Photographer: Francois Nel/Getty Images

The United Arab Emirates will likely suffer a deeper economic contraction this year than previously estimated, hurt by disruptions caused by the coronavirus pandemic and lower oil prices.

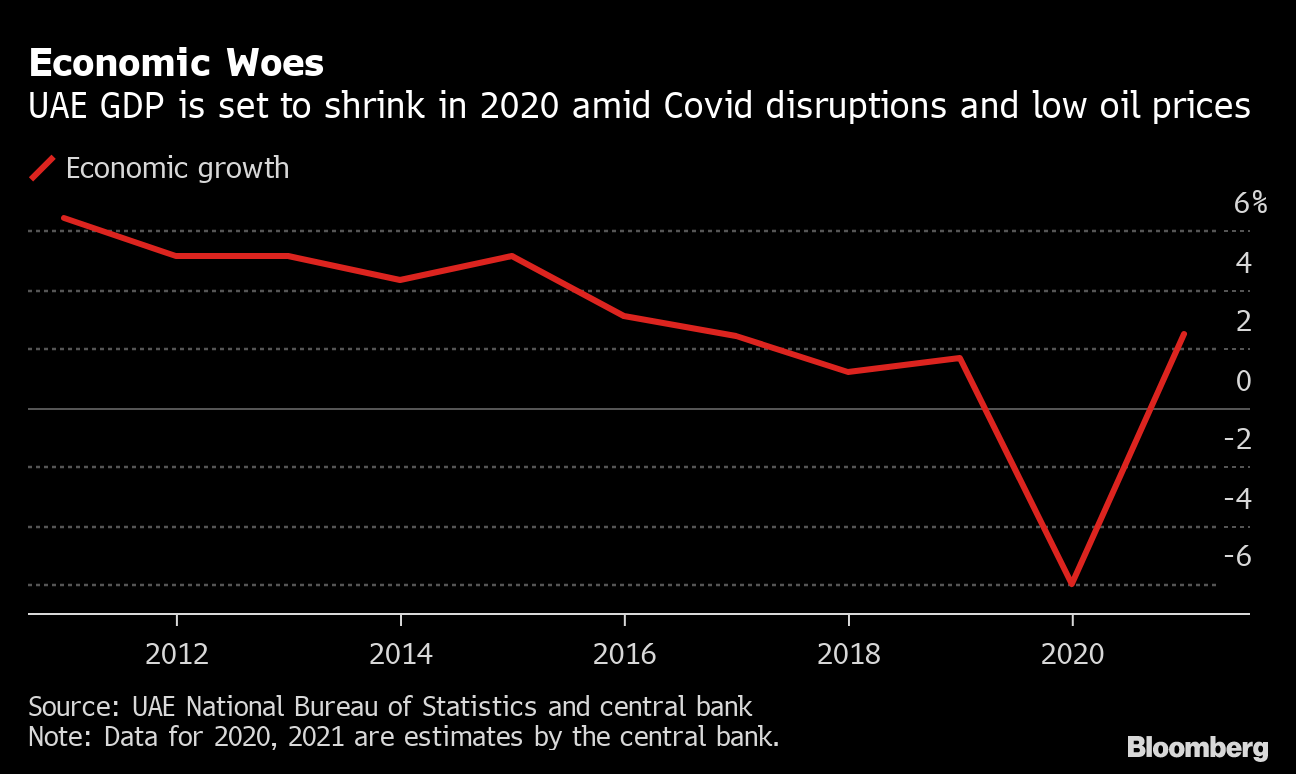

Gross domestic product in the Arab world’s second-largest economy is estimated to shrink about 6% in 2020, compared with a previous forecast for a decline of 5.2%, the central bank said in its quarterly review on Tuesday. The economy is expected to grow 2.5% in 2021.

Economic Woes

UAE GDP is set to shrink in 2020 amid Covid disruptions and low oil prices

Source: UAE National Bureau of Statistics and central bank

Note: Data for 2020, 2021 are estimates by the central bank.

.chart-js display: none;

The outlook is slightly better than forecasts from the International Monetary Fund, which expects a decline of 6.6% this year. The UAE economy last contracted by more than 5% in 2009, according to the fund.

“As an oil exporter, the UAE is likely to feel the fallout from reduced global demand for oil due to the contraction of economic activities worldwide, including transportation and international travel,” according to the central bank report. “Real oil GDP is projected to contract in 2020, corresponding to an average oil production of 2.8 million barrels per day for the year as a whole.”

More from the report:

- Non-oil GDP is seen growing 3.6% in 2021, fueled by an increase in fiscal spending, pick up in credit and employment as well as a stabilization in the property market

- Oil GDP next year is expected to remain flat as a result of OPEC+ production cuts

- This year, crude production fell by 4.1% year-on-year during the second quarter and by 17.7% during the following quarter