When trying to forecast or analyze what is going to happen in economic policy in a particular country, I focus on four factors: ideas, incentives, leadership, and providence or luck. When some of these factors align, as in 2017 when U.S. leadership embraced a policy of tax reduction and regulatory reform, I forecast an increase in growth. I was right. Other factors that I usually include are uncertainty in leadership; the push or drag of major players in the world economy; and medium- and long-term rule of law and overall economic freedom in the country or region in focus.

Another factor I usually include is national and international security. For instance, I consider the threat of a violent nuclear incident as the greatest menace to domestic and international prosperity, and North Korea has been back in the news in this regard. The less catastrophic but more widespread threat of Islamic terrorism is also a concern. Whatever one may think of President Trump’s approach to Islamic extremism, I think it is safe to say that there is a new level of unpredictability, and extremist groups do not know where or when another strike and response may come.

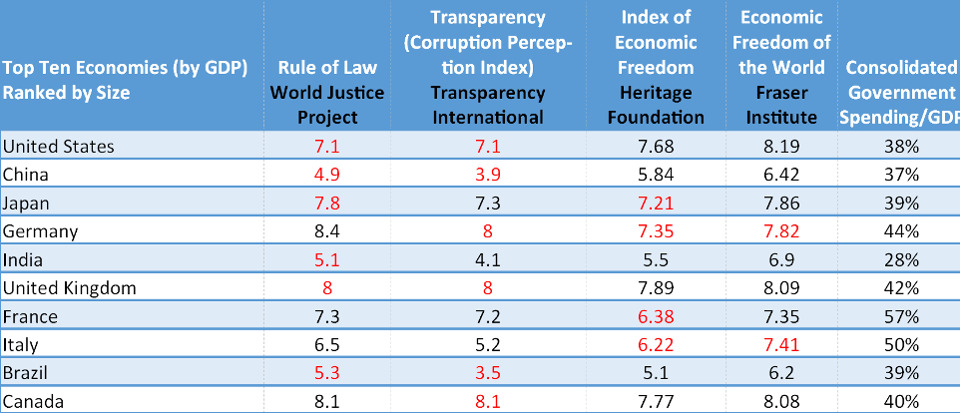

Rule of law, corruption, economic freedom, and government spending for the top ten economies. Rule … [+] of law from World Justice Project; Corruption Perception Index, from Transparency International; Economic Freedom from Heritage Foundation (2019) and Fraser Institute (2017 data, per methodolgy); Government spending: last three year average, from Heritage Index of Economic Freedom. In red, declines in scores. Table by Alejandro Chafuen

Los Angeles, Ca. Shipping containers are offloaded from the container ship APL Singapore onto … [+] Terminal Island at the busy Port of Los Angeles. The vessel APL Singapore is being retrofitted with a system that will dilute its fuel with water. The Wife On Demand system (Water In Fuel Emulsion) promises to reduce the amount of pollutants released into the environment. (Photo by Rick Loomis/Los Angeles Times via Getty Images) Los Angeles Times via Getty Images

China’s growth continues to moderate and hover around 6%. India is poised to grow at 4%, which is high for us but low for them. At least two factors having a negative effect on China are trade skirmishes with the United States and the situation in Hong Kong; both will still be with us in 2020. “2019 was a horrible year for Xi Jinping’s China” was the headline of a recent article in the French newspaper Le Monde.

In Mexico, Latin America’s second largest economy and one of the most relevant for the United States, continues to slow. Its president, Andrés Manuel López Obrador, has limited populist measures to redistribution, by which I mean he has not jumped on the protectionist bandwagon or given in to the temptation to impose exchange controls or expand price controls unlike other populist leaders. The economy is at a standstill, with no growth expected for 2020. The United States’ other major trading partner, Canada, is predicted to grow at a modest 1.5%. During the last stretch of the recent electoral campaign, the re-elected Prime Minister Justin Trudeau promised increased government spending as if this were a magic formula for growth. Among the top ten economies, France has the largest consolidated government spending per GDP (56%), and yet its growth is even slower than Canada’s.

