The global economy is entering the final quarter of its worst year in living memory in a precarious state with the coronavirus threatening to wreak yet more destruction on labor markets.

The darkening outlook for U.S. employment, the impending halt to a U.K. furlough and the expiry of a moratorium on German insolvencies provide a glimpse of the trouble in store. The International Labour Organisation estimated recently that the world would lose working hours equivalent to 245 million full-time jobs in the last three months of 2020.

The quarter began with a portent as blue-chip employers from Walt Disney Co. to Royal Dutch Shell Plc and Continental AG announced tens of thousands of staff cuts within a 24-hour period. Then on Friday, the U.S. Labor Department revealed slowing job gains in September, with many Americans giving up on looking for work.

Adding to those omens, the U.K.’s main furlough program will end later this month, and a group representing the country’s events industry predicts more than 90,000 people will be made redundant in coming weeks.

Renewed clusters of infections underscore the vulnerability of already battered economies to further damage that could ultimately hit livelihoods. The latest outbreak in Paris may force bars and restaurants to close, while London is at a “tipping point,” according to a local health official.

What Bloomberg’s Economists Say…

“A second wave of infections, major corporate layoffs in the U.S. and the end of the furlough scheme in the U.K. flag the risk unemployment will rise into year-end. Bad news for the immediate outlook is also bad news for the medium term, with deeper labor market scars threatening to drag on the recovery — even after a Covid-19 vaccine is eventually found.”

–Tom Orlik, chief economist

Click here for what happened last week and below is our wrap of what is coming up in the global economy.

U.S. and Canada

On Wednesday, the Federal Reserve will release minutes of its Sept. 15-16 meeting of the Federal Open Market Committee. It could be especially fruitful for Fed watchers, beginning with details of the debate over the committee’s new guidance on the conditions that will be necessary to trigger a rate increase.

The minutes may also reveal whether policy makers discussed increasing asset purchases and continuing to restrict bank dividends. There may also be a separate section summarizing discussions that preceded a special Aug. 27 vote on the new framework, under which the Fed will allow inflation to run higher and unemployment to go lower than officials previously had tolerated.

In terms of economic data, traders will be looking at the latest reports on trade and the weekly jobless claims.

In Canada, Bank of Canada Governor Tiff Macklem is set to speak Thursday and the jobs report for September is due Friday.

