This article comes to us courtesy of EVANNEX, which makes and sells aftermarket Tesla accessories. The opinions expressed therein are not necessarily our own at InsideEVs, nor have we been paid by EVANNEX to publish these articles. We find the company’s perspective as an aftermarket supplier of Tesla accessories interesting and are willing to share its content free of charge. Enjoy!

Posted on EVANNEX on July 24, 2020 by Charles Morris

As stock-market pundits tie themselves in knots trying to explain how Tesla became the world’s most valuable automaker in the space of a few short years, it may be worth repeating a few basic principles from Investing 101.

One of those rudimentary rules is that the stock market is forward-looking. A company’s stock price doesn’t reflect what the company did last quarter, but rather what the market thinks it will be doing a year or multiple years into the future. Investing is about making educated guesses about what the future will look like, and predicting which firms are in position to thrive in that future, and which are likely to be left behind. If you accept that the future of the auto industry is electric (and almost every auto industry CEO does, or claims to), then it’s pretty much a no-brainer to bet on Tesla.

Professor Bradford Cornell has been harping on this theme over the course of several columns about Tesla. His latest piece, which appeared in ValueWalk, summarizes some of his past arguments in an eloquent explanation of why TSLA stock is continuing its ascent into orbit, while shares in the legacy automakers remain earthbound.

For years now, we’ve been hearing about a wave of “Tesla killers” soon to come from the legacy automakers, but that wave never seems to arrive. I’ve driven most of the EV offerings out there, and some of them are excellent automobiles, but none can beat what Tesla has to offer, and so far, none are being sold in any real volume.

For Professor Cornell, a successful EV needs to check four boxes: it needs stylish design, plenty of range, and a reasonable price, and it needs to be available in quantity. Only the Tesla Model 3 and Model Y check all four boxes. The Bolt, the LEAF, the i3, the I-PACE, the e-tron, the Taycan, and even new offerings such as the Polestar—all of them lack at least one of these qualities.

We keep hearing about great new EVs in the pipeline, but these keep getting delayed. The Mercedes EQC 400 luxury SUV, originally scheduled to go on sale in the US this year, won’t arrive until 2021. Volkswagen’s ID.4 and Ford’s Mach E are also at least a year away, and Toyota is still nattering about hydrogen.

These are all familiar themes that have been discussed often in this space and others for the last couple of years. It’s plain that time is not on side of the legacy auto brands. However, Professor Cornell calls attention to an aspect of the situation that hasn’t received much discussion: the longer the old boys (and one gal) assume a wait-and-see posture, the more trouble they’re going to have raising capital relative to Tesla, and this could give the whippersnapper an insurmountable competitive advantage.

Tesla’s sky-high stock price gives it access to plenty of capital. And it’s using that capital to build new factories, to develop new models and new features, and to continuously improve its production technology.

