Countries by Share of the Global Economy

As 2022 comes to a close we can recap many historic milestones of the year, like the Earth’s population hitting 8 billion and the global economy surpassing $100 trillion.

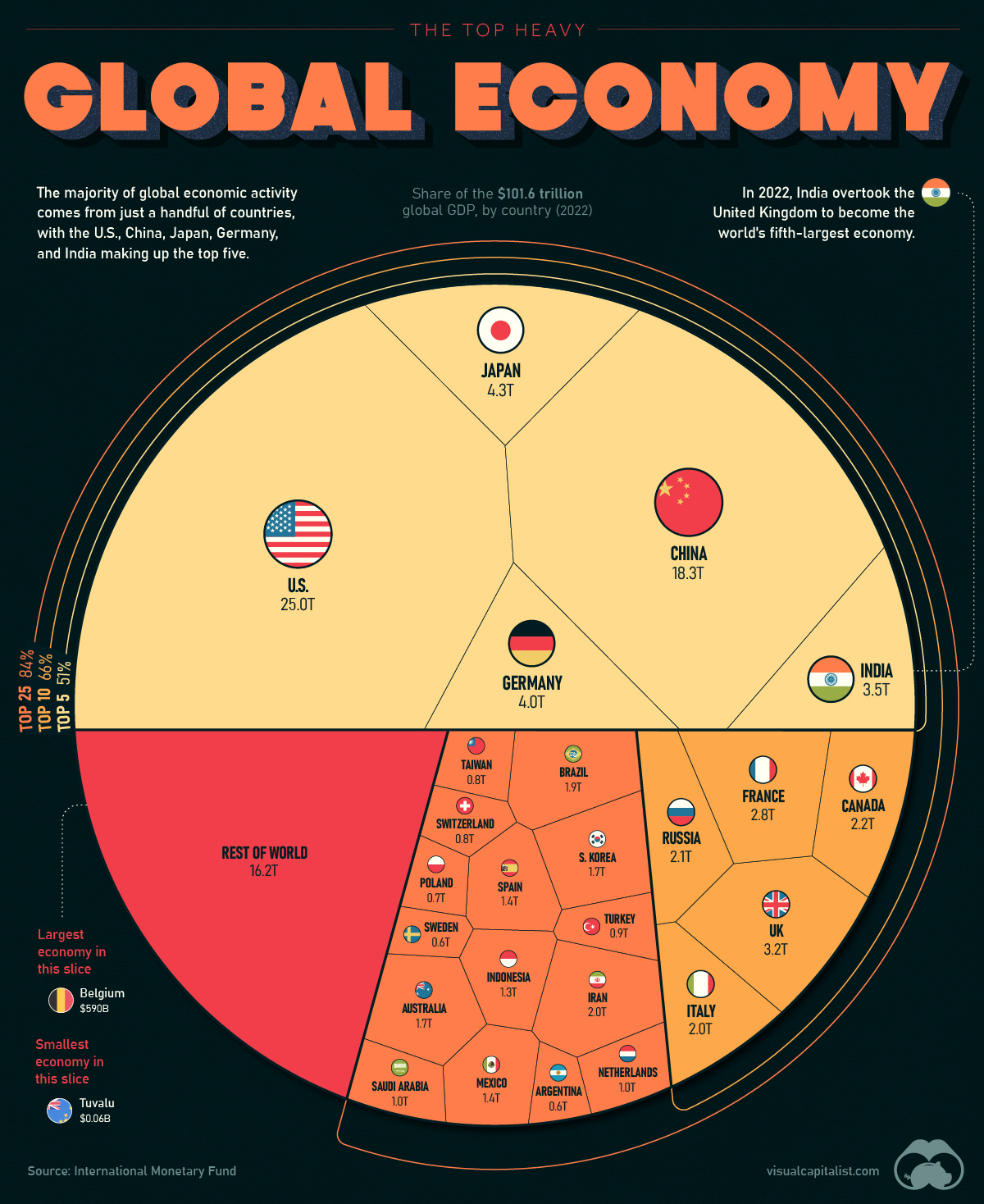

In this chart, we visualize the world’s GDP using data from the IMF, showcasing the biggest economies and the share of global economic activity that they make up.

The GDP Heavyweights

The global economy can be thought of as a pie, with the size of each slice representing the share of the Global Economy GDP contributed by each country. Currently, the largest slices of the pie are held by the United States, China, Japan, Germany, and India, which together account for more than half of global GDP.

