The pace of U.S. hiring accelerated in June, with payrolls increasing by the most in 10 months, suggesting firms are having greater success recruiting workers to keep pace with the economy’s reopening.

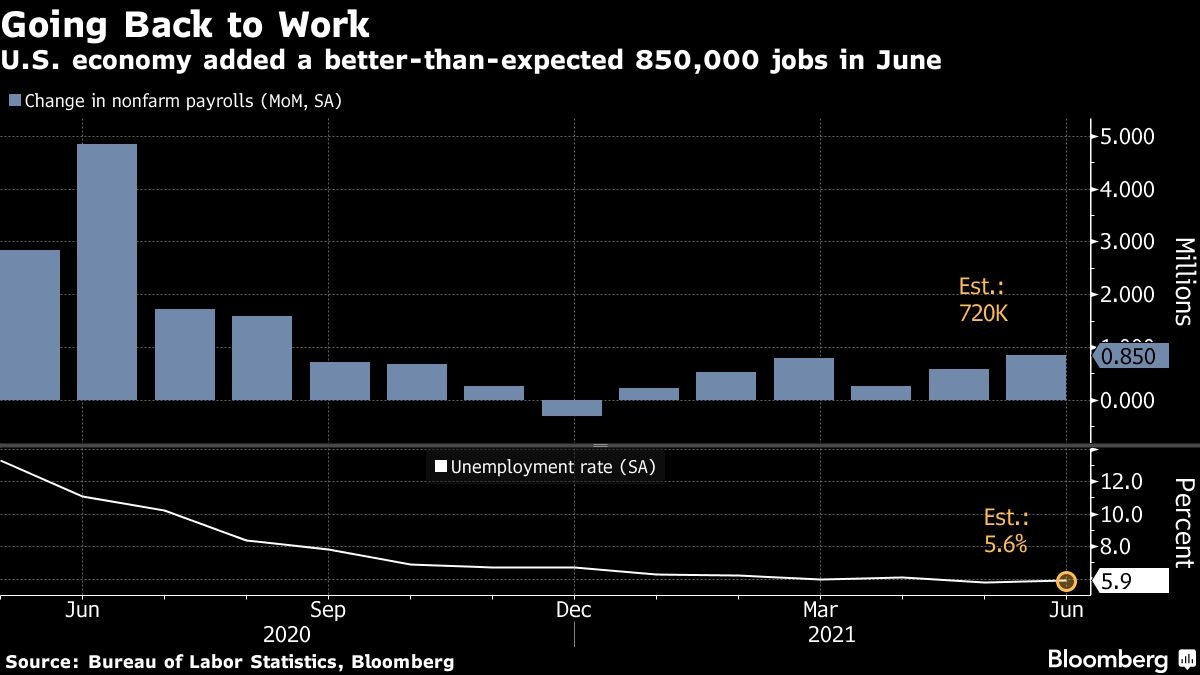

Nonfarm payrolls jumped by 850,000 last month, bolstered by strong job gains in leisure and hospitality, a Labor Department report showed Friday. The unemployment rate edged up to 5.9 per cent because more people voluntarily left their jobs and the number of job seekers rose.

The median estimate in a Bloomberg survey of economists was for a 720,000 rise in June payrolls.

“Things are picking up,” said Nick Bunker, an economist at the job-search company Indeed. “While labor supply may not be as responsive as some employers might like, they are adding jobs at an increasing rate.”

The gain in payrolls, while well above expectations, doesn’t markedly raise pressure on the Federal Reserve to pare monetary policy support for the economy. Even with the latest advance, U.S. payrolls are still 6.76 million below their pre-pandemic level.

Stocks opened higher and Treasury securities fluctuated after the report.

Demand for labor remains robust as employers strive to keep pace with a firming economy, fueled by the lifting of restrictions on business and social activity, mass vaccinations and trillions of dollars in federal relief.

At the same time, a limited supply of labor continues to beleaguer employers, with the number of Americans on payrolls still well below pre-pandemic levels.

Coronavirus concerns, child-care responsibilities and expanded unemployment benefits are all likely contributing to the record number of unfilled positions. Those factors should abate in the coming months though, supporting future hiring.

Wage growth is also picking up as businesses raise pay to attract candidates. The June jobs report showed a hefty 2.3 per cent month-over-month increase in non-supervisory workers’ average hourly earnings in the leisure and hospitality industry. Overall average earnings rose 0.3 per cent last month.

What Bloomberg Economics Says…

“For the Federal Reserve, the data should be sufficient to move the dialogue forward on tapering discussions this summer. Substantial further progress should be clearer this fall, with an actual reduction to commence in early 2022, in our view.”

— Andrew Husby and Eliza Winger, economists

For President Joe Biden’s administration, the report offers some relief after prior months showed disappointing job gains.

“The strength of our recovery is helping us flip the script,” Biden said in remarks Friday. “Instead of workers competing with each other for jobs that are scarce, employers are competing with each other to attract workers.”

The Labor Department’s figures showed a 343,000 increase in leisure and hospitality payrolls, a sector that’s taking longer to recover because of the pandemic.

Job growth last month was also bolstered by a 188,000 gain in government payrolls. State and local government education employment rose about 230,000, boosted by seasonal adjustments to offset the typical declines seen at the end of the school year.

Hiring was relatively broad-based in June, including other notable gains in business services and retail trade. However, construction payrolls dropped for a third straight month and manufacturing employment rose less than forecast.

“Most of the new jobs now being created are in sectors that were slammed by the pandemic, while companies in other industries are struggling to find available workers,” Sal Guatieri, senior economist at BMO Capital Markets, said in a note.

The overall participation rate held steady and remained well short of pre-pandemic levels. The employment population ratio, or the share of the population that’s currently working, was also unchanged.