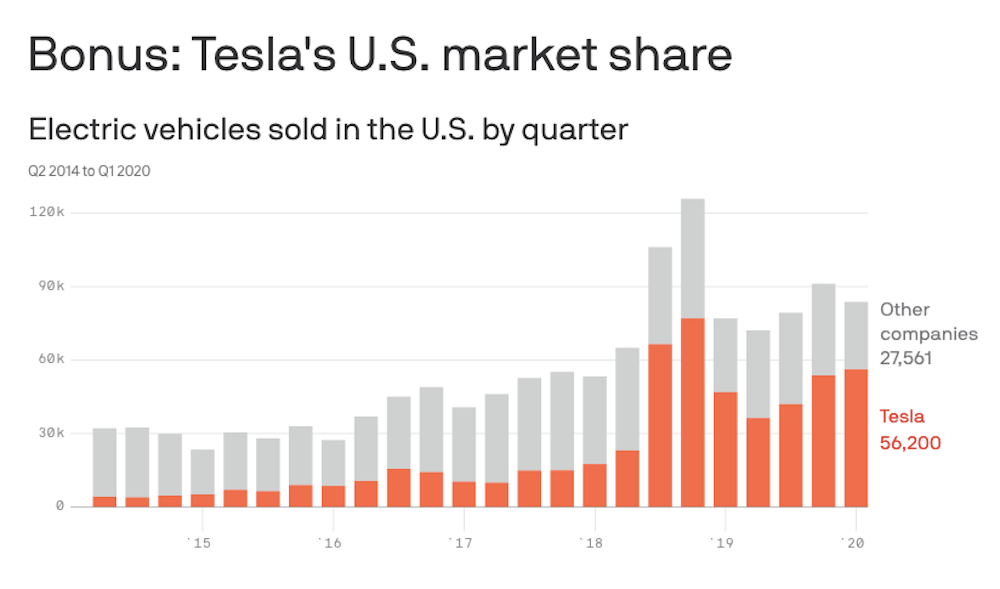

Above: Tesla currently sells the lion’s share of electric vehicles in the U.S. and it’s been growing its market share over the past year (Source: Axios)

Don’t the auto giants have access to lots of capital, too? Of course. But unlike Tesla, they aren’t devoting all, or even most, of their investment to EVs. They have existing product lines to keep alive, networks of dealerships to keep happy, and now, an economy-killing pandemic to fight.

Audi’s CEO just proclaimed that ICE vehicles “will be alive for a very long time,” and that the company will “continue to invest massively in the development of combustion engines.”

The German magazine Auto motor und sport (via CleanTechnica) reports that the sales department at VW has been fighting against the company’s focus on electric cars. CEO Herbert Diess wanted to replace existing ICE versions of the tiny Up! city car and the Passat luxury sedan with electric models, but dealers nixed both moves, so the gas-burning versions of both cars will live on, and continue to consume capital.

It’s becoming clear that EV sales (which pretty much means Tesla sales) are going to take much less of a hit from the COVID-related economic turmoil than ICE vehicles. In the second quarter of this year, Tesla’s deliveries were 90,650, only slightly lower than Q2 2019’s figure of 95,200. GM, Toyota, Fiat Chrysler, Ford and Audi all saw their deliveries drop more than 30% in Q2.

These three real-world examples illustrate three unproductive pursuits (there are others) to which the legacy automakers are forced to direct much of their attention (and money), while Tesla is investing in the future.

To return to Professor Cornell’s four criteria for a successful EV, I think #4, widespread availability, is likely to be the most problematic for the old guard, unless they change their strategies. Yes, Big Auto is investing what seems like big money in electrification, but their plans are still too timid to take on Tesla. GM and Ford collectively plan to produce about 325,000 electric vehicles in 2026. Tesla produced over 367,000 electric vehicles in 2019.

As Cornell sums it up, “If the competitors do not start making interesting, reasonably priced, electric cars at scale, they may face the same fate as retailers who did not respond quickly to Amazon.”

MONTREAL – Travel company Transat AT Inc. reported a loss in its latest quarter compared with a profit a year earlier as its revenue edged lower.

The parent company of Air Transat says it lost $39.9 million or $1.03 per diluted share in its quarter ended July 31.

The result compared with a profit of $57.3 million or $1.49 per diluted share a year earlier.

Revenue in what was the company’s third quarter totalled $736.2 million, down from $746.3 million in the same quarter last year.

On an adjusted basis, Transat says it lost $1.10 per share in its latest quarter compared with an adjusted profit of $1.10 per share a year earlier.

Transat chief executive Annick Guérard says demand for leisure travel remains healthy, as evidenced by higher traffic, but consumers are increasingly price conscious given the current economic uncertainty.

This report by The Canadian Press was first published Sept. 12, 2024.

Dollarama Inc.’s food aisles may have expanded far beyond sweet treats or piles of gum by the checkout counter in recent years, but its chief executive maintains his company is “not in the grocery business,” even if it’s keeping an eye on the sector.

“It’s just one small part of our store,” Neil Rossy told analysts on a Wednesday call, where he was questioned about the company’s food merchandise and rivals playing in the same space.

“We will keep an eye on all retailers — like all retailers keep an eye on us — to make sure that we’re competitive and we understand what’s out there.”

