At Labour’s 2021 conference, shadow chancellor Rachel Reeves announced her ambition to be the UK’s first “green” chancellor.

To stress her bona fides, she pledged to invest £28bn a year, every year to 2030 to “green” the economy.

Labour’s Green Prosperity Plan was one of its defining policies. It gave the party a clear dividing line with government.

Ms Reeves said there would be “no dither, and no delay” in tackling the climate crisis.

It was also an answer to the government’s “levelling up” pledge.

The borrowed cash would underpin well-paid jobs in every corner of the UK in the energy sector.

So why has Ms Reeves kicked the pledge into the second half of the next Parliament, if Labour wins?

The first reason is obvious.

Ms Reeves now says she was “green” – in a different sense of the word – in 2021, in that she hadn’t foreseen what then-Prime Minister Liz Truss would do to the economy.

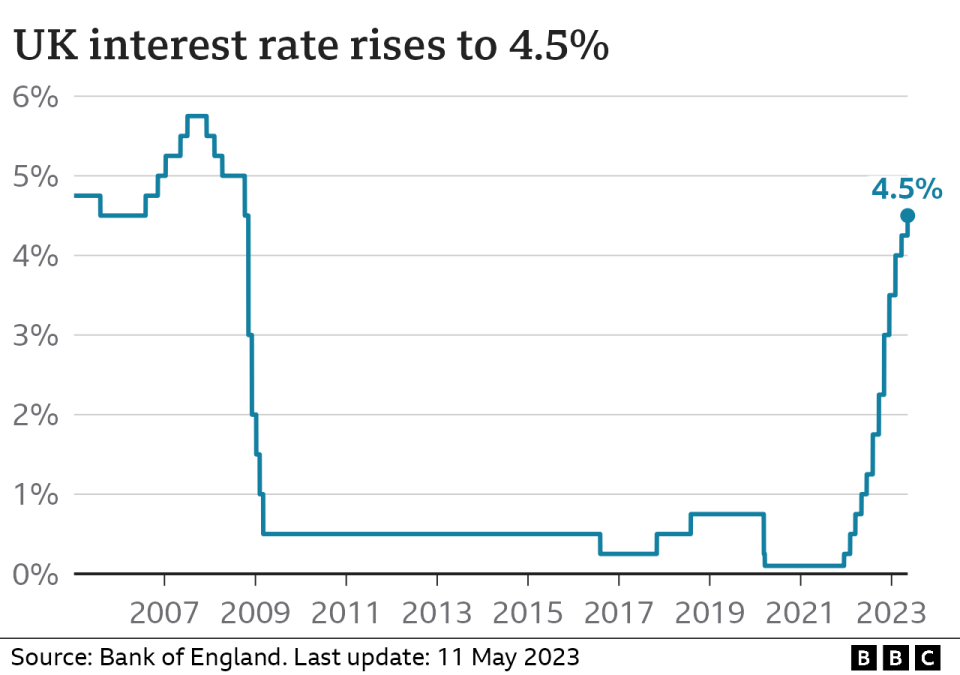

With interest rates up, the cost of borrowing rises too, making the £28bn pledge more expensive to deliver.

And Ms Reeves wants to emphasise that if any spending commitments clash with her fiscal rules, the rules would win every time.

But did the £28bn green pledge really clash with her rules?

In their own detailed briefing on their fiscal rules, Labour said: “It is essential that for our future prosperity that we retain the ability to borrow for investing in capital projects which over time will pay for themselves.

“And that is why our target for eliminating the deficit excludes investment.”

So borrowing to invest in the future technology and jobs shouldn’t fall foul of that fiscal rule.

Chart showing interest rate rises (May 2023)

But there is another rule which Ms Reeves cited this morning – to have debt falling as a percentage of GDP or Gross Domestic Product, a measure of economic activity.

Meeting that rule may have contributed to putting the £28bn on the backburner – though I remember at the 2021 conference some senior Labour figures questioning the wisdom of borrowing the equivalent of half the defence budget every year even then.

And some senior figures in Labour are far less convinced that £28bn would necessarily bust the debt rule – economic forecasts can change by far greater margins.

One of the other justifications for the change of position is that £28bn shouldn’t be poured in to the economy straight away.

That’s because it will take time to train workers, to create and bolster supply chains. Hence “ramping up” to £28bn.

One shadow minister said that while today’s announcement felt like a bit of a handbrake turn, it was nonetheless inevitable and sensible.

The scale of the ambition remained the same, but pragmatically the shadow chancellor was simply not committing to spending which would be difficult to deliver.

But all this must have been known in 2021, too.

So why announce the U-turn today?

The change of position was discussed within Labour’s Treasury team for some time.

Engagement with investors convinced them the government itself may not need to pump in a huge amount of cash straight away – the private sector would provide green jobs without state help.

And while Ms Reeves has ditched the £28bn pledge in the first half of the Parliament, this doesn’t mean that a Labour government would spend nothing on its Green Prosperity Plan.

I understand cash will be prioritised for projects where the private sector would not commit without state assistance – nuclear and hydrogen for example.

But it seems clear that politics and not just economics played a role in today’s announcement.

Tory attacks

There have been grumbles and growls over how the policy has landed over the past two years within Labour’s ranks and internal criticism has increased, not receded.

One concern was that the amount to be borrowed – the £28bn – was better known than what the money would buy – from home insulation and heat pumps to new carbon capture technology.

But it was crystal clear this week that the Conservatives felt that they had seen a vulnerability that could be exploited.

The front page of the Daily Mail blared this week about the alleged dangers of the policy – the extra borrowing would put up interest and therefore mortgage costs.

