Stocks made new record highs, with the S&P 500 reaching a closing high of 4,894.16 on Thursday and an intraday high of 4,906.69 on Friday. For the week, the S&P rose 1.1% to close at 4,890.97. The index is now up 2.5% year to date and up 36.7% from its October 12, 2022 closing low of 3,577.03.

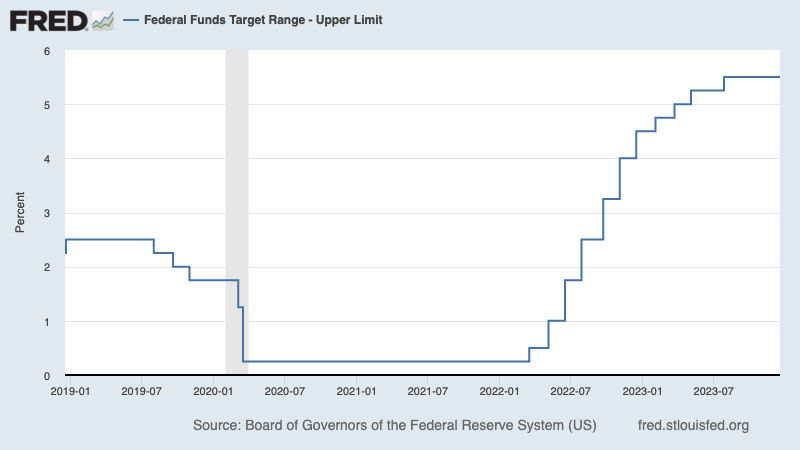

One of the hottest debates in the markets right now is if and when the Federal Reserve will pivot from its very hawkish stance and start cutting interest rates.

For a while, futures traders were betting that the first rate cut would come with the monetary policy meeting this coming March. But more recently, those bets have been pared back with traders now assigning a 47% chance of a March rate cut, down from 83% a month ago.

A popular view is that rate cuts would be bullish for risk assets like stocks. So any developments that lower the odds of a rate cut in the near term would therefore be bearish. All other things being equal, this view makes sense.

The world has changed since Fed rate decisions were a much bigger deal

I’m no monetary policy economist. But as I discussed on the Investopedia Express podcast earlier this month, I think concerns about the Fed’s next move on interest rates are a bit overblown.

First of all, we’re talking about a potential 25-basis-point cut from a range of 5.25% to 5.5%. Sure, that’s not insignificant. But that’s nowhere near as big a deal as it was when we were talking about 25-, 50-, and 75-basis-point rate hikes from near 0%.

In other words, the stakes for the upcoming Fed policy meetings aren’t nearly as high as they were in 2022 and 2023.

Third, we have to keep in mind that rate cuts and rate hikes — in and of themselves — aren’t the real issue. Rather, they represent reactions to real issues.

Putting it another way, whether or not the Fed cuts rates is not the right question. Here’s an excerpt of what I said to Investopedia’s Caleb Silver earlier this month:

… As far as whether or not they actually pivot and begin to cut or hold or whatever, I think that’s really not the right question. The question [should] be, “If they don’t cut, then why are they not cutting as they suggested in their dot plots?” Right? Is it possible that the economy heats up more than they initially modeled? Yeah, maybe that’s a good reason to not cut because they’re concerned that inflation is going to be bubbling up again.From an investor perspective and from an economic perspective, that’s not exactly the worst thing in the world that the economy isn’t falling apart. Because remember, a lot of these assumptions when it comes to the Fed pivot, in addition to inflation cooling, are also tied to the idea that the economy is also cooling — that growth is slowing and decelerating and that a lot of people have recessions on their mind. So maybe the Fed doesn’t pivot because the economy’s picking up? That’s really not that big a deal.

To reiterate, the Fed’s projection that it would cut rates in 2024 was accompanied by assumptions that economic growth would slow significantly and inflation rates would take another leg lower during the year.

That’s to say if the Fed were to change its outlook for rate cuts, it may also be the case that its outlook for the economy and inflation have changed as well.

Economic reality is proving stronger than expected

Also on Thursday, we learned orders for nondefense capital goods excluding aircraft — a.k.a. core capex or business investment — rose 0.3% to a record $74.33 billion in December.

Core capex orders are a leading indicator, meaning they foretell economic activity. While the growth rate has leveled off a bit, they continue to signal economic strength in the months to come.

