Geopolitical risk had been in the spotlight for several weeks and the US government had warned about the deployment of forces on the Ukrainian border. Many investors, however, wanted to believe in a rapid, negotiated resolution even after Russia issued a presidential decree recognising the ‘independence’ of the ‘Donetsk People’s Republic’ and the ‘Luhansk People’s Republic’ on 21 February and then invaded the Ukraine on 24 March.

The fall in global equities in February (-2.7% for the MSCI AC World index in US dollars) was relatively modest given that an allusion was made to the use of nuclear weapons.

The environment in the financial markets has changed radically in the first week of March with a pronounced flight to safety in the face of the abrupt fall in equity valuations, particularly apparent in Europe, on account of the geographical proximity of the conflict.

This new environment has led to a rapid fall in bond yields. The yield of the US 10-year Treasury note closed at 1.73% on 1 March, down 26bp compared to 23 February. In the eurozone, the yield of the 10-year German Bund fell back to below the threshold of 0% for the first time since the end of January to close at -0.07%, down 30bp from 23 February.

This downward trend in yields was likely accentuated by investors covering underweight positions.

…and something more

The fall in bond yields was even more pronounced in the ‘peripheral’ markets of the eurozone. The yield of the 10-year Italian BTP fell from 1.94% on 23 February to 1.40% on 1 March, a drop of more than 50bp reducing the spread versus the German 10-year yield to below 1.50%, its lowest level since the beginning of February.

This outperformance of ‘peripheral’ eurozone debt reflects an adjustment in monetary policy expectations. While statements by the US Federal Reserve (Fed) and the European Central Bank (ECB) since the beginning of the year had signalled an imminent hawkish turn in policy, which was duly priced by markets, investors are now seeking to establish to what extent the geopolitical crisis is likely to change the direction of travel for monetary policy.

Several FOMC (Federal Open Market Committee) members have already hinted that the situation in the Ukraine could be taken into consideration at their 16 March meeting. These comments led investors to lower their expectations for an increase in the federal funds target rate: Forward markets now anticipate the Fed will raise official rates by 25bp between four and five times in 2022. This compares with expectations of almost seven such rate hikes previously.

The adjustments are even sharper for the ECB: Some members of the governing council, who had previously made hawkish statements about the need to raise policy rates, have said the conflict could delay the winding-down of support policies as the global economic environment is now more uncertain.

Hawks and doves on the council appear to agree that the normalisation of monetary policy could be slowed. In the case of the ECB, this could mean prolonging asset purchases. The outperformance of Italian bonds appears to indicate this is what investors now expect.

Let’s not forget inflation

Central banks have nuanced their hawkish rhetoric in the wake of recent events by emphasising the rise in uncertainty, but should we conclude that they will abandon plans to normalise monetary policies as they detailed in January and February?

In other words, has the economic situation changed dramatically since the last week of February? This question is difficult to answer given the nature of this new shock.

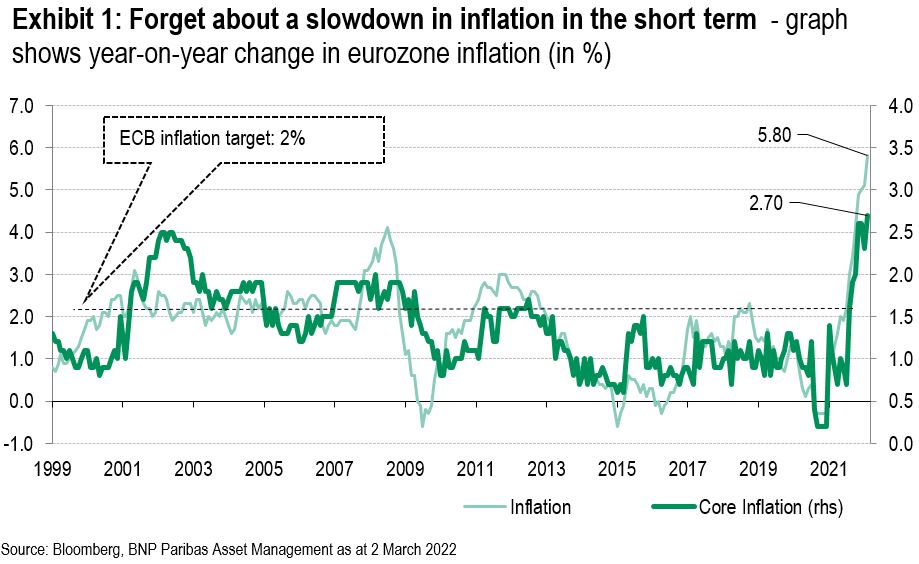

One thing, however, seems certain in the short term: The rise in the cost of commodities (energy, but also agricultural products as Russia and Ukraine account for almost a quarter of world wheat exports) will lead to another increase in producer and consumer prices.

According to the flash estimate released on 2 March, inflation in the eurozone was running at 5.8% year-on-year in February (after 5.1% in January). For the second consecutive month, the scenario, long central to ECB thinking, of an ebb in inflationary pressures in early 2022 has failed to materialise. In addition, core inflation, excluding food and energy, also accelerated in February to stand at 2.7% after 2.3% in January and 2.6% at the end of 2021.

In the US, the Fed’s preferred measure of core inflation, the personal consumption expenditures index excluding food and energy prices (5.2% year-on-year in January), has been above 3.5% since June, well above the central bank’s 2% target and not really consistent with the ‘transitory ‘inflation scenario which admittedly the Fed has abandoned since November. In addition, various indicators are converging to show a significant acceleration in wage increases.

What effects of the Ukrainian crisis on economic growth?

