The Federal Reserve looks set to deliver a fourth straight super-sized rate increase with Chair Jerome Powell repeating his resolute message on inflation and opening the door to a downshift — without necessarily pivoting yet.

The Federal Open Market Committee is expected to raise rates by 75 basis points on Wednesday to a range of 3.75 to 4 per cent, the highest level since 2008 as the central bank extends its most aggressive tightening campaign since the 1980s.

The decision will be announced at 2 p.m. in Washington and Powell will hold a press conference 30 minutes later. No fresh Fed forecasts are released at this meeting.

The central bank chief may emphasize policymakers remain steadfast in their inflation fight, while leaving options open for their gathering in mid-December, when markets are split between another big move or a shift to 50 basis points.

In July, his comments were wrongly interpreted by investors as a near-term policy pivot, with markets rallying in response, which eased financial conditions — making it harder for the Fed to curb prices. The chair may want to avoid a misstep, even if he suggests a shift to smaller increases at upcoming meetings.

“They may want to go slower just in the interest of financial stability,” said Julia Coronado, the founder of MacroPolicy Perspectives LLC. “It’s a challenge for messaging because they don’t want to ease financial conditions significantly. They need tight financial conditions to keep cooling the economy off. So he doesn’t want to sound dovish, but he may want to go slower.”

Powell is trying to curb the hottest inflation in 40 years amid criticism he was slow to respond to rising prices last year. The hikes have roiled financial markets as investors worry the Fed could trigger a recession.

What Bloomberg Economics Says…

“Less certain than today’s rate-hike is how Fed Chair Powell will communicate a potential future downshift in the rate-hike pace — the degree of conviction, the risks around hike sizing, and implications for the terminal rate. We expect that he will present a 50-basis-point move as the base case and clarify that a downshift in the pace of rate hikes does not necessarily mean a lower terminal rate.”

— Anna Wong, Andrew Husby and Eliza Winger (economists)

Wednesday’s expected move comes less than a week before midterm elections in the US, where Republicans have made high inflation a top issue and tried to pin blame on President Joe Biden and his party in Congress. Last week, two Democratic senators urged Powell to not cause unnecessary pain by raising rates too high.

Rates

Economists overwhelmingly predict the FOMC will raise 75 basis points, though one is looking for a step down to 50 basis points instead. Investors are close to fully pricing in 75 basis points at this Fed meeting, according to interest-rate futures markets.

The Bank of Canada unexpectedly slowed its pace of interest-rate hikes to a half point last week, though economists noted Canada’s higher share of adjustable-rate mortgages magnify the macroeconomic impact of the central bank’s rate increases.