The independent Institute for Fiscal Studies was also being cited by Conservative ministers.

Its director Paul Johnson had warned that while additional borrowing would pump money in to the economy, it also drives up interest rates.

As Labour has been attacking the Conservatives for their handling of the economy, and the “mortgage premium” they claim the government has caused, it was understandable that they did not want the same attack to be aimed at them, and Ms Reeves this morning sought to eliminate a potential negative.

As one Labour shadow minister put it: “They [the Conservatives] will be pulling their hair out that one of their attack lines has failed.”

Some in Labour’s ranks, though, believe the party should have insulated (no pun intended) itself from attack by making the case more stridently that borrowing to invest is different from borrowing to meet day-to-day spending.

Credibility is key

Labour’s opinion poll lead is wide but pessimists in their ranks fear it is shallow.

Establishing economic credibility is seen as key.

But while it may have been the lesser of two evils, today’s change of tack isn’t cost-free.

The party has committed to achieve a net-zero power system by 2030.

But with potentially significantly less investment, is this target in danger too?

And unlike many of the left-wing commitments that have been ditched – where the leadership don’t really mind the backlash – this was the shadow chancellor watering down her own highest-profile pledge.

That in itself has allowed the Conservatives to shout about Labour’s economic plans being “in tatters”.

As Labour is still committed to its Green Prosperity Plan – just not the original timescale – they will still claim they have clear dividing lines with the government.

But one of their key arguments has been this: With the US pouring subsidies in to domestic green industries, the UK will get left behind if it doesn’t follow suit. And fast.

A delay doesn’t destroy – but it does potentially weaken – the Labour case.

But there is another concern amongst those who are most certainly not on the Corbyn left.

Emphasising competence and fiscal credibility over climate change commitments could leave some target voters cold.

NEW YORK (AP) — Shares of Tesla soared Wednesday as investors bet that the electric vehicle maker and its CEO Elon Musk will benefit from Donald Trump’s return to the White House.

Tesla stands to make significant gains under a Trump administration with the threat of diminished subsidies for alternative energy and electric vehicles doing the most harm to smaller competitors. Trump’s plans for extensive tariffs on Chinese imports make it less likely that Chinese EVs will be sold in bulk in the U.S. anytime soon.

“Tesla has the scale and scope that is unmatched,” said Wedbush analyst Dan Ives, in a note to investors. “This dynamic could give Musk and Tesla a clear competitive advantage in a non-EV subsidy environment, coupled by likely higher China tariffs that would continue to push away cheaper Chinese EV players.”

Tesla shares jumped 14.8% Wednesday while shares of rival electric vehicle makers tumbled. Nio, based in Shanghai, fell 5.3%. Shares of electric truck maker Rivian dropped 8.3% and Lucid Group fell 5.3%.

Tesla dominates sales of electric vehicles in the U.S, with 48.9% in market share through the middle of 2024, according to the U.S. Energy Information Administration.

Subsidies for clean energy are part of the Inflation Reduction Act, signed into law by President Joe Biden in 2022. It included tax credits for manufacturing, along with tax credits for consumers of electric vehicles.

Musk was one of Trump’s biggest donors, spending at least $119 million mobilizing Trump’s supporters to back the Republican nominee. He also pledged to give away $1 million a day to voters signing a petition for his political action committee.

In some ways, it has been a rocky year for Tesla, with sales and profit declining through the first half of the year. Profit did rise 17.3% in the third quarter.

The U.S. opened an investigation into the company’s “Full Self-Driving” system after reports of crashes in low-visibility conditions, including one that killed a pedestrian. The investigation covers roughly 2.4 million Teslas from the 2016 through 2024 model years.

And investors sent company shares tumbling last month after Tesla unveiled its long-awaited robotaxi at a Hollywood studio Thursday night, seeing not much progress at Tesla on autonomous vehicles while other companies have been making notable progress.

TORONTO – Canada’s main stock index was up more than 100 points in late-morning trading, helped by strength in base metal and utility stocks, while U.S. stock markets were mixed.

The S&P/TSX composite index was up 103.40 points at 24,542.48.

In New York, the Dow Jones industrial average was up 192.31 points at 42,932.73. The S&P 500 index was up 7.14 points at 5,822.40, while the Nasdaq composite was down 9.03 points at 18,306.56.

The Canadian dollar traded for 72.61 cents US compared with 72.44 cents US on Tuesday.

The November crude oil contract was down 71 cents at US$69.87 per barrel and the November natural gas contract was down eight cents at US$2.42 per mmBTU.

The December gold contract was up US$7.20 at US$2,686.10 an ounce and the December copper contract was up a penny at US$4.35 a pound.

This report by The Canadian Press was first published Oct. 16, 2024.

TORONTO – Canada’s main stock index was up more than 200 points in late-morning trading, while U.S. stock markets were also headed higher.

The S&P/TSX composite index was up 205.86 points at 24,508.12.

In New York, the Dow Jones industrial average was up 336.62 points at 42,790.74. The S&P 500 index was up 34.19 points at 5,814.24, while the Nasdaq composite was up 60.27 points at 18.342.32.

The Canadian dollar traded for 72.61 cents US compared with 72.71 cents US on Thursday.

The November crude oil contract was down 15 cents at US$75.70 per barrel and the November natural gas contract was down two cents at US$2.65 per mmBTU.

The December gold contract was down US$29.60 at US$2,668.90 an ounce and the December copper contract was up four cents at US$4.47 a pound.

This report by The Canadian Press was first published Oct. 11, 2024.