Here’s a look at every country’s share of the world’s $101.6 trillion economy:

| Rank | Country | GDP (Billions, USD) |

|---|---|---|

| #1 | ???????? United States | $25,035.2 |

| #2 | ???????? China | $18,321.2 |

| #3 | ???????? Japan | $4,300.6 |

| #4 | ???????? Germany | $4,031.1 |

| #5 | ???????? India | $3,468.6 |

| #6 | ???????? United Kingdom | $3,198.5 |

| #7 | ???????? France | $2,778.1 |

| #8 | ???????? Canada | $2,200.4 |

| #9 | ???????? Russia | $2,133.1 |

| #10 | ???????? Italy | $1,997.0 |

| #11 | ???????? Iran | $1,973.7 |

| #12 | ???????? Brazil | $1,894.7 |

| #13 | ???????? South Korea | $1,734.2 |

| #14 | ???????? Australia | $1,724.8 |

| #15 | ???????? Mexico | $1,424.5 |

| #16 | ???????? Spain | $1,389.9 |

| #17 | ???????? Indonesia | $1,289.4 |

| #18 | ???????? Saudi Arabia | $1,010.6 |

| #19 | ???????? Netherlands | $990.6 |

| #20 | ???????? Turkey | $853.5 |

| #21 | ???????? Taiwan | $828.7 |

| #22 | ???????? Switzerland | $807.4 |

| #23 | ???????? Poland | $716.3 |

| #24 | ???????? Argentina | $630.7 |

| #25 | ???????? Sweden | $603.9 |

| #26 | ???????? Belgium | $589.5 |

| #27 | ???????? Thailand | $534.8 |

| #28 | ???????? Israel | $527.2 |

| #29 | ???????? Ireland | $519.8 |

| #30 | ???????? Norway | $504.7 |

| #31 | ???????? Nigeria | $504.2 |

| #32 | ???????? United Arab Emirates | $503.9 |

| #33 | ???????? Egypt | $469.1 |

| #34 | ???????? Austria | $468.0 |

| #35 | ???????? Bangladesh | $460.8 |

| #36 | ???????? Malaysia | $434.1 |

| #37 | ???????? Singapore | $423.6 |

| #38 | ???????? Vietnam | $413.8 |

| #39 | ???????? South Africa | $411.5 |

| #40 | ???????? Philippines | $401.7 |

| #41 | ???????? Denmark | $386.7 |

| #42 | ???????? Pakistan | $376.5 |

| #43 | ???????? Hong Kong SAR | $368.4 |

| #44 | ???????? Colombia | $342.9 |

| #45 | ???????? Chile | $310.9 |

| #46 | ???????? Romania | $299.9 |

| #47 | ???????? Czech Republic | $295.6 |

| #48 | ???????? Iraq | $282.9 |

| #49 | ???????? Finland | $281.4 |

| #50 | ???????? Portugal | $255.9 |

| #51 | ???????? New Zealand | $242.7 |

| #52 | ???????? Peru | $239.3 |

| #53 | ???????? Kazakhstan | $224.3 |

| #54 | ???????? Greece | $222.0 |

| #55 | ???????? Qatar | $221.4 |

| #56 | ???????? Algeria | $187.2 |

| #57 | ???????? Hungary | $184.7 |

| #58 | ???????? Kuwait | $183.6 |

| #59 | ???????? Morocco | $142.9 |

| #60 | ???????? Angola | $124.8 |

| #61 | ???????? Puerto Rico | $118.7 |

| #62 | ???????? Ecuador | $115.5 |

| #63 | ???????? Kenya | $114.9 |

| #64 | ???????? Slovakia | $112.4 |

| #65 | ???????? Dominican Republic | $112.4 |

| #66 | ???????? Ethiopia | $111.2 |

| #67 | ???????? Oman | $109.0 |

| #68 | ???????? Guatemala | $91.3 |

| #69 | ???????? Bulgaria | $85.0 |

| #70 | ???????? Luxembourg | $82.2 |

| #71 | ???????? Venezuela | $82.1 |

| #72 | ???????? Belarus | $79.7 |

| #73 | ???????? Uzbekistan | $79.1 |

| #74 | ???????? Tanzania | $76.6 |

| #75 | ???????? Ghana | $76.0 |

| #76 | ???????? Turkmenistan | $74.4 |

| #77 | ???????? Sri Lanka | $73.7 |

| #78 | ???????? Uruguay | $71.2 |

| #79 | ???????? Panama | $71.1 |

| #80 | ???????? Azerbaijan | $70.1 |

