Uncredited

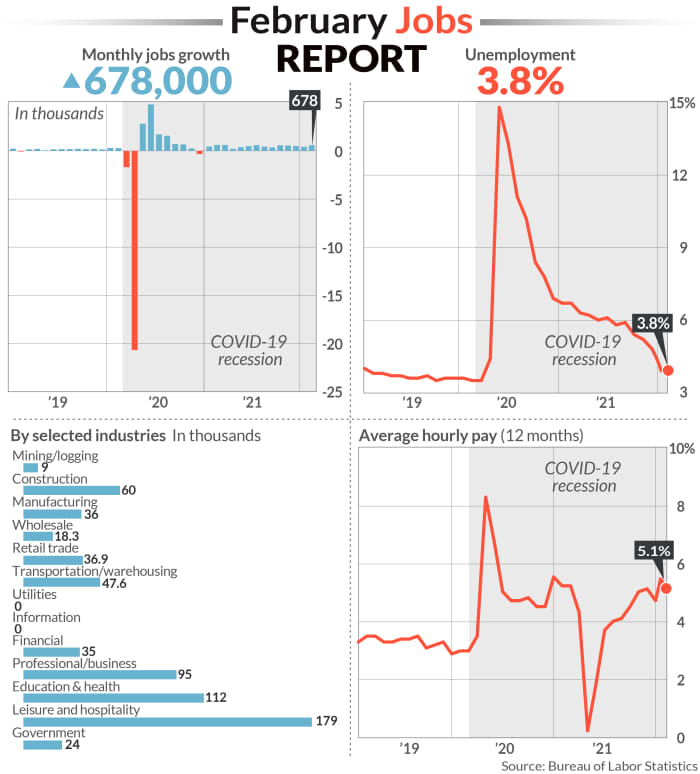

The numbers: The U.S. added 678,000 jobs in February and the unemployment rate fell again even as businesses grappled with the worst labor shortage in decades, signaling the economy is picking up after a slow start to the year.

The unemployment rate dropped to 3.8% from 4%, the government said Friday.

The increase in hiring last month — the biggest in seven months — exceeded forecasts. Economists polled by The Wall Street had estimated 440,000 new jobs.

The government’s employment report won’t sway the Federal Reserve as the central bank prepares for a series of interest-rate increases to try to tame the worst bout of U.S. inflation in 40 years.

The jobs report has also been less reliable over the past year owing to the waxing and waning of the pandemic. The estimates have been subject to large revisions months later that have presented a very different view of how many people are being hired.

One thing is clear, though. The labor market is very tight and it’s going away to stay that way for a while. Workers are taking advantage of the situation to leave their employers in droves for better-paying jobs.

Hourly wages only rose 1 cent to $31.58 in February, but worker pay is climbing at the fastest rate since the early 1980s.

Read: Soaring U.S. worker pay stalled in February, but probably not for long

“The ‘Great Resignation’ is real,” a technology executive told ISM. “Severe labor shortages are expected well into 2022.”

U.S. stocks fell in Friday trades and were little swayed by the jobs report. The war in Ukraine is the main focus of investors now.

Big picture: The economy is getting a tailwind from the steep decline in cases of the omicron variant of the coronavirus.

People who got sick from the highly contagious variant have returned to work. Governments have dropped business restrictions and companies have stepped up hiring efforts to try to cater to high demand for their goods and services.

Yet soaring inflation and ongoing shortages of labor and supplies are likely to constrain the economy in the first half of 2022 before easing, analysts predict. Americans are unlikely to buy as many houses, cars and other big-ticket items if prices keep rising and interest rates go up though.

The war in Ukraine also threatens to worsen inflation and deliver another shock to an already fragile global economy.

Key details: About a quarter of the new jobs created in February were in leisure and hospitality, the industries most affected when coronavirus cases were high.

Restaurants added 124,000 new jobs last month and hotels hired 28,000 people.

Hiring also rose strongly at white-collar professional jobs (95,000), health care (64,000), construction (60,000) and transportation and warehousing (48,000).

No industry reported a decline in employment.

The size of the labor force increased by 301,000 in February. The percentage of people in the labor force rose a tick to 62.3%, though it’s still well below the peak before the pandemic.

The economy would have about 3 million more workers if the so-called participation rate in the labor market was the same now as it was before the pandemic.

Hiring in January and December were somewhat stronger than previously reported. Job gains in the two months were raised by a combined 92,000.

Steady hiring is pushing the unemployment rate back to precrisis levels, when it had fallen to a half-century low of 3.5%.

The tight labor market is a blessing for many workers. They’ve switched jobs for better pay or gotten higher wages from their current employers.

Over the past year the average paycheck has increased by 5.1% — one of the fastest increase since the early 1980s.

“Employers continue to struggle to bring in new workers and keep existing ones,” said Thomas Barkin, president of the Richmond Federal Reserve.

Rising pay still isn’t keeping up with inflation, however. The cost of living jumped 7.5% in the 12 months ended in January.

Higher wages could even add to inflationary pressures unless accompanied by increases in worker productivity.

In a worst-case scenario, a dreaded wage-price spiral could take place and keep inflation at worrisomely high levels.

Looking ahead: “If we see more numbers like this moving forward, we can be optimistic about this year. Employment is growing at a strong rate and joblessness is getting closer and closer to pre-pandemic levels,” said Indeed Hiring Lab Research Director Nick Bunker. “Still, in these uncertain times, we cannot take anything for granted.”

“What this tells me is that the U.S. economy is open for business. Omicron is in the past, and businesses expect demand to remain strong going forward,” said John Leer, chief economist at Morning Consult.

Market reaction: The Dow Jones Industrial Average

DJIA,

-0.53%

and S&P 500

SPX,

-0.79%

were sank in Friday trades. Stocks have been under pressure the past week since the Russian invasion of Ukraine.