What Top Banks Expect in November, December

Bank of America: 75 bps

Barclays: 75 bps, 75 bps

Citigroup: 75 bps, 50bps

Deutsche Bank: 75 bps, 75 bps

JPMorgan Chase: 75 bps, 50 bps

Goldman Sachs: 75 bps, 50 bps

Morgan Stanley: 75 bps, 50 bps

Wells Fargo: 75 bps, 50 bps

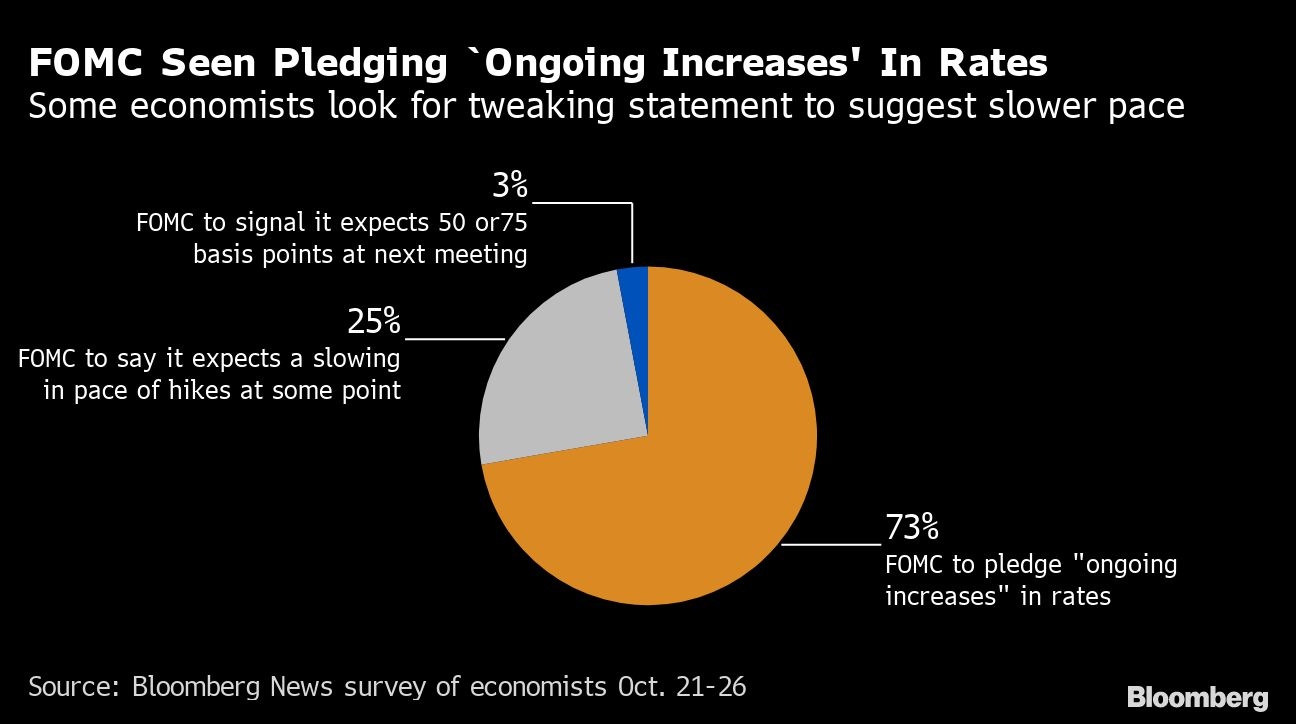

FOMC Statement

The statement is likely to retain its pledge of “ongoing increases” in interest rates, but that could be “modestly tweaked in some way to indicate that you’re closer to the end” of hikes, said Michael Feroli, chief US economist at JPMorgan Chase & Co. One option would be to say “some further increases,” he said.

Press Conference

Powell since July has said it will be necessary to slow the pace of hikes at some point, and he’s likely to reiterate that, while leaving options open in December depending on incoming data. There will be two employment reports and two consumer-price reports before the Dec. 13-14 meeting.

“Markets want some indication that the Fed’s going to downshift,” said Drew Matus, chief market strategist with MetLife Investment Management. “This whole point of downshifting and moving to a slower pace of hikes is because you don’t know how much you have to do. So if it’s raining outside and I am driving, I am slowing down.”

Dissents

About a third of economists expect a dissent at the meeting. The most likely candidates would be Kansas City Fed President Esther George, who dissented in June in favor of a smaller hike, and St. Louis Fed President James Bullard, who dissented in March as a hawk.

Balance Sheet

The Fed is likely to reiterate its plans to shrink its massive balance sheet at a pace of US$1.1 trillion a year. Economists project that will bring the balance sheet to US$8.5 trillion by year end, dropping to US$6.7 trillion in December 2024.

No announcement is expected on sales of mortgage-backed securities.

Financial Stability

A report on financial stability is likely to be presented during the meeting, according to Nomura’s economists, and Powell may be asked whether the pace of hikes and potentially a US recession could cause international spillovers or disruptions in US credit markets. Three-month Treasury yields topped the 10-year yield last week, a so-called inversion that is often seen as a signal of a recession.

“We are not conditioned in the US to be dealing with a 4.5 per cent federal funds rate,” said Troy Ludtka, senior US economist at Natixis North America LLC, and there are concerns credit markets could be disrupted. “Internationally is even scarier. Europe looks terrible. China is not in recession, but I think it’s their slowest growth in a long, long time.”

Ethics Questions

Powell also could be asked about the latest incidents to raise questions about ethics standards at the central bank.

Atlanta Fed President Raphael Bostic recently revealed he violated central bank policy on financial transactions, leading Powell to ask the Fed’s inspector general to review his financial disclosures.

In a separate incident, Bullard last month attended a Citigroup-hosted meeting in Washington to which media were not invited and at which he discussed monetary policy. The St. Louis Fed has since said it would think differently about accepting such invitations in the future.

Speaking from personal experience, a bad hire isn’t a good look. The last thing you want is to hear, “Who the hell hired Bob?” and have your hiring judgment questioned.

The job seeker who’s empathetic to the employer’s side of the hiring desk, which controls the hiring process, is rare.

One of the best things you can do to enhance your job search is to practice perspective-taking, which involves seeing things from a different perspective.

It’s natural for employers to find candidates who have empathy and an understanding of their challenges and pain points more attractive. Candidates like these are seen as potential allies rather than individuals only looking out for themselves. Since most job seekers approach employers with a ‘what’s in it for me’ mindset, practicing perspective-taking sets you apart.

“If there is any one secret of success, it lies in the ability to get the other person’s point of view and see things from that person’s angle as well as from your own.” – Henry Ford.

Perspective-taking makes you realize that from an employer’s POV hiring is fraught with risks employers want to avoid; thus, you consider what most job seekers don’t: How can I present myself as the least risky hiring option?

Here’s an exercise that’ll help you visualize the employer’s side of the hiring process.