Not much help will come from other countries in Europe, either. Their bloated welfare states and hostile climate of ideas – especially on the environment – continue to be anti-growth. The attitude towards the environment in many European countries seems driven more by religious fervor than science and economic reality. I was in Italy during the “student” anti-growth demonstrations in September, and in Madrid during the recent environmental summit. They “canonized” their saint Greta of Sweden as a powerful and effective weapon against the demons of economic development. If they move from merely show to actions, a regulatory push on climate could have an even higher negative effect on growth.

The harm will be mostly in Western Europe; in other regions, most of the large economies have governments which will not follow the so-called environmental policy “consensus.” The two largest economies of the Americas, the United States and Brazil, have a similar approach and understanding of environmental matters: a more prosperous economy can and should contribute to better ecological stewardship. In Asia, independently of what agreements their bureaucrats sign, the governments of the two largest Asian economies, China and India, will prioritize growth even more than the United States and Brazil.

Last January I forecast a slowdown in growth rate, due mostly to two factors: an all-out war of the Deep State against President Trump, and a tightening by the Fed. There was a modest decline in the rate of growth, and the Deep State’s efforts against Donald Trump and his allies in the administration were as I expected. But I was wrong in believing that the Fed was going to stick to the measures that they hinted at in late 2018. Independently of what the numbers and monetary economists say, the leadership of Donald Trump and the acquiescence of the Fed played a big role in the reversal. Seeing the large deficits coexist with very low interest rates is not something that we studied in depth at universities. Yet, in the West, the United States and Canada still have the highest Central Bank interest rates, so it is not irrational for leaders in both countries to call for even lower rates.

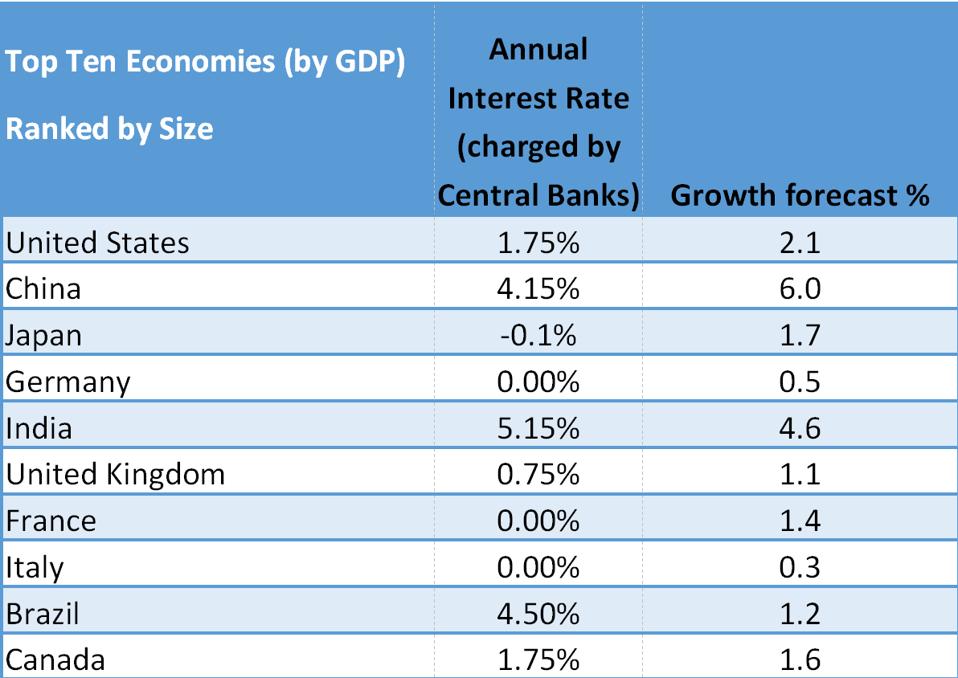

Interest rates and growth forecast of the ten largest economies. Interest rate data and 2020 GDP … [+] growth forecast by TradingEconomics Table by Alejandro Chafuen