Digging deeper

Average weekly hours decreased to 34.7 hours from 34.8

The participation rate for women age 25 to 54 rose by 0.4 percentage point; the rate among men in that age group also climbed

The number of Americans classified as long-term unemployed, or those who have been unemployed for 27 weeks or more, increased by the most since November

The U-6 rate, also known as the underemployment rate, fell to a pandemic low of 9.8 per cent. The broad measure includes those who are employed part-time for economic reasons and those who have stopped looking for a job because they are discouraged about their job prospects

TOKYO (AP) — Japanese technology group SoftBank swung back to profitability in the July-September quarter, boosted by positive results in its Vision Fund investments.

Tokyo-based SoftBank Group Corp. reported Tuesday a fiscal second quarter profit of nearly 1.18 trillion yen ($7.7 billion), compared with a 931 billion yen loss in the year-earlier period.

Quarterly sales edged up about 6% to nearly 1.77 trillion yen ($11.5 billion).

SoftBank credited income from royalties and licensing related to its holdings in Arm, a computer chip-designing company, whose business spans smartphones, data centers, networking equipment, automotive, consumer electronic devices, and AI applications.

The results were also helped by the absence of losses related to SoftBank’s investment in office-space sharing venture WeWork, which hit the previous fiscal year.

WeWork, which filed for Chapter 11 bankruptcy protection in 2023, emerged from Chapter 11 in June.

SoftBank has benefitted in recent months from rising share prices in some investment, such as U.S.-based e-commerce company Coupang, Chinese mobility provider DiDi Global and Bytedance, the Chinese developer of TikTok.

SoftBank’s financial results tend to swing wildly, partly because of its sprawling investment portfolio that includes search engine Yahoo, Chinese retailer Alibaba, and artificial intelligence company Nvidia.

SoftBank makes investments in a variety of companies that it groups together in a series of Vision Funds.

The company’s founder, Masayoshi Son, is a pioneer in technology investment in Japan. SoftBank Group does not give earnings forecasts.

Shopify Inc. executives brushed off concerns that incoming U.S. President Donald Trump will be a major detriment to many of the company’s merchants.

“There’s nothing in what we’ve heard from Trump, nor would there have been anything from (Democratic candidate) Kamala (Harris), which we think impacts the overall state of new business formation and entrepreneurship,” Shopify’s chief financial officer Jeff Hoffmeister told analysts on a call Tuesday.

“We still feel really good about all the merchants out there, all the entrepreneurs that want to start new businesses and that’s obviously not going to change with the administration.”

Hoffmeister’s comments come a week after Trump, a Republican businessman, trounced Harris in an election that will soon return him to the Oval Office.

On the campaign trail, he threatened to impose tariffs of 60 per cent on imports from China and roughly 10 per cent to 20 per cent on goods from all other countries.

If the president-elect makes good on the promise, many worry the cost of operating will soar for companies, including customers of Shopify, which sells e-commerce software to small businesses but also brands as big as Kylie Cosmetics and Victoria’s Secret.

These merchants may feel they have no choice but to pass on the increases to customers, perhaps sparking more inflation.

If Trump’s tariffs do come to fruition, Shopify’s president Harley Finkelstein pointed out China is “not a huge area” for Shopify.

However, “we can’t anticipate what every presidential administration is going to do,” he cautioned.

He likened the uncertainty facing the business community to the COVID-19 pandemic where Shopify had to help companies migrate online.

“Our job is no matter what comes the way of our merchants, we provide them with tools and service and support for them to navigate it really well,” he said.

Finkelstein was questioned about the forthcoming U.S. leadership change on a call meant to delve into Shopify’s latest earnings, which sent shares soaring 27 per cent to $158.63 shortly after Tuesday’s market open.

The Ottawa-based company, which keeps its books in U.S. dollars, reported US$828 million in net income for its third quarter, up from US$718 million in the same quarter last year, as its revenue rose 26 per cent.

Revenue for the period ended Sept. 30 totalled US$2.16 billion, up from US$1.71 billion a year earlier.

Subscription solutions revenue reached US$610 million, up from US$486 million in the same quarter last year.

Merchant solutions revenue amounted to US$1.55 billion, up from US$1.23 billion.

Shopify’s net income excluding the impact of equity investments totalled US$344 million for the quarter, up from US$173 million in the same quarter last year.

Daniel Chan, a TD Cowen analyst, said the results show Shopify has a leadership position in the e-commerce world and “a continued ability to gain market share.”

In its outlook for its fourth quarter of 2024, the company said it expects revenue to grow at a mid-to-high-twenties percentage rate on a year-over-year basis.

“Q4 guidance suggests Shopify will finish the year strong, with better-than-expected revenue growth and operating margin,” Chan pointed out in a note to investors.

This report by The Canadian Press was first published Nov. 12, 2024.

TORONTO – RioCan Real Estate Investment Trust says it has cut almost 10 per cent of its staff as it deals with a slowdown in the condo market and overall pushes for greater efficiency.

The company says the cuts, which amount to around 60 employees based on its last annual filing, will mean about $9 million in restructuring charges and should translate to about $8 million in annualized cash savings.

The job cuts come as RioCan and others scale back condo development plans as the market softens, but chief executive Jonathan Gitlin says the reductions were from a companywide efficiency effort.

RioCan says it doesn’t plan to start any new construction of mixed-use properties this year and well into 2025 as it adjusts to the shifting market demand.

The company reported a net income of $96.9 million in the third quarter, up from a loss of $73.5 million last year, as it saw a $159 million boost from a favourable change in the fair value of investment properties.

RioCan reported what it says is a record-breaking 97.8 per cent occupancy rate in the quarter including retail committed occupancy of 98.6 per cent.

This report by The Canadian Press was first published Nov. 12, 2024.