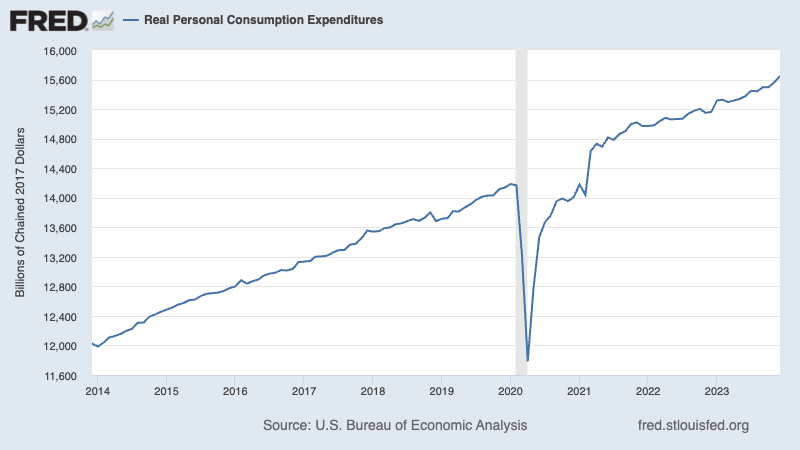

On Friday, we learned personal consumption expenditures — which represents about 69% of GDP — increased 0.7% month over month in December to a record annual rate of $19.0 trillion.

The confluence of data we’ve gotten over the past several weeks suggest economic activity is tracking stronger than many expected.

Of course, the worry is that hot economic activity could fan the flames of inflation again, which would explain why those rate hike odds are coming down — traders are betting that the Fed will keep monetary policy tighter for longer to rein in the economy to contain inflation risks.

But on balance, all this is not necessarily a bad thing.

Importantly, the stock market rallied for much of the year, with the S&P 500 surging 24%.

The bottom line

I think we’ll probably continue to hear pundits warn that rate-cut odds are coming down and argue this is bearish for stocks.

But before buying into that argument, we have to understand the economic circumstances that would cause the Fed to put off rate cuts.

If it’s because the economy is proving to be stronger than expected, then it’s no sure thing that keeping monetary policy tight is necessarily bad news — as we learned all of last year. By the way, it is the case that the economy has been proving stronger than expected as inflation rates continue to cool. And even as the odds of a rate cut have declined, the S&P 500 has been hitting fresh record highs.

And amid all this, the debate is over a relatively small move in the Fed’s benchmark interest rate. That is to say maybe the Fed’s next move just isn’t that big of a deal.

As always, context matters — especially when we’re thinking about developments that appear bullish or bearish for stocks.

One more quick thought

While we’re on the subject, we should also consider the possible scenario the Fed begins cutting rates because the economy takes a significant turn for the worse. As Carson Group’s Ryan Detrick observed, rate cuts that were intended to stimulate the economy amid a recession came with the S&P 500 falling an average of 11.6% in the year that followed.

This is a scenario where the rising odds of a rate cut is not necessarily a bullish signal. Another reminder that context matters.

Reviewing the macro crosscurrents

There were a few notable data points and macroeconomic developments from last week to consider:

Inflation rates cools. The personal consumption expenditures (PCE) price index in December was up 2.6% from a year ago, unchanged from November’s level. The core PCE price index — the Federal Reserve’s preferred measure of inflation — was up 2.9% during the month after coming in at 3.2% higher in the prior month.

On a month over month basis, the core PCE price index was up 0.2%, up slightly from the prior month’s print of 0.1%. If you annualized the rolling three-month and six-month figures, the core PCE price index was up 1.5% and 1.9%, respectively.

While inflation rates are beginning to hover near the Federal Reserve’s target rate of 2%, the central bank has indicated that it wants prices to stay cool for a little while before it is comfortable confident inflation is under control. So even though there may not be more rate hikes and rate cuts may be around the corner, rates are likely to be kept high for a while.

Consumers are spending. According to BEA data, personal consumption expenditures increased 0.7% month over month in December to a record annual rate of $19.0 trillion.

Adjusted for inflation, real personal consumption expenditures also rose to a new record.

