The world economy’s rebound from the depths of the coronavirus crisis is fading, setting up an uncertain finish to the year.

The concerns are multiple. The coming northern winter may trigger another wave of the virus as the wait for a vaccine continues. Government support for furloughed workers and bank moratoriums on loan repayments are set to expire. Strains between the U.S. and China could get worse in the run-up to November’s presidential election, and undermine business confidence.

“We have seen peak rebound,” Joachim Fels, global economic adviser at Pacific Investment Management Co., told Bloomberg Television. “From now on, the momentum is fading a little bit.”

That sets up a delicate balancing act for governments. They’ve injected almost $20 trillion in fiscal and monetary support, in an effort to get the economy as far back to normal as is feasible in a pandemic, and can point to plenty of successes.

In the U.S., unemployment fell sharply in August and the housing market has been a bright spot. China’s steady recovery is cited by optimists as a guide to where the rest of the world is headed, while Germany is posting some decent industrial data too. And emerging markets are getting a breather from the dollar’s decline.

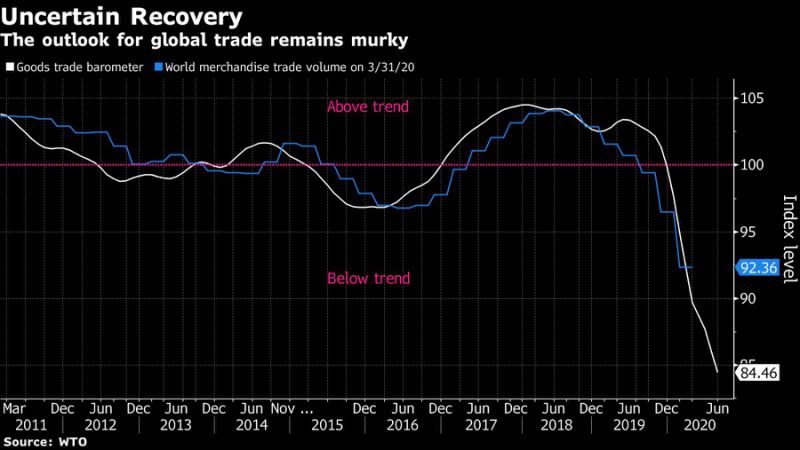

Long Slog

But keeping up the momentum on all these fronts won’t be easy. It would likely require policy makers to top up their stimulus efforts, at a point when some are looking to cut back instead. And for all the scientific progress with vaccines, they won’t be available anytime soon on the scale needed to bring the virus under tight control — a key condition for business-as-usual.

Meanwhile, there are headwinds. On labor markets, for example, government aid helped to drive an initial rebound — which may have been the easy part. Next up is the long slog of retooling businesses, reallocating resources, and retraining workers in industries that are no longer viable. That kind of restructuring could play out for some time.

Already this month, some of the world’s best known industrial brands have signaled job cuts are on the way.

A.P. Moller-Maersk A/S is planning a major overhaul that’s set to affect thousands at the world’s biggest container shipping company. Ford Motor Co. is cutting about 5% of its U.S. salaried workers, and United Airlines Holdings Inc. will eliminate 16,000 jobs next month as it shrinks operations.

There are other worrying signs too.

In China, which contained the virus months ago, consumers remain reluctant to spend and the nation’s biggest banks just posted their worst profit declines in more than a decade as bad debt ballooned.

U.S. lawmakers continue to haggle over more fiscal stimulus, which may be needed to sustain the recovery in the world’s largest economy.

Adding 1.4 million jobs in August was “a big step in the right direction,” said Ryan Sweet, head of monetary policy research at Moody’s Analytics. But the economy needs to maintain that kind of pace, he said, and “without fiscal stimulus that will be hard to do.”

‘Not Looking Good’

In Europe, gauges of activity are fading, and factories are trying to cut costs as weak demand and price cuts squeeze profit margins. While France and Germany have extended their furlough programs, the U.K. plans to end its version in October, potentially putting millions of jobs at risk.

Japanese Prime Minister Shinzo Abe, who announced his resignation last month on health grounds, warned in a press conference that “winter is coming” and the nation will need to gird to contain the virus.

What Bloomberg’s Economists Say

“High-frequency data paints a picture of a rapid rebound in the second quarter, and a stall – with activity still well short of pre-virus levels – in the third. There’s scope for further gains. If the U.S. did as well as Germany at containing the virus and getting back to work – for example – that would be a significant positive. To get back to pre-virus normality, a vaccine is required.”

–Tom Orlik, chief economist. Read more here

Stock markets are vulnerable to disappointment in economic numbers in the coming months amid a gradual curbing of emergency fiscal support.

“In terms of valuations, we’ve got to look beyond just what happened this week to the longer term,” said Catherine Mann, global chief economist at Citigroup Inc. “And the longer term is not looking good right now in terms of support for consumption, and therefore business investment and growth in the U.S. economy.”

Overshadowing everything is the continued spread of the virus, with flare-ups around the world.

Even when a vaccine is devised, making it available worldwide on the necessary scale is going to take time, according to Warwick McKibbin of the Brookings Institution and Australia National University. His models suggest that the virus could cost the world economy some $35 trillion through 2025.

“You have to get quite a lot of the population vaccinated before the economic costs start to come down,” he said.