Asia

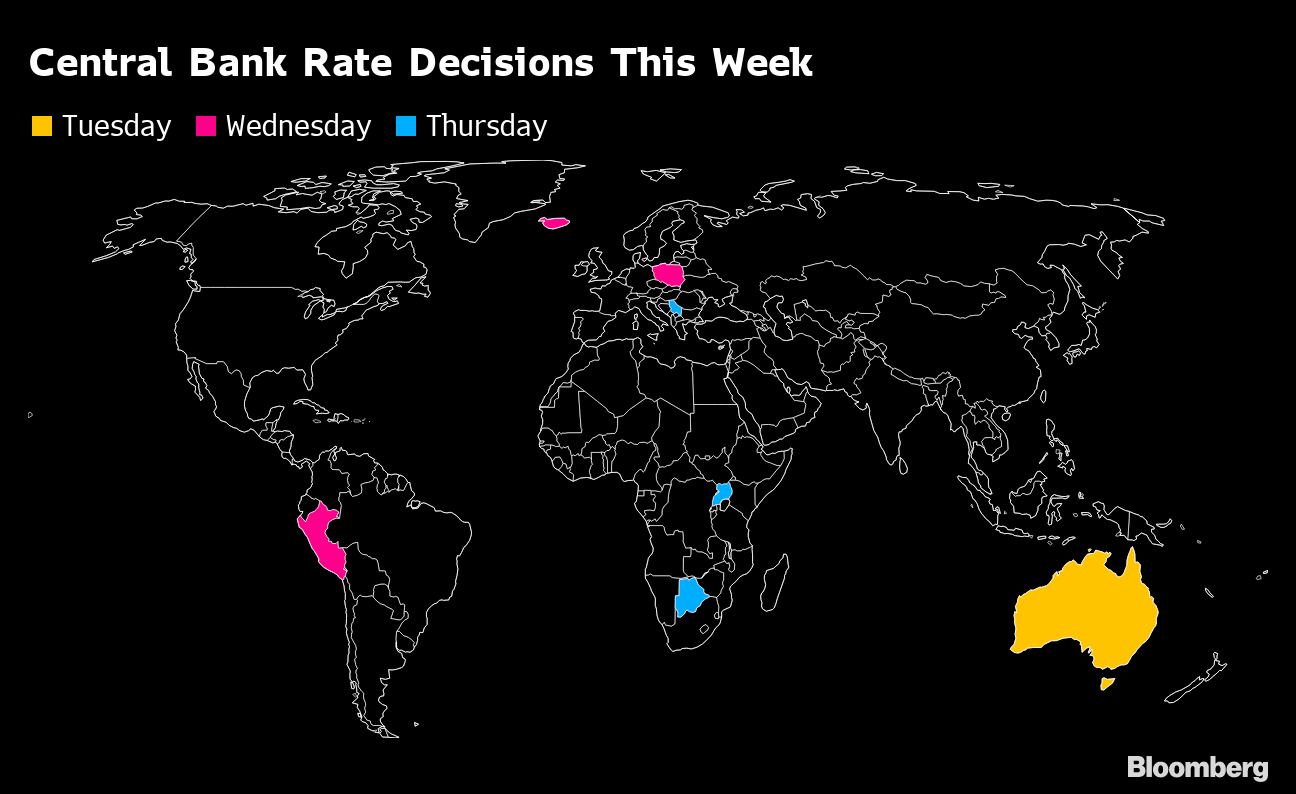

With China shut for its Golden Week holidays, attention shifts to the rest of the region. It’s a busy week in Australia, with the central bank announcing its interest-rate decision on Tuesday, hours before the government unveils its budget plan. Prime Minister Scott Morrison’s government will likely outline additional fiscal stimulus, including infrastructure spending and tax cuts, to pull the economy out of its first recession in nearly 30 years.

Central Bank Rate Decisions This Week

.chart-js display: none;

Bank of Japan Governor Haruhiko Kuroda will speak at events in the coming week. His remarks on the economic recovery and the outlook for prices will be closely watched for any signs of less gloom as the central bank prepares for a meeting later this month. Japanese wage and household spending data will offer the latest indication of how the economy is picking up after recent patchy signals.

Europe, Middle East, Africa

For European Central Bank policy makers including President Christine Lagarde and Chief Economist Philip Lane this week will be a chance to offer any clues on whether the latest disappointing inflation data are enough to move the needle in the debate for extra stimulus. Minutes of the ECB’s September meeting will be published Thursday.