Spending cooled with the cold. From BofA: “Total card spending per HH was down 3.0% y/y in the week ending Jan 20, according to BAC aggregated credit & debit card data. Total card spending in the South & MW was likely the most impacted by cold weather while NE spending showed some recovery y/y. Overall, spending on discretionary services – entertainment, restaurants, lodging and airlines – was the most affected.”

Watching layoffs. From BofA: “Despite some layoff announcement recently, both the size and frequency have been falling (Exhibit 19). Layoff announcements from Banks were also fairly muted vs. last year, other than Citi (restructuring).”

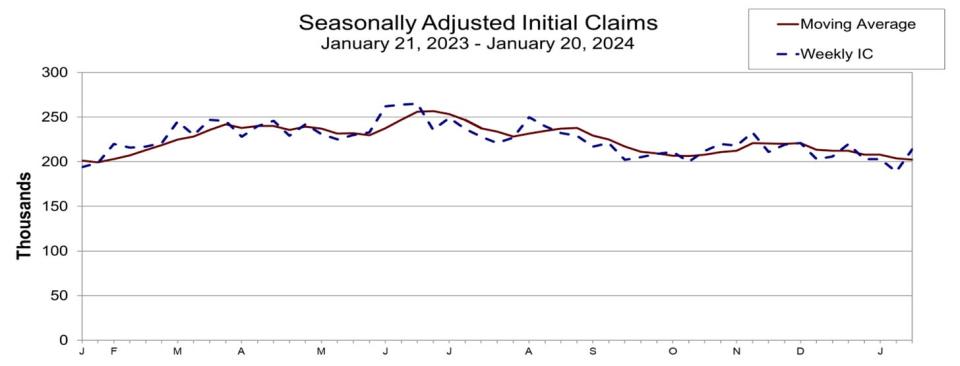

Unemployment claims rise. Initial claims for unemployment benefits increased to 214,000 during the week ending January 20, up from 189,000 the week prior. This is above the September 2022 low of 182,000, but it continues to trend at levels historically associated with economic growth.

Gas prices tick up. From AAA: “After making a brief weekend trip to $3.07, the national average for gas edged higher by one penny since last week to $3.10. The meandering journey is likely caused by low gas demand countered by slightly higher costs for oil. The result is a pump price stalemate.”

People are driving. Weekly EIA data through January 19 show gasoline demand is up from a year ago.

From DataTrek Research co-founder Nicholas Colas: “Lower oil/gas prices are an underappreciated economic tailwind as we start 2024. These not only tend to help consumer confidence but also reduce inflationary pressures on the American economy as a whole.”

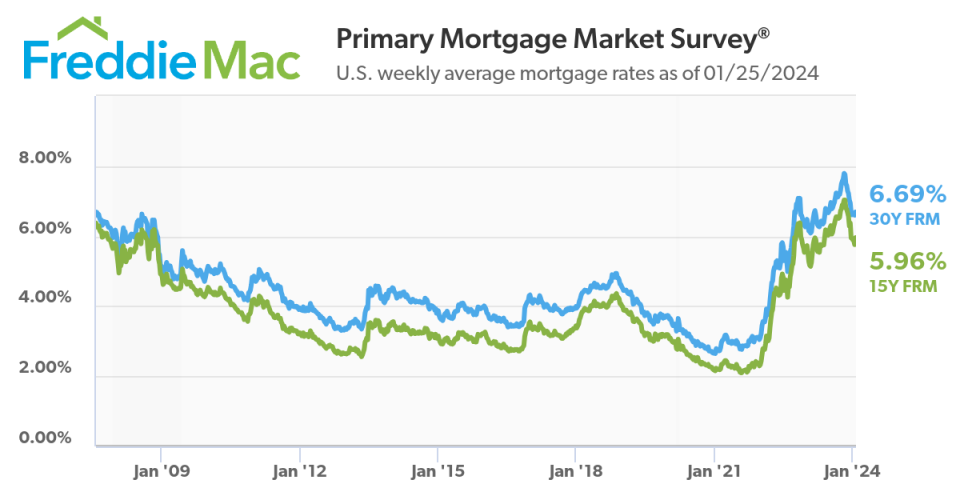

Mortgage rates tick up. According to Freddie Mac, the average 30-year fixed-rate mortgage rose to 6.69% from 6.60% the week prior. From Freddie Mac: “Mortgage rates decreased this week, reaching their lowest level since May of 2023. This is an encouraging development for the housing market and in particular first-time homebuyers who are sensitive to changes in housing affordability. However, as purchase demand continues to thaw, it will put more pressure on already depleted inventory for sale.”