<p class="canvas-atom canvas-text Mb(1.0em) Mb(0)–sm Mt(0.8em)–sm" type="text" content="For more articles like this, please visit us at bloomberg.com” data-reactid=”58″>For more articles like this, please visit us at bloomberg.com

<p class="canvas-atom canvas-text Mb(1.0em) Mb(0)–sm Mt(0.8em)–sm" type="text" content="Subscribe now to stay ahead with the most trusted business news source.” data-reactid=”59″>Subscribe now to stay ahead with the most trusted business news source.

OTTAWA – Canada’s unemployment rate held steady at 6.5 per cent last month as hiring remained weak across the economy.

Statistics Canada’s labour force survey on Friday said employment rose by a modest 15,000 jobs in October.

Business, building and support services saw the largest gain in employment.

Meanwhile, finance, insurance, real estate, rental and leasing experienced the largest decline.

Many economists see weakness in the job market continuing in the short term, before the Bank of Canada’s interest rate cuts spark a rebound in economic growth next year.

Despite ongoing softness in the labour market, however, strong wage growth has raged on in Canada. Average hourly wages in October grew 4.9 per cent from a year ago, reaching $35.76.

Friday’s report also shed some light on the financial health of households.

According to the agency, 28.8 per cent of Canadians aged 15 or older were living in a household that had difficulty meeting financial needs – like food and housing – in the previous four weeks.

That was down from 33.1 per cent in October 2023 and 35.5 per cent in October 2022, but still above the 20.4 per cent figure recorded in October 2020.

People living in a rented home were more likely to report difficulty meeting financial needs, with nearly four in 10 reporting that was the case.

That compares with just under a quarter of those living in an owned home by a household member.

Immigrants were also more likely to report facing financial strain last month, with about four out of 10 immigrants who landed in the last year doing so.

That compares with about three in 10 more established immigrants and one in four of people born in Canada.

This report by The Canadian Press was first published Nov. 8, 2024.

The Canadian Institute for Health Information says health-care spending in Canada is projected to reach a new high in 2024.

The annual report released Thursday says total health spending is expected to hit $372 billion, or $9,054 per Canadian.

CIHI’s national analysis predicts expenditures will rise by 5.7 per cent in 2024, compared to 4.5 per cent in 2023 and 1.7 per cent in 2022.

This year’s health spending is estimated to represent 12.4 per cent of Canada’s gross domestic product. Excluding two years of the pandemic, it would be the highest ratio in the country’s history.

While it’s not unusual for health expenditures to outpace economic growth, the report says this could be the case for the next several years due to Canada’s growing population and its aging demographic.

Canada’s per capita spending on health care in 2022 was among the highest in the world, but still less than countries such as the United States and Sweden.

The report notes that the Canadian dental and pharmacare plans could push health-care spending even further as more people who previously couldn’t afford these services start using them.

This report by The Canadian Press was first published Nov. 7, 2024.

Canadian Press health coverage receives support through a partnership with the Canadian Medical Association. CP is solely responsible for this content.

As Canadians wake up to news that Donald Trump will return to the White House, the president-elect’s protectionist stance is casting a spotlight on what effect his second term will have on Canada-U.S. economic ties.

Some Canadian business leaders have expressed worry over Trump’s promise to introduce a universal 10 per cent tariff on all American imports.

A Canadian Chamber of Commerce report released last month suggested those tariffs would shrink the Canadian economy, resulting in around $30 billion per year in economic costs.

More than 77 per cent of Canadian exports go to the U.S.

Canada’s manufacturing sector faces the biggest risk should Trump push forward on imposing broad tariffs, said Canadian Manufacturers and Exporters president and CEO Dennis Darby. He said the sector is the “most trade-exposed” within Canada.

“It’s in the U.S.’s best interest, it’s in our best interest, but most importantly for consumers across North America, that we’re able to trade goods, materials, ingredients, as we have under the trade agreements,” Darby said in an interview.

“It’s a more complex or complicated outcome than it would have been with the Democrats, but we’ve had to deal with this before and we’re going to do our best to deal with it again.”

American economists have also warned Trump’s plan could cause inflation and possibly a recession, which could have ripple effects in Canada.

It’s consumers who will ultimately feel the burden of any inflationary effect caused by broad tariffs, said Darby.

“A tariff tends to raise costs, and it ultimately raises prices, so that’s something that we have to be prepared for,” he said.

“It could tilt production mandates. A tariff makes goods more expensive, but on the same token, it also will make inputs for the U.S. more expensive.”

A report last month by TD economist Marc Ercolao said research shows a full-scale implementation of Trump’s tariff plan could lead to a near-five per cent reduction in Canadian export volumes to the U.S. by early-2027, relative to current baseline forecasts.

Retaliation by Canada would also increase costs for domestic producers, and push import volumes lower in the process.

“Slowing import activity mitigates some of the negative net trade impact on total GDP enough to avoid a technical recession, but still produces a period of extended stagnation through 2025 and 2026,” Ercolao said.

Since the Canada-United States-Mexico Agreement came into effect in 2020, trade between Canada and the U.S. has surged by 46 per cent, according to the Toronto Region Board of Trade.

With that deal is up for review in 2026, Canadian Chamber of Commerce president and CEO Candace Laing said the Canadian government “must collaborate effectively with the Trump administration to preserve and strengthen our bilateral economic partnership.”

“With an impressive $3.6 billion in daily trade, Canada and the United States are each other’s closest international partners. The secure and efficient flow of goods and people across our border … remains essential for the economies of both countries,” she said in a statement.

“By resisting tariffs and trade barriers that will only raise prices and hurt consumers in both countries, Canada and the United States can strengthen resilient cross-border supply chains that enhance our shared economic security.”

This report by The Canadian Press was first published Nov. 6, 2024.