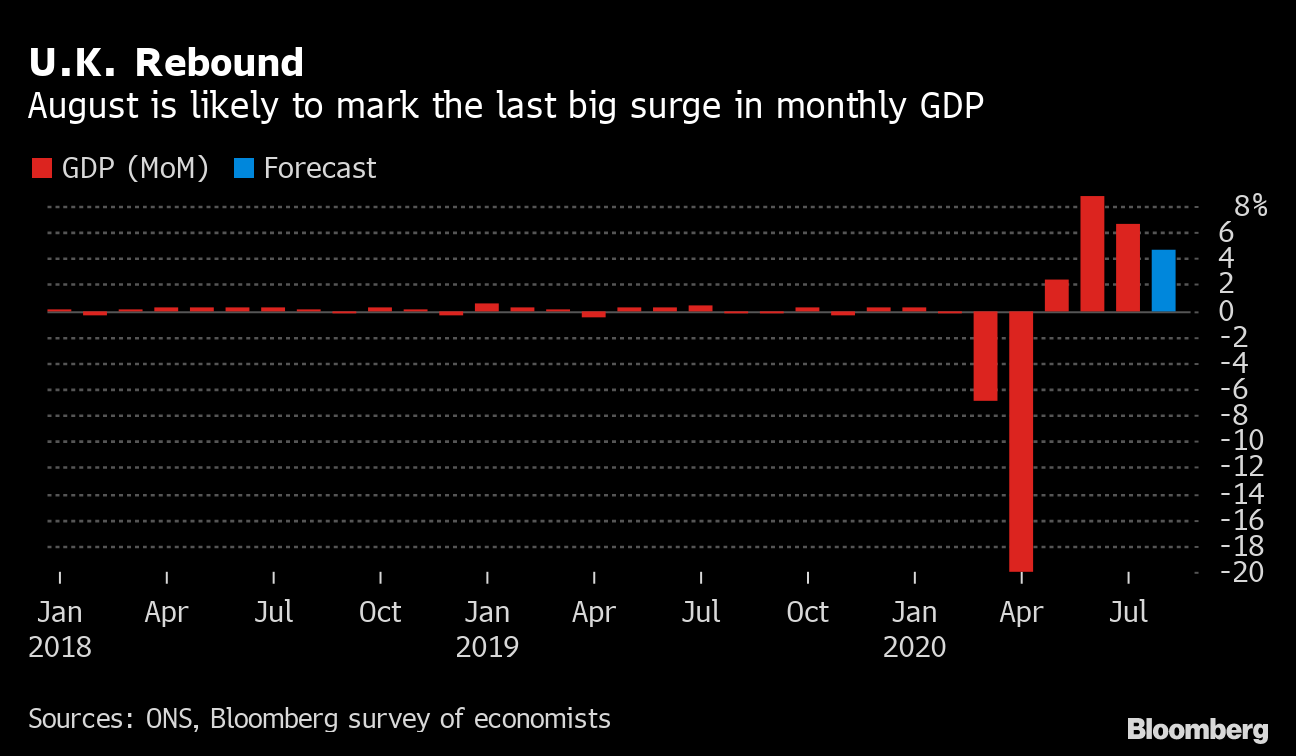

Investors will also be listening closely to remarks by Bank of England officials for signs of any divergent views on the economic rebound and the potential use of negative rates. Monthly U.K. GDP numbers are due Friday.

U.K. Rebound

August is likely to mark the last big surge in monthly GDP

Sources: ONS, Bloomberg survey of economists

.chart-js display: none;

In the Nordics, Norwegian central bank chief Oystein Olsen speaks after surprising markets last month with a more dovish forward guidance than anticipated. Later in the week, Norway published its economic output data for August.

Central banks in Poland, Serbia and Uganda are expected to keep interest rates unchanged, while Botswana may have room to cut.

Latin America

Monday’s reading of Mexico’s consumer confidence may show a fourth month of improvement.

Shaken in Mexico

Consumer, business confidence had been falling before the outbreak

Source: Instituto Nacional de Estadística y Geografía

.chart-js display: none;

In central banking, Peru on Wednesday will pause at 0.25% for a sixth month as the economy begins to turn around, while the minutes from policy makers’ Sept. 24 meeting out Thursday may cement bets that Mexico’s comfortable holding at 4.25%.

Initial Rebound

Brazil retail sales recovered sharply at first, seen slowing up in August

Sources: Instituto Brasileiro de Geografia e Estatistica; Bloomberg survey

Note: August 2020 figures represent median estimates.

.chart-js display: none;

Price data this week will show inflation coming off pandemic-lows in Mexico, Brazil and Chile, while still well under target in Colombia. Brazil’s retail sales report for August will show monthly and annual gains with some loss of momentum.

— With assistance by Alaa Shahine, Nasreen Seria, Robert Jameson, Benjamin Harvey, Christopher Condon, and Theophilos Argitis