Over the last decade and as consumers have more recently sought deals, Dollarama’s food merchandise has expanded to include bread and pantry staples like cereal, rice and pasta sold at prices on par or below supermarkets.

However, the competition in the discount segment of the market Dollarama operates in intensified recently when the country’s biggest grocery chain began piloting a new ultra-discount store.

The No Name stores being tested by Loblaw Cos. Ltd. in Windsor, St. Catharines and Brockville, Ont., are billed as 20 per cent cheaper than discount retail competitors including No Frills. The grocery giant is able to offer such cost savings by relying on a smaller store footprint, fewer chilled products and a hearty range of No Name merchandise.

Though Rossy brushed off notions that his company is a supermarket challenger, grocers aren’t off his radar.

“All retailers in Canada are realistic about the fact that everyone is everyone’s competition on any given item or category,” he said.

Rossy declined to reveal how much of the chain’s sales would overlap with Loblaw or the food category, arguing the vast variety of items Dollarama sells is its strength rather than its grocery products alone.

“What makes Dollarama Dollarama is a very wide assortment of different departments that somewhat represent the old five-and-dime local convenience store,” he said.

The breadth of Dollarama’s offerings helped carry the company to a second-quarter profit of $285.9 million, up from $245.8 million in the same quarter last year as its sales rose 7.4 per cent.

The retailer said Wednesday the profit amounted to $1.02 per diluted share for the 13-week period ended July 28, up from 86 cents per diluted share a year earlier.

The period the quarter covers includes the start of summer, when Rossy said the weather was “terrible.”

“The weather got slightly better towards the end of the summer and our sales certainly increased, but not enough to make up for the season’s horrible start,” he said.

Sales totalled $1.56 billion for the quarter, up from $1.46 billion in the same quarter last year.

Comparable store sales, a key metric for retailers, increased 4.7 per cent, while the average transaction was down2.2 per cent and traffic was up seven per cent, RBC analyst Irene Nattel pointed out.

She told investors in a note that the numbers reflect “solid demand as cautious consumers focus on core consumables and everyday essentials.”

Analysts have attributed such behaviour to interest rates that have been slow to drop and high prices of key consumer goods, which are weighing on household budgets.

To cope, many Canadians have spent more time seeking deals, trading down to more affordable brands and forgoing small luxuries they would treat themselves to in better economic times.

“When people feel squeezed, they tend to shy away from discretionary, focus on the basics,” Rossy said. “When people are feeling good about their wallet, they tend to be more lax about the basics and more willing to spend on discretionary.”

The current economic situation has drawn in not just the average Canadian looking to save a buck or two, but also wealthier consumers.

“When the entire economy is feeling slightly squeezed, we get more consumers who might not have to or want to shop at a Dollarama generally or who enjoy shopping at a Dollarama but have the luxury of not having to worry about the price in some other store that they happen to be standing in that has those goods,” Rossy said.

“Well, when times are tougher, they’ll consider the extra five minutes to go to the store next door.”

This report by The Canadian Press was first published Sept. 11, 2024.

TORONTO – The U.S. Consumer Financial Protection Bureau has ordered TD Bank Group to pay US$28 million for repeatedly sharing inaccurate, negative information about its customers to consumer reporting companies.

The agency says TD has to pay US$7.76 million in total to tens of thousands of victims of its illegal actions, along with a US$20 million civil penalty.

It says TD shared information that contained systemic errors about credit card and bank deposit accounts to consumer reporting companies, which can include credit reports as well as screening reports for tenants and employees and other background checks.

CFPB director Rohit Chopra says in a statement that TD threatened the consumer reports of customers with fraudulent information then “barely lifted a finger to fix it,” and that regulators will need to “focus major attention” on TD Bank to change its course.

TD says in a statement it self-identified these issues and proactively worked to improve its practices, and that it is committed to delivering on its responsibilities to its customers.

The bank also faces scrutiny in the U.S. over its anti-money laundering program where it expects to pay more than US$3 billion in monetary penalties to resolve.

This report by The Canadian Press was first published Sept. 11, 2024.