| #81 | ???????? Croatia | $69.4 |

| #82 | ???????? Côte d’Ivoire | $68.6 |

| #83 | ???????? Costa Rica | $68.5 |

| #84 | ???????? Lithuania | $68.0 |

| #85 | ???????? Democratic Republic of the Congo | $63.9 |

| #86 | ???????? Serbia | $62.7 |

| #87 | ???????? Slovenia | $62.2 |

| #88 | ???????? Myanmar | $59.5 |

| #89 | ???????? Uganda | $48.4 |

| #90 | ???????? Jordan | $48.1 |

| #91 | ???????? Tunisia | $46.3 |

| #92 | ???????? Cameroon | $44.2 |

| #93 | ???????? Bahrain | $43.5 |

| #94 | ???????? Bolivia | $43.4 |

| #95 | ???????? Sudan | $42.8 |

| #96 | ???????? Paraguay | $41.9 |

| #97 | ???????? Libya | $40.8 |

| #98 | ???????? Latvia | $40.6 |

| #99 | ???????? Estonia | $39.1 |

| #100 | ???????? Nepal | $39.0 |

| #101 | ???????? Zimbabwe | $38.3 |

| #102 | ???????? El Salvador | $32.0 |

| #103 | ???????? Papua New Guinea | $31.4 |

| #104 | ???????? Honduras | $30.6 |

| #105 | ???????? Trinidad and Tobago | $29.3 |

| #106 | ???????? Cambodia | $28.3 |

| #107 | ???????? Iceland | $27.7 |

| #108 | ???????? Yemen | $27.6 |

| #109 | ???????? Senegal | $27.5 |

| #110 | ???????? Zambia | $27.0 |

| #111 | ???????? Cyprus | $26.7 |

| #112 | ???????? Georgia | $25.2 |

| #113 | ???????? Bosnia and Herzegovina | $23.7 |

| #114 | ???????? Macao SAR | $23.4 |

| #115 | ???????? Gabon | $22.2 |

| #116 | ???????? Haiti | $20.2 |

| #117 | ???????? Guinea | $19.7 |

| #118 | West Bank and Gaza | $18.8 |

| #119 | ???????? Brunei | $18.5 |

| #120 | ???????? Mali | $18.4 |

| #121 | ???????? Burkina Faso | $18.3 |

| #122 | ???????? Albania | $18.3 |

| #123 | ???????? Botswana | $18.0 |

| #124 | ???????? Mozambique | $17.9 |

| #125 | ???????? Armenia | $17.7 |

| #126 | ???????? Benin | $17.5 |

| #127 | ???????? Malta | $17.2 |

| #128 | ???????? Equatorial Guinea | $16.9 |

| #129 | ???????? Laos | $16.3 |

| #130 | ???????? Jamaica | $16.1 |

| #131 | ???????? Mongolia | $15.7 |

| #132 | ???????? Nicaragua | $15.7 |

| #133 | ???????? Madagascar | $15.1 |

| #134 | ???????? Guyana | $14.8 |

| #135 | ???????? Niger | $14.6 |

| #136 | ???????? Republic of Congo | $14.5 |

| #137 | ???????? North Macedonia | $14.1 |

| #138 | ???????? Moldova | $14.0 |

| #139 | ???????? Chad | $12.9 |

| #140 | ???????? The Bahamas | $12.7 |

| #141 | ???????? Namibia | $12.5 |

| #142 | ???????? Rwanda | $12.1 |

| #143 | ???????? Malawi | $11.6 |

| #144 | ???????? Mauritius | $11.5 |

| #145 | ???????? Mauritania | $10.1 |

| #146 | ???????? Tajikistan | $10.0 |

| #147 | ???????? Kyrgyzstan | $9.8 |

| #148 | ???????? Kosovo | $9.2 |

| #149 | ???????? Somalia | $8.4 |

| #150 | ???????? Togo | $8.4 |

| #151 | ???????? Montenegro | $6.1 |

| #152 | ???????? Maldives | $5.9 |

| #153 | ???????? Barbados | $5.8 |

| #154 | ???????? Fiji | $4.9 |

| #155 | ???????? South Sudan | $4.8 |

| #156 | ???????? Eswatini | $4.7 |

| #157 | ???????? Sierra Leone | $4.1 |

| #158 | ???????? Liberia | $3.9 |

| #159 | ???????? Djibouti | $3.7 |

| #160 | ???????? Burundi | $3.7 |

| #161 | ???????? Aruba | $3.5 |

| #162 | ???????? Andorra | $3.3 |

| #163 | ???????? Suriname | $3.0 |

| #164 | ???????? Bhutan | $2.7 |

