries in Alabama and Louisiana. And across Europe and Asia, many refineries are running at half rate. U.S. oil refiners processed just 12.45 million barrels a day on the week to April 17, the lowest amount in at least 30 years, except for hurricane-related closures.

More refinery shutdowns are coming, oil traders and consultants said, particularly in the U.S. where lockdowns started later than in Europe and demand is still contracting. Steve Sawyer, director of refining at Facts Global Energy, said that global refineries could halt as much as 25 per cent of total capacity in May.

“No one is going to be able to dodge this bullet.”

TOKYO (AP) — Japanese technology group SoftBank swung back to profitability in the July-September quarter, boosted by positive results in its Vision Fund investments.

Tokyo-based SoftBank Group Corp. reported Tuesday a fiscal second quarter profit of nearly 1.18 trillion yen ($7.7 billion), compared with a 931 billion yen loss in the year-earlier period.

Quarterly sales edged up about 6% to nearly 1.77 trillion yen ($11.5 billion).

SoftBank credited income from royalties and licensing related to its holdings in Arm, a computer chip-designing company, whose business spans smartphones, data centers, networking equipment, automotive, consumer electronic devices, and AI applications.

The results were also helped by the absence of losses related to SoftBank’s investment in office-space sharing venture WeWork, which hit the previous fiscal year.

WeWork, which filed for Chapter 11 bankruptcy protection in 2023, emerged from Chapter 11 in June.

SoftBank has benefitted in recent months from rising share prices in some investment, such as U.S.-based e-commerce company Coupang, Chinese mobility provider DiDi Global and Bytedance, the Chinese developer of TikTok.

SoftBank’s financial results tend to swing wildly, partly because of its sprawling investment portfolio that includes search engine Yahoo, Chinese retailer Alibaba, and artificial intelligence company Nvidia.

SoftBank makes investments in a variety of companies that it groups together in a series of Vision Funds.

The company’s founder, Masayoshi Son, is a pioneer in technology investment in Japan. SoftBank Group does not give earnings forecasts.

Shopify Inc. executives brushed off concerns that incoming U.S. President Donald Trump will be a major detriment to many of the company’s merchants.

“There’s nothing in what we’ve heard from Trump, nor would there have been anything from (Democratic candidate) Kamala (Harris), which we think impacts the overall state of new business formation and entrepreneurship,” Shopify’s chief financial officer Jeff Hoffmeister told analysts on a call Tuesday.

“We still feel really good about all the merchants out there, all the entrepreneurs that want to start new businesses and that’s obviously not going to change with the administration.”

Hoffmeister’s comments come a week after Trump, a Republican businessman, trounced Harris in an election that will soon return him to the Oval Office.

On the campaign trail, he threatened to impose tariffs of 60 per cent on imports from China and roughly 10 per cent to 20 per cent on goods from all other countries.

If the president-elect makes good on the promise, many worry the cost of operating will soar for companies, including customers of Shopify, which sells e-commerce software to small businesses but also brands as big as Kylie Cosmetics and Victoria’s Secret.

These merchants may feel they have no choice but to pass on the increases to customers, perhaps sparking more inflation.

If Trump’s tariffs do come to fruition, Shopify’s president Harley Finkelstein pointed out China is “not a huge area” for Shopify.

However, “we can’t anticipate what every presidential administration is going to do,” he cautioned.

He likened the uncertainty facing the business community to the COVID-19 pandemic where Shopify had to help companies migrate online.

“Our job is no matter what comes the way of our merchants, we provide them with tools and service and support for them to navigate it really well,” he said.

Finkelstein was questioned about the forthcoming U.S. leadership change on a call meant to delve into Shopify’s latest earnings, which sent shares soaring 27 per cent to $158.63 shortly after Tuesday’s market open.

The Ottawa-based company, which keeps its books in U.S. dollars, reported US$828 million in net income for its third quarter, up from US$718 million in the same quarter last year, as its revenue rose 26 per cent.

Revenue for the period ended Sept. 30 totalled US$2.16 billion, up from US$1.71 billion a year earlier.

Subscription solutions revenue reached US$610 million, up from US$486 million in the same quarter last year.

Merchant solutions revenue amounted to US$1.55 billion, up from US$1.23 billion.

Shopify’s net income excluding the impact of equity investments totalled US$344 million for the quarter, up from US$173 million in the same quarter last year.

Daniel Chan, a TD Cowen analyst, said the results show Shopify has a leadership position in the e-commerce world and “a continued ability to gain market share.”

In its outlook for its fourth quarter of 2024, the company said it expects revenue to grow at a mid-to-high-twenties percentage rate on a year-over-year basis.

“Q4 guidance suggests Shopify will finish the year strong, with better-than-expected revenue growth and operating margin,” Chan pointed out in a note to investors.

This report by The Canadian Press was first published Nov. 12, 2024.

TORONTO – RioCan Real Estate Investment Trust says it has cut almost 10 per cent of its staff as it deals with a slowdown in the condo market and overall pushes for greater efficiency.

The company says the cuts, which amount to around 60 employees based on its last annual filing, will mean about $9 million in restructuring charges and should translate to about $8 million in annualized cash savings.

The job cuts come as RioCan and others scale back condo development plans as the market softens, but chief executive Jonathan Gitlin says the reductions were from a companywide efficiency effort.

RioCan says it doesn’t plan to start any new construction of mixed-use properties this year and well into 2025 as it adjusts to the shifting market demand.

The company reported a net income of $96.9 million in the third quarter, up from a loss of $73.5 million last year, as it saw a $159 million boost from a favourable change in the fair value of investment properties.

RioCan reported what it says is a record-breaking 97.8 per cent occupancy rate in the quarter including retail committed occupancy of 98.6 per cent.

This report by The Canadian Press was first published Nov. 12, 2024.