Real eState

The quick rise and public fall of Vancouver’s Coromandel Properties

But now, Coromandel finds itself under scrutiny and the talk of the town. Its recent petition to B.C. Supreme Court seeking creditor protection reveals a pattern of high levels of leverage and repeated borrowing to hold onto properties while failing to develop them quickly enough.

The company has declared it is in financial trouble with $700 million in outstanding debts on 16 prime Vancouver properties, most of which are potential development sites. It is seeking relief under the Companies’ Creditors Arrangement Act, seeking time for the company to be restructured.

Coromandel’s creditor protection application was delayed in a B.C. Supreme Court hearing on Thursday, around the same time hundreds of real estate industry professionals were gathered three blocks away in a hotel ballroom to hear Vancouver Mayor Ken Sim speak at an event hosted by the Urban Development Institute (UDI).

It’s a fall from grace for a company that grew relatively quickly to amass a portfolio of 16 prime Vancouver properties. Coromandel’s petition pegs the combined appraised value of those sites, based on their existing use or Coromandel’s plans for them, at more than $1 billion.

Coromandel Properties began as CM Bay Properties. In 2014, the company paid $15.8 million for a former gas station site near Oakridge Centre that was notable for a proposal to build a mixed-use condo and retail complex in what media reports at the time described as a record-setting per buildable-square-foot price.

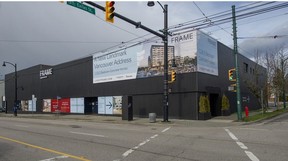

In 2015, it moved into offices on the 18th floor of a building on West Georgia Street in downtown Vancouver and announced it would be known as Coromandel Properties, putting forth Jerry Zhong, also known as Zhen Yu Zhong, as its principal.

The company now leases 12,000 square feet of space in the Georgia Street office tower for $19,892 a month, according to a list of assets and liabilities included in the court petition.

In the following years, Coromandel continued to add to its portfolio. The petition outlines the company’s vision for several of these sites, including tall towers combining hotels, offices, condos and apartments. But figures in the development industry say the company has, to date, completed a limited number of relatively modest projects.

Earlier this month, Coromandel’s website listed nine “future development” projects, four in various stages of development, and only two completed projects.

“I would call them a small developer with unusually large land holdings. They’re a small developer, both in terms of their past track record and overall amount of property under development,” said Jon Stovell, who has been in the Metro Vancouver real estate development industry for more than 25 years and is chair of the UDI and president of Reliance Properties.

“It’s fair to say it’s a significant event. Everybody is keeping an eye on to see how it sorts itself out. It’s primarily a function of a very, very, very rapid increase in interest rates … and not surprising that some developer, maybe, is caught on the wrong side of that, just the way that their capital is structured,” said Stovell.

Ronn Rapp, CEO of the Homebuilders Association Vancouver, put it this way: “Everyone has to start somewhere, but the order of magnitude in this case is unusual.”

Typically, developers want to sequence their projects “to drive a more evenly balanced cash flow position,” Rapp said, with some projects in early stages while others are under construction and others are completed and driving revenue.

In July 2015, Zhong explained in a news release that his company’s new name, Coromandel, was “derived from the valuable screens that were created in China and shipped all over the world via the Coromandel Coast of southern India. We chose (the name) to honour the heritage of our company’s principals who travelled from China to make Canada their home.”

But there were also much smaller companies, backed by a mix of money from B.C., other Canadian provinces and overseas that were jumping into the market to assemble residential land and buy commercial sites in various part of Metro Vancouver.

Coromandel was one of several of these. Some local developers were critical of the way these newer companies seemed to be buying prime lots at top dollar with no pressing plans to develop them. Academics and observers said it wasn’t the first time inflated real estate prices were being blamed on investors and immigrants from Asia, pointing back to the 1980s and 1990s-era exodus of people and money from Hong Kong to Vancouver.