| #165 | ???????? Belize | $2.7 |

| #166 | ???????? Lesotho | $2.5 |

| #167 | ???????? Central African Republic | $2.5 |

| #168 | ???????? Timor-Leste | $2.4 |

| #169 | ???????? Eritrea | $2.4 |

| #170 | ???????? The Gambia | $2.1 |

| #171 | ???????? Cabo Verde | $2.1 |

| #172 | ???????? Seychelles | $2.0 |

| #173 | ???????? St. Lucia | $2.0 |

| #174 | ???????? Antigua and Barbuda | $1.7 |

| #175 | ???????? Guinea-Bissau | $1.6 |

| #176 | ???????? San Marino | $1.6 |

| #177 | ???????? Solomon Islands | $1.6 |

| #178 | ???????? Comoros | $1.2 |

| #179 | ???????? Grenada | $1.2 |

| #180 | ???????? St. Kitts and Nevis | $1.1 |

| #181 | ???????? Vanuatu | $1.0 |

| #182 | ???????? St. Vincent and the Grenadines | $1.0 |

| #183 | ???????? Samoa | $0.83 |

| #184 | ???????? Dominica | $0.60 |

| #185 | ???????? São Tomé and Príncipe | $0.51 |

| #186 | ???????? Tonga | $0.50 |

| #187 | ???????? Micronesia | $0.43 |

| #188 | ???????? Marshall Islands | $0.27 |

| #189 | ???????? Palau | $0.23 |

| #190 | ???????? Kiribati | $0.21 |

| #191 | ???????? Nauru | $0.13 |

| #192 | ???????? Tuvalu | $0.06 |

| #193 | ???????? Ukraine | Data not available |

| Total World GDP | $101,559.3 |

Just five countries make up more than half of the world’s entire GDP in 2022: the U.S., China, Japan, India, and Germany. Interestingly, India replaced the UK this year as a top five economy.

Adding on another five countries (the top 10) makes up 66% of the global economy, and the top 25 countries comprise 84% of global GDP.

The World’s Smallest Economies

The rest of the world — the remaining 167 nations — make up 16% of the global GDP. Many of the smallest economies are islands located in Oceania.

Here’s a look at the 20 smallest economies in the world:

| Country | GDP (Billions, USD) |

|---|---|

| ???????? Tuvalu | $0.06 |

| ???????? Nauru | $0.13 |

| ???????? Kiribati | $0.21 |

| ???????? Palau | $0.23 |

| ???????? Marshall Islands | $0.27 |

| ???????? Micronesia | $0.43 |

| ???????? Tonga | $0.50 |

| ???????? São Tomé and Príncipe | $0.51 |

| ???????? Dominica | $0.60 |

| ???????? Samoa | $0.83 |

| ???????? St. Vincent and the Grenadines | $0.95 |

| ???????? Vanuatu | $0.98 |

| ???????? St. Kitts and Nevis | $1.12 |

| ???????? Grenada | $1.19 |

| ???????? Comoros | $1.24 |

| ???????? Solomon Islands | $1.60 |

| ???????? San Marino | $1.62 |

| ???????? Guinea-Bissau | $1.62 |

| ???????? Antigua and Barbuda | $1.69 |

| ???????? St. Lucia | $1.97 |

Tuvalu has the smallest GDP of any country at just $64 million. Tuvalu is one of a dozen nations with a GDP of less than one billion dollars.

The Global Economy in 2023

Heading into 2023, there is much economic uncertainty. Many experts are anticipating a brief recession, although opinions differ on the definition of “brief”.

Some experts believe that China will buck the trend of economic downturn. If this prediction comes true, the country could own an even larger slice of the Global Economy GDP pie in the near future.

Speaking of predictions, we’re creating the ultimate cheatsheet for 2023.

See what hundreds of experts are predicting for 2023 with our Global Forecast Series.