Given that almost all the candidates in the Democratic Party promise a reversal of the regulatory and tax policies of the Trump administration, economic agents face a scenario of “fear, uncertainty, and doubt,” or FUD. This scenario – similar to the situation in the United Kingdom during these past few years of Brexit impasse – puts a damper on investment decisions. The efforts of most of the entrenched bureaucracy against Trump will continue, and so will their effect of creating uncertainty about the future direction of economic policy. But the danger of the Deep State impact has diminished. During 2019 some in their camp began to show their cards and acknowledge the Deep State’s existence. While in the past those who alleged the existence of the Deep State were ridiculed, now we find those who proudly assert “thank God for the Deep State.” One of these latter was John MacLaughlin, former Central Intelligence Agency deputy director. For him and those of his ilk, they are the grown-ups protecting the country from Trump. He actually said with a straight face that the CIA is different than other agencies because it “is institutionally committed to objectivity and of telling the truth.”

Thus, what happens in the U.S. economy will influence the world, more than the other way around. To put things in perspective, our economy is more than 10 times larger than that of Brazil, India or Canada, the bottom three in the top 10. Among the top-10 economies, only China and India will grow more than the United States in 2020. In this group, growth is expected to accelerate only in Brazil and the United Kingdom, and even there not by much. Both are currently headed by leaders who favor a free economy and who are seen as a threat by many in the international and local entrenched bureaucracies.

On issues that affect long-term growth, such as rule of law and transparency, the world is at a standstill. Six of the top-10 economies have shown deterioration in their rule of law and transparency scores. Sound money and free trade are two areas of grave concern for lovers of the free economy. In both areas President Trump has generated doubts. It is in these two areas that the indices of economic freedom have shown greatest improvement over the last quarter century. The forces that led to improvements in trade and monetary stability are still with us, and they feed my optimism that the major economies will not push for major protectionist measures and that we will not enter a sustained inflationary period in the near future. We still do not know where the average tariffs will end up after Peter Navarro’s “reciprocity bouts,” especially when it comes to major U.S. trading partners.

With regard to sound money, those who measure it mostly by price level or inflation do not seem alarmed. Apart from the dwindling ranks of libertarians, few seem concerned with government spending. Not only Trudeau but also President Trump, Prime Minister Boris Johnson, and other leaders of the top-10 economies are willing to sign increases in government spending. And at least in the United Kingdom and the United States, the opposition wants even more spending. Sadly, Sebastián Piñera, the president of the freest economy in Latin America, has also announced a plan to expand government expenditures and interventionism. Given its small size (1.5% of the United States), Chile is less relevant to the world economy, but until now it had served as a positive example for those who promote freer economic systems. That is gone now.

We have never had so much economic data at our fingertips. But given leadership doubts and a new quasi-consensus on higher spending and low interest rates, we have nothing close to a 20/20 vision of the 2020 economy. Balancing all these factors, however, and with none of the economic trends pointing to a crisis in the short term, the U.S. economy, like a slow-moving giant ship, will continue to push forward and ahead of most Western economies.

OTTAWA – Canada’s unemployment rate held steady at 6.5 per cent last month as hiring remained weak across the economy.

Statistics Canada’s labour force survey on Friday said employment rose by a modest 15,000 jobs in October.

Business, building and support services saw the largest gain in employment.

Meanwhile, finance, insurance, real estate, rental and leasing experienced the largest decline.

Many economists see weakness in the job market continuing in the short term, before the Bank of Canada’s interest rate cuts spark a rebound in economic growth next year.

Despite ongoing softness in the labour market, however, strong wage growth has raged on in Canada. Average hourly wages in October grew 4.9 per cent from a year ago, reaching $35.76.

Friday’s report also shed some light on the financial health of households.

According to the agency, 28.8 per cent of Canadians aged 15 or older were living in a household that had difficulty meeting financial needs – like food and housing – in the previous four weeks.

That was down from 33.1 per cent in October 2023 and 35.5 per cent in October 2022, but still above the 20.4 per cent figure recorded in October 2020.

People living in a rented home were more likely to report difficulty meeting financial needs, with nearly four in 10 reporting that was the case.

That compares with just under a quarter of those living in an owned home by a household member.