Candidate A or B?

Imagine you’re the Director of Customer Service for a regional bank with 85 branches. You’re hiring a call centre manager who’ll work onsite at the bank’s head office, overseeing the bank’s 50-seat call centre. In addition to working with the call centre agents, the successful candidate will also interact with other departments, your boss, and members of the C-suite leadership team; in other words, they’ll be visible throughout the bank.

The job posting resulted in over 400 applications. The bank’s ATS and HR (phone interview vetting, skill assessment testing) selected five candidates, plus an employee referral, for you to interview. You aim to shortlist the six candidates to three, whom you’ll interview a second time, and then make a hiring decision. Before scheduling the interviews, which’ll take place between all your other ongoing responsibilities, you spend 5 – 10 minutes with each candidate’s resume and review their respective digital footprint and LinkedIn activity.

In your opinion, which candidate deserves a second interview?

Candidate A: Their resume provides quantitative numbers—evidence—of the results they’ve achieved. (Through enhanced agent training, reduced average handle time from 4:32 mins. to 2:43 minutes, which decreased the abandon rate from 4.6% to 2.2%.)

Candidate B: Their resume offers only opinions. (“I’m detail-oriented,” “I learn fast.”)

Candidate A: Looks you in the eye, has a firm handshake, smiles, and exudes confidence.

Candidate B: Doesn’t look you in the eye, has a weak handshake.

Candidate A: Referred by Ariya, who’s been with the bank for over 15 years and has a stellar record, having moved up from teller to credit analyst and is tracking to become a Managing Director.

Candidate B: Applied online. Based on your knowledge, they did nothing else to make their application more visible. (e.g., reached out to you or other bank employees)

Candidate A: Well educated, grew up as a digital native, eager and energetic. Currently manages a 35-seat call center for a mid-size credit union. They mention they called the bank’s call centre several times and suggest ways to improve the caller experience.

Candidate B: Has been working in banking for over 25 years, managing the call center at their last bank for 17 years before being laid off eight months ago. They definitely have the experience to run a call centre. However, you have a nagging gut feeling that they’re just looking for a place to park themselves until they can afford to retire.

Candidate A: Has a fully completed LinkedIn profile (picture, eye-catching banner) packed with quantifying numbers. It’s evident how they were of value to their employers. Recently, they engaged constructively with posts and comments and published a LinkedIn article on managing Generations Y and Z call centre agents. Their Facebook, Instagram, and Twitter/X accounts aren’t controversial, sharing between ‘Happy Birthday’ and ‘Congratulations’ messages, their love of fine dining, baseball, and gardening.

Candidate B: Their LinkedIn profile is incomplete. The last time they posted on LinkedIn was seven months ago, ranting about how the government’s latest interest rate hike will plunge the country into a deep recession. Conspiracy theories abound on their Facebook page.

Candidate A: Notices the golf calendar on your desk, the putter and golf balls in the corner, and a photograph of Phil Mickelson putting on the green jacket at the 2010 Masters hanging on your wall. While nodding towards the picture, they say, “Evidently, you golf. Not being a golfer myself, what made you take up golf, which I understand is a frustrating sport?”

Candidate B: Doesn’t proactively engage in small talk. Waits for you to start the interview.

Which of the above candidates presents the least hiring risk? Will likely succeed (read: achieve the results the employer needs)? Will show your boss, upper management, and employees you know how to hire for competence and fit?

Nick Kossovan, a well-seasoned veteran of the corporate landscape, offers “unsweetened” job search advice. You can send Nick your questions to artoffindingwork@gmail.com.

Though I have no empirical evidence to support my claim, I believe job search success can be achieved faster by using what I call “The Job Seekers’ Trinity” as your framework, the trinity being:

The power of focus

Managing your anger

Presenting evidence

Each component plays a critical role in sustaining motivation and strategically positioning yourself for job search success. Harnessing your focus, managing your anger, and presenting compelling evidence (read: quantitative numbers of achieved results) will transform your job search from a daunting endeavour into a structured, persuasive job search campaign that employers will notice.

The Power of Focus

Your job search success is mainly determined by what you’re focused on, namely:

What you focus on.

Your life is controlled by what you focus on; thus, focusing on the positives shapes your mindset for positive outcomes. Yes, layoffs, which the media loves to report to keep us addicted to the news, are a daily occurrence, but so is hiring. Don’t let all the doom and gloom talk overshadow this fact. Focus on where you want to go, not on what others and the media want you to fear.

Bonus of not focusing on negatives: You’ll be happier.

Focus on how you can provide measurable value to employers.

If you’re struggling with your job search, the likely reason is that you’re not showing, along with providing evidence, employers how you can add tangible value to an employer’s bottom line. Business is a numbers game, yet few job seekers speak about their numbers. If you don’t focus on and talk about your numbers, how do you expect employers to see the value in hiring you?