Survey signals growth pickup. From S&P Global’s January U.S. PMI: “An encouraging start to the year is indicated for the U.S. economy by the flash PMI data, with companies reporting a marked acceleration of growth alongside a sharp cooling of inflation pressures. Output measured across both goods and services rose in January at the fastest rate since last June, growth momentum having stepped up a gear on the back of improved demand conditions. New orders inflows have now picked up for three months, buoyed in particular by improving sales to domestic customers, helping lift business confidence about the year ahead to the most optimistic since May 2022.”

Business investment activity is strong. Orders for nondefense capital goods excluding aircraft — a.k.a. core capex or business investment — rose 0.3% to a record $74.33 billion in December.

Core capex orders are a leading indicator, meaning they foretell economic activity down the road. While the growth rate has leveled off a bit, they continue to signal economic strength in the months to come.

Most U.S. states are still growing. From the Philly Fed’s December State Coincident Indexes report: “Over the past three months, the indexes increased in 25 states, decreased in 22 states, and remained stable in three, for a three-month diffusion index of 6. Additionally, in the past month, the indexes increased in 26 states, decreased in 16 states, and remained stable in eight, for a one-month diffusion index of 20.”

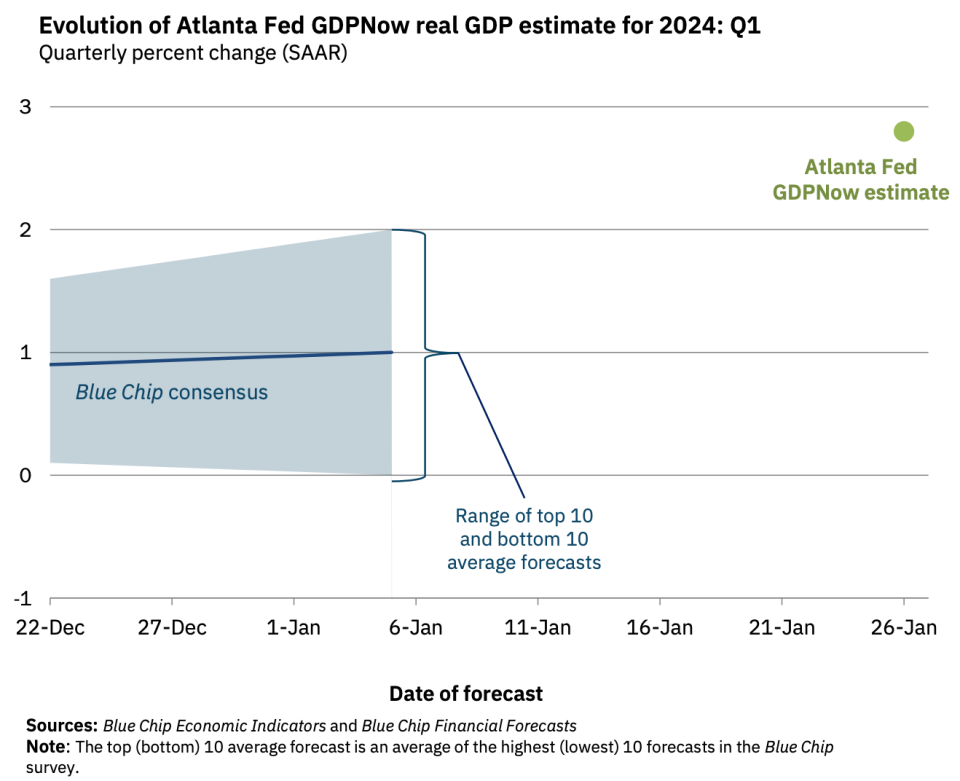

Near-term GDP growth estimates look good. The Atlanta Fed’s GDPNow model sees real GDP growth climbing at a 3.0% rate in Q1.

This comes as the Federal Reserve continues to employ very tight monetary policy in its ongoing effort to bring inflation down. While it’s true that the Fed has taken a less hawkish tone in 2023 than in 2022, and that most economists agree that the final interest rate hike of the cycle has either already happened or is near, inflation still has to cool more and stay cool for a little while before the central bank is comfortable with price stability.