Immigrants were also more likely to report facing financial strain last month, with about four out of 10 immigrants who landed in the last year doing so.

That compares with about three in 10 more established immigrants and one in four of people born in Canada.

This report by The Canadian Press was first published Nov. 8, 2024.

The Canadian Institute for Health Information says health-care spending in Canada is projected to reach a new high in 2024.

The annual report released Thursday says total health spending is expected to hit $372 billion, or $9,054 per Canadian.

CIHI’s national analysis predicts expenditures will rise by 5.7 per cent in 2024, compared to 4.5 per cent in 2023 and 1.7 per cent in 2022.

This year’s health spending is estimated to represent 12.4 per cent of Canada’s gross domestic product. Excluding two years of the pandemic, it would be the highest ratio in the country’s history.

While it’s not unusual for health expenditures to outpace economic growth, the report says this could be the case for the next several years due to Canada’s growing population and its aging demographic.

Canada’s per capita spending on health care in 2022 was among the highest in the world, but still less than countries such as the United States and Sweden.

The report notes that the Canadian dental and pharmacare plans could push health-care spending even further as more people who previously couldn’t afford these services start using them.

This report by The Canadian Press was first published Nov. 7, 2024.

Canadian Press health coverage receives support through a partnership with the Canadian Medical Association. CP is solely responsible for this content.

As Canadians wake up to news that Donald Trump will return to the White House, the president-elect’s protectionist stance is casting a spotlight on what effect his second term will have on Canada-U.S. economic ties.

Some Canadian business leaders have expressed worry over Trump’s promise to introduce a universal 10 per cent tariff on all American imports.

A Canadian Chamber of Commerce report released last month suggested those tariffs would shrink the Canadian economy, resulting in around $30 billion per year in economic costs.

More than 77 per cent of Canadian exports go to the U.S.

Canada’s manufacturing sector faces the biggest risk should Trump push forward on imposing broad tariffs, said Canadian Manufacturers and Exporters president and CEO Dennis Darby. He said the sector is the “most trade-exposed” within Canada.

“It’s in the U.S.’s best interest, it’s in our best interest, but most importantly for consumers across North America, that we’re able to trade goods, materials, ingredients, as we have under the trade agreements,” Darby said in an interview.

“It’s a more complex or complicated outcome than it would have been with the Democrats, but we’ve had to deal with this before and we’re going to do our best to deal with it again.”

American economists have also warned Trump’s plan could cause inflation and possibly a recession, which could have ripple effects in Canada.

It’s consumers who will ultimately feel the burden of any inflationary effect caused by broad tariffs, said Darby.

“A tariff tends to raise costs, and it ultimately raises prices, so that’s something that we have to be prepared for,” he said.

“It could tilt production mandates. A tariff makes goods more expensive, but on the same token, it also will make inputs for the U.S. more expensive.”

A report last month by TD economist Marc Ercolao said research shows a full-scale implementation of Trump’s tariff plan could lead to a near-five per cent reduction in Canadian export volumes to the U.S. by early-2027, relative to current baseline forecasts.

Retaliation by Canada would also increase costs for domestic producers, and push import volumes lower in the process.

“Slowing import activity mitigates some of the negative net trade impact on total GDP enough to avoid a technical recession, but still produces a period of extended stagnation through 2025 and 2026,” Ercolao said.

Since the Canada-United States-Mexico Agreement came into effect in 2020, trade between Canada and the U.S. has surged by 46 per cent, according to the Toronto Region Board of Trade.

With that deal is up for review in 2026, Canadian Chamber of Commerce president and CEO Candace Laing said the Canadian government “must collaborate effectively with the Trump administration to preserve and strengthen our bilateral economic partnership.”

“With an impressive $3.6 billion in daily trade, Canada and the United States are each other’s closest international partners. The secure and efficient flow of goods and people across our border … remains essential for the economies of both countries,” she said in a statement.

“By resisting tariffs and trade barriers that will only raise prices and hurt consumers in both countries, Canada and the United States can strengthen resilient cross-border supply chains that enhance our shared economic security.”

This report by The Canadian Press was first published Nov. 6, 2024.