Managing Your Anger

Displaying anger in public is never a good look. Professionals are expected to control their emotions, so public displays of anger are viewed as unprofessional.

LinkedIn has become a platform heavily populated with job seekers posting angry rants—fueled mainly by a sense of entitlement—bashing and criticizing employers, recruiters, and the government, proving many job seekers think the public display of their anger won’t negatively affect their job search.

When you’re unemployed, it’s natural to be angry when your family, friends, and neighbours are employed. “Why me?” is a constant question in your head. Additionally, job searching is fraught with frustrations, such as not getting responses to your applications and being ghosted after interviews.

The key is acknowledging your anger and not letting it dictate your actions, such as adding to the angry rants on LinkedIn and other social media platforms, which employers will see.

Undoubtedly, rejection, which is inevitable when job hunting, causes the most anger. What works for me is to reframe rejections, be it through being ghosted, email, a call or text, as “Every ‘No’ brings me one step closer to a ‘Yes.'”

Additionally, I’ve significantly reduced triggering my anger by eliminating any sense of entitlement and keeping my expectations in check. Neither you nor I are owed anything, including a job, respect, empathy, understanding, agreement, or even love. A sense of entitlement and anger are intrinsically linked. The more rights you perceive you have, the more anger you need to defend them. Losing any sense of entitlement you may have will make you less angry, which has no place in a job search.

Presenting Evidence

As I stated earlier, business is a numbers game. Since all business decisions, including hiring, are based on numbers, presenting evidence in the form of quantitative numbers is crucial.

Which candidate would you contact to set up an interview if you were hiring a social media manager:

“Managed Fabian Publishing’s social media accounts, posting content daily.”

“Designed and executed Fabian Publishing’s global social media strategy across 8.7 million LinkedIn, X/Twitter, Instagram and Facebook followers. Through consistent engagement with customers, followers, and influencers, increased social media lead generation by 46% year-over-year, generating in 2023 $7.6 million in revenue.”

Numerical evidence, not generic statements or opinions, is how you prove your value to employers. Stating you’re a “team player” or “results-driven,” as opposed to “I’m part of an inside sales team that generated in 2023 $8.5 million in sales,” or “In 2023 I managed three company-wide software implementations, all of which came under budget,” is meaningless to an employer.

Despite all the job search advice offered, I still see resumes and LinkedIn profiles listing generic responsibilities rather than accomplishments backed by numbers. A statement such as “managed a team” doesn’t convey your management responsibilities or your team’s achievements under your leadership. “Led a team of five to increase sales by 20%, from $3.7 million to $4.44 million, within six months” shows the value of your management skills.

Throughout your job search, constantly think of all the numbers you can provide—revenue generated, number of new clients, cost savings, reduced workload, waste reduction—as evidence to employers why you’d be a great value-add to their business.

The Job Seekers’ Trinity—focusing on the positive, managing your anger and providing evidence—is a framework that’ll increase the effectiveness of your job search activities and make you stand out in today’s hyper-competitive job market, thus expediting your job search to a successful conclusion.

Nick Kossovan, a well-seasoned veteran of the corporate landscape, offers “unsweetened” job search advice. You can send Nick your questions to artoffindingwork@gmail.com.

TOKYO (AP) — Japanese technology group SoftBank swung back to profitability in the July-September quarter, boosted by positive results in its Vision Fund investments.

Tokyo-based SoftBank Group Corp. reported Tuesday a fiscal second quarter profit of nearly 1.18 trillion yen ($7.7 billion), compared with a 931 billion yen loss in the year-earlier period.

Quarterly sales edged up about 6% to nearly 1.77 trillion yen ($11.5 billion).

SoftBank credited income from royalties and licensing related to its holdings in Arm, a computer chip-designing company, whose business spans smartphones, data centers, networking equipment, automotive, consumer electronic devices, and AI applications.

The results were also helped by the absence of losses related to SoftBank’s investment in office-space sharing venture WeWork, which hit the previous fiscal year.

WeWork, which filed for Chapter 11 bankruptcy protection in 2023, emerged from Chapter 11 in June.

SoftBank has benefitted in recent months from rising share prices in some investment, such as U.S.-based e-commerce company Coupang, Chinese mobility provider DiDi Global and Bytedance, the Chinese developer of TikTok.

SoftBank’s financial results tend to swing wildly, partly because of its sprawling investment portfolio that includes search engine Yahoo, Chinese retailer Alibaba, and artificial intelligence company Nvidia.

SoftBank makes investments in a variety of companies that it groups together in a series of Vision Funds.

The company’s founder, Masayoshi Son, is a pioneer in technology investment in Japan. SoftBank Group does not give earnings forecasts.