Again, uncertainty dominates, and although the direct exposure (measured by exports) of the eurozone to Russia and the Ukraine is limited, it is uneven across countries, as is their dependence on energy imports. In addition, the confidence of economic agents, who after two years of pandemic were starting to contemplate a return to normal life, could be affected, perhaps durably. On the other hand, business surveys point to a bright outlook for employment and activity.

Early estimates of the economic implications of the conflict mainly take into account new assumptions about oil and commodity prices. The scenario presented at an internal meeting by Philip Lane, the ECB’s chief economist, envisages a 0.3 to 0.4 percentage point decrease in GDP growth this year. In December, Eurosystem staff projections anticipated annual GDP growth of 4.2% in 2022. A more comprehensive assessment is expected to be presented on 10 March at the Governing Council.

Until then, let’s leave the last word to Fabio Panetta, member of the Executive Board of the ECB:

‘It would be unwise to pre-commit on future policy steps until the fallout from the current crisis becomes clearer’.

Mr. Panetta has traditionally been seen as a dove and his speech is in line with that mind set, but as such his words can reconcile hawks, doves and markets. In a highly uncertain environment, one should not rush, even when it comes to reappraising previous findings.

Disclaimer

Any views expressed here are those of the author as of the date of publication, are based on available information, and are subject to change without notice. Individual portfolio management teams may hold different views and may take different investment decisions for different clients. The views expressed in this podcast do not in any way constitute investment advice.

The value of investments and the income they generate may go down as well as up and it is possible that investors will not recover their initial outlay. Past performance is no guarantee for future returns.

Investing in emerging markets, or specialised or restricted sectors is likely to be subject to a higher-than-average volatility due to a high degree of concentration, greater uncertainty because less information is available, there is less liquidity or due to greater sensitivity to changes in market conditions (social, political and economic conditions).

Some emerging markets offer less security than the majority of international developed markets. For this reason, services for portfolio transactions, liquidation and conservation on behalf of funds invested in emerging markets may carry greater risk.

NEW YORK (AP) — Shares of Tesla soared Wednesday as investors bet that the electric vehicle maker and its CEO Elon Musk will benefit from Donald Trump’s return to the White House.

Tesla stands to make significant gains under a Trump administration with the threat of diminished subsidies for alternative energy and electric vehicles doing the most harm to smaller competitors. Trump’s plans for extensive tariffs on Chinese imports make it less likely that Chinese EVs will be sold in bulk in the U.S. anytime soon.

“Tesla has the scale and scope that is unmatched,” said Wedbush analyst Dan Ives, in a note to investors. “This dynamic could give Musk and Tesla a clear competitive advantage in a non-EV subsidy environment, coupled by likely higher China tariffs that would continue to push away cheaper Chinese EV players.”

Tesla shares jumped 14.8% Wednesday while shares of rival electric vehicle makers tumbled. Nio, based in Shanghai, fell 5.3%. Shares of electric truck maker Rivian dropped 8.3% and Lucid Group fell 5.3%.

Tesla dominates sales of electric vehicles in the U.S, with 48.9% in market share through the middle of 2024, according to the U.S. Energy Information Administration.

Subsidies for clean energy are part of the Inflation Reduction Act, signed into law by President Joe Biden in 2022. It included tax credits for manufacturing, along with tax credits for consumers of electric vehicles.

Musk was one of Trump’s biggest donors, spending at least $119 million mobilizing Trump’s supporters to back the Republican nominee. He also pledged to give away $1 million a day to voters signing a petition for his political action committee.

In some ways, it has been a rocky year for Tesla, with sales and profit declining through the first half of the year. Profit did rise 17.3% in the third quarter.

The U.S. opened an investigation into the company’s “Full Self-Driving” system after reports of crashes in low-visibility conditions, including one that killed a pedestrian. The investigation covers roughly 2.4 million Teslas from the 2016 through 2024 model years.

And investors sent company shares tumbling last month after Tesla unveiled its long-awaited robotaxi at a Hollywood studio Thursday night, seeing not much progress at Tesla on autonomous vehicles while other companies have been making notable progress.

TORONTO – Canada’s main stock index was up more than 100 points in late-morning trading, helped by strength in base metal and utility stocks, while U.S. stock markets were mixed.

The S&P/TSX composite index was up 103.40 points at 24,542.48.

In New York, the Dow Jones industrial average was up 192.31 points at 42,932.73. The S&P 500 index was up 7.14 points at 5,822.40, while the Nasdaq composite was down 9.03 points at 18,306.56.

The Canadian dollar traded for 72.61 cents US compared with 72.44 cents US on Tuesday.

The November crude oil contract was down 71 cents at US$69.87 per barrel and the November natural gas contract was down eight cents at US$2.42 per mmBTU.

The December gold contract was up US$7.20 at US$2,686.10 an ounce and the December copper contract was up a penny at US$4.35 a pound.

This report by The Canadian Press was first published Oct. 16, 2024.

TORONTO – Canada’s main stock index was up more than 200 points in late-morning trading, while U.S. stock markets were also headed higher.

The S&P/TSX composite index was up 205.86 points at 24,508.12.

In New York, the Dow Jones industrial average was up 336.62 points at 42,790.74. The S&P 500 index was up 34.19 points at 5,814.24, while the Nasdaq composite was up 60.27 points at 18.342.32.

The Canadian dollar traded for 72.61 cents US compared with 72.71 cents US on Thursday.

The November crude oil contract was down 15 cents at US$75.70 per barrel and the November natural gas contract was down two cents at US$2.65 per mmBTU.

The December gold contract was down US$29.60 at US$2,668.90 an ounce and the December copper contract was up four cents at US$4.47 a pound.

This report by The Canadian Press was first published Oct. 11, 2024.