TORONTO – Roots Corp. may have built its brand on all things comfy and cosy, but its CEO says activewear is now “really becoming a core part” of the brand.

The category, which at Roots spans leggings, tracksuits, sports bras and bike shorts, has seen such sustained double-digit growth that Meghan Roach plans to make it a key part of the business’ future.

“It’s an area … you will see us continue to expand upon,” she told analysts on a Friday call.

The Toronto-based retailer’s push into activewear has taken shape over many years and included several turns as the official designer and supplier of Team Canada’s Olympic uniform.

But consumers have had plenty of choice when it comes to workout gear and other apparel suited to their sporting needs. On top of the slew of athletic brands like Nike and Adidas, shoppers have also gravitated toward Lululemon Athletica Inc., Alo and Vuori, ramping up competition in the activewear category.

Roach feels Roots’ toehold in the category stems from the fit, feel and following its merchandise has cultivated.

“Our product really resonates with (shoppers) because you can wear it through multiple different use cases and occasions,” she said.

“We’ve been seeing customers come back again and again for some of these core products in our activewear collection.”

Her remarks came the same day as Roots revealed it lost $5.2 million in its latest quarter compared with a loss of $5.3 million in the same quarter last year.

The company said the second-quarter loss amounted to 13 cents per diluted share for the quarter ended Aug. 3, the same as a year earlier.

In presenting the results, Roach reminded analysts that the first half of the year is usually “seasonally small,” representing just 30 per cent of the company’s annual sales.

Sales for the second quarter totalled $47.7 million, down from $49.4 million in the same quarter last year.

The move lower came as direct-to-consumer sales amounted to $36.4 million, down from $37.1 million a year earlier, as comparable sales edged down 0.2 per cent.

The numbers reflect the fact that Roots continued to grapple with inventory challenges in the company’s Cooper fleece line that first cropped up in its previous quarter.

Roots recently began to use artificial intelligence to assist with daily inventory replenishments and said more tools helping with allocation will go live in the next quarter.

Beyond that time period, the company intends to keep exploring AI and renovate more of its stores.

It will also re-evaluate its design ranks.

Roots announced Friday that chief product officer Karuna Scheinfeld has stepped down.

Rather than fill the role, the company plans to hire senior level design talent with international experience in the outdoor and activewear sectors who will take on tasks previously done by the chief product officer.

This report by The Canadian Press was first published Sept. 13, 2024.

VANCOUVER – Mediated talks between the union representing HandyDART workers in Metro Vancouver and its employer, Transdev, are set to resume today as a strike that has stopped most services drags into a second week.

No timeline has been set for the length of the negotiations, but Joe McCann, president of the Amalgamated Transit Union Local 1724, says they are willing to stay there as long as it takes, even if talks drag on all night.

About 600 employees of the door-to-door transit service for people unable to navigate the conventional transit system have been on strike since last Tuesday, pausing service for all but essential medical trips.

Hundreds of drivers rallied outside TransLink’s head office earlier this week, calling for the transportation provider to intervene in the dispute with Transdev, which was contracted to oversee HandyDART service.

Transdev said earlier this week that it will provide a reply to the union’s latest proposal on Thursday.

A statement from the company said it “strongly believes” that their employees deserve fair wages, and that a fair contract “must balance the needs of their employees, clients and taxpayers.”

This report by The Canadian Press was first published Sept. 12, 2024.

MONTREAL – Travel company Transat AT Inc. reported a loss in its latest quarter compared with a profit a year earlier as its revenue edged lower.

The parent company of Air Transat says it lost $39.9 million or $1.03 per diluted share in its quarter ended July 31.

The result compared with a profit of $57.3 million or $1.49 per diluted share a year earlier.

Revenue in what was the company’s third quarter totalled $736.2 million, down from $746.3 million in the same quarter last year.

On an adjusted basis, Transat says it lost $1.10 per share in its latest quarter compared with an adjusted profit of $1.10 per share a year earlier.

Transat chief executive Annick Guérard says demand for leisure travel remains healthy, as evidenced by higher traffic, but consumers are increasingly price conscious given the current economic uncertainty.

This report by The Canadian Press was first published Sept. 12, 2024.