Instead, the company threw its support behind popular events like the Vancouver Cherry Blossom Festival and charitable causes such as the Vancouver Sun’s Adopt-A-School program. At the Vancouver Art Gallery, it joined some of the city’s high profile entrepreneurs, such as Artizia founder Brian Hill, as well as big corporate names, such as BMO and TD, in being a lead sponsor and backer of major exhibits, including Claude Monet’s Secret Garden and Takashi Murakami’s The Octopus Eats Its Own Leg.

In one of the few public photos of Zhong, he is pictured at the opening of the Murakami exhibit standing with a big cheerful smile next to the Japanese pop artist.

Like many other more established developers, Coromandel and Zhong also threw money into political contributions. Elections B.C. records show that in 2017 alone, Coromandel donated $20,000 to the B.C. NDP and $35,000 to Vision Vancouver. Ahead of the 2018 election, Zhong also donated to Vision and independent candidate Kennedy Stewart.

Zhong attended events and parties, but kept a low-profile in the media.

Stovell said he does not personally know Zhong, but knows Louie from his time on city council, saying “he was a great councillor and did a lot for the city.”

Louie grew up in East Vancouver and his career took him from bundling Vancouver Sun and Province newspapers in the viewless basement of the old Pacific Press building, where he was a union rep, to a key player in Vancouver’s city council chamber, to Coromandel’s board rooms.

Louie was first elected to Vancouver council in 2002 representing COPE, as the left-leaning, union-backed party swept to power. He was part of the split from COPE which produced the more centrist Vision Vancouver, the party with which he was re-elected to council in 2005, 2008, 2011 and 2014.

Coromandel didn’t make Louie and Zhong available for an interview, and declined to answer questions by email.

John Nicola, CEO of Nicola Wealth, said his company bought Coromandel out of a joint venture earlier this year to build two apartment towers on a site near Oakridge.

“They, at the time, needed a liquidity event,” Nicola said. “They had obviously, in hindsight, pressure from these other projects, and we were committed to going ahead, so therefore we said: ‘OK fine, we are going to continue on our own.’”

— With research from Carolyn Soltau

TORONTO – The Toronto Regional Real Estate Board says home sales in October surged as buyers continued moving off the sidelines amid lower interest rates.

The board said 6,658 homes changed hands last month in the Greater Toronto Area, up 44.4 per cent compared with 4,611 in the same month last year. Sales were up 14 per cent from September on a seasonally adjusted basis.

The average selling price was up 1.1 per cent compared with a year earlier at $1,135,215. The composite benchmark price, meant to represent the typical home, was down 3.3 per cent year-over-year.

“While we are still early in the Bank of Canada’s rate cutting cycle, it definitely does appear that an increasing number of buyers moved off the sidelines and back into the marketplace in October,” said TRREB president Jennifer Pearce in a news release.

“The positive affordability picture brought about by lower borrowing costs and relatively flat home prices prompted this improvement in market activity.”

The Bank of Canada has slashed its key interest rate four times since June, including a half-percentage point cut on Oct. 23. The rate now stands at 3.75 per cent, down from the high of five per cent that deterred many would-be buyers from the housing market.

New listings last month totalled 15,328, up 4.3 per cent from a year earlier.

In the City of Toronto, there were 2,509 sales last month, a 37.6 per cent jump from October 2023. Throughout the rest of the GTA, home sales rose 48.9 per cent to 4,149.

The sales uptick is encouraging, said Cameron Forbes, general manager and broker for Re/Max Realtron Realty Inc., who added the figures for October were stronger than he anticipated.

“I thought they’d be up for sure, but not necessarily that much,” said Forbes.

“Obviously, the 50 basis points was certainly a great move in the right direction. I just thought it would take more to get things going.”

He said it shows confidence in the market is returning faster than expected, especially among existing homeowners looking for a new property.

“The average consumer who’s employed and may have been able to get some increases in their wages over the last little bit to make up some ground with inflation, I think they’re confident, so they’re looking in the market.

“The conditions are nice because you’ve got a little more time, you’ve got more choice, you’ve got fewer other buyers to compete against.”

All property types saw more sales in October compared with a year ago throughout the GTA.

Townhouses led the surge with 56.8 per cent more sales, followed by detached homes at 46.6 per cent and semi-detached homes at 44 per cent. There were 33.4 per cent more condos that changed hands year-over-year.

“Market conditions did tighten in October, but there is still a lot of inventory and therefore choice for homebuyers,” said TRREB chief market analyst Jason Mercer.

“This choice will keep home price growth moderate over the next few months. However, as inventory is absorbed and home construction continues to lag population growth, selling price growth will accelerate, likely as we move through the spring of 2025.”

This report by The Canadian Press was first published Nov. 6, 2024.

The Canadian Press. All rights reserved.

HALIFAX – A village of tiny homes is set to open next month in a Halifax suburb, the latest project by the provincial government to address homelessness.

Located in Lower Sackville, N.S., the tiny home community will house up to 34 people when the first 26 units open Nov. 4.

Another 35 people are scheduled to move in when construction on another 29 units should be complete in December, under a partnership between the province, the Halifax Regional Municipality, United Way Halifax, The Shaw Group and Dexter Construction.

The province invested $9.4 million to build the village and will contribute $935,000 annually for operating costs.

Residents have been chosen from a list of people experiencing homelessness maintained by the Affordable Housing Association of Nova Scotia.

They will pay rent that is tied to their income for a unit that is fully furnished with a private bathroom, shower and a kitchen equipped with a cooktop, small fridge and microwave.

The Atlantic Community Shelters Society will also provide support to residents, ranging from counselling and mental health supports to employment and educational services.

This report by The Canadian Press was first published Oct. 24, 2024.

The Canadian Press. All rights reserved.

Housing affordability is a key issue in the provincial election campaign in British Columbia, particularly in major centres.

Here are some statistics about housing in B.C. from the Canada Mortgage and Housing Corporation’s 2024 Rental Market Report, issued in January, and the B.C. Real Estate Association’s August 2024 report.

Average residential home price in B.C.: $938,500

Average price in greater Vancouver (2024 year to date): $1,304,438

Average price in greater Victoria (2024 year to date): $979,103

Average price in the Okanagan (2024 year to date): $748,015

Average two-bedroom purpose-built rental in Vancouver: $2,181

Average two-bedroom purpose-built rental in Victoria: $1,839

Average two-bedroom purpose-built rental in Canada: $1,359

Rental vacancy rate in Vancouver: 0.9 per cent

How much more do new renters in Vancouver pay compared with renters who have occupied their home for at least a year: 27 per cent

This report by The Canadian Press was first published Oct. 17, 2024.

The Canadian Press. All rights reserved.

Canada’s Denis Shapovalov wins Belgrade Open for his second ATP Tour title

Talks to resume in B.C. port dispute in bid to end multi-day lockout

The Royal Canadian Legion turns to Amazon for annual poppy campaign boost

dynaCERT Inc. Invites You to Join Us at the Vancouver Resource Investment Conference | INN – Investing News Network

AP source: Bears acquiring quarterback Nick Foles from Jaguars – Sportsnet.ca

12 Bizarre Things People Did Just To Make Social Media Content

-

News9 hours ago

News9 hours agoAffordability or bust: Nova Scotia election campaign all about cost of living

-

News9 hours ago

News9 hours agoCanada’s Denis Shapovalov wins Belgrade Open for his second ATP Tour title

-

News9 hours ago

News9 hours ago11 new cases of measles confirmed in New Brunswick, bringing total cases to 25

-

News9 hours ago

News9 hours agoFirst World War airmen from New Brunswick were pioneers of air warfare

-

News9 hours ago

News9 hours agoTalks to resume in B.C. port dispute in bid to end multi-day lockout

-

News9 hours ago

News9 hours agoMuseum to honour Chinese Canadian troops who fought in war and for citizenship rights

-

News9 hours ago

News9 hours agoThe Royal Canadian Legion turns to Amazon